[ISC] Q. 28, 29, 30 Solution of Admission of Partner TS Grewal Accounts Class 12 (2026-27)

Solution to Question number 28, 29, 30 of the Admission of partner chapter 3 of TS Grewal Book 2026-27 Edition ISC/CISCE Board?

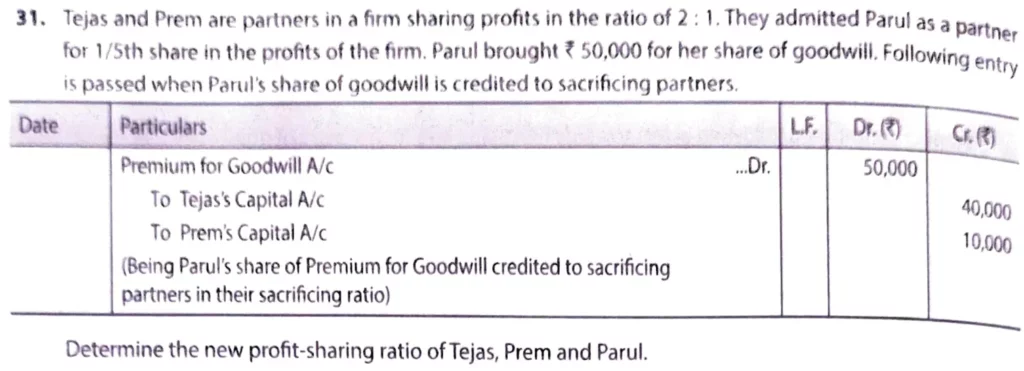

Tejas and Prem are partners in a firm sharing profits in the ratio of 2 : 1. They admitted Parul as a partner for 1/5th share in the profits of the firm. Parul brought ₹ 50,000 for her share of goodwill. Following entry is passed when Parul’s share of goodwill is credited to sacrificing partners.

| Particulars | Dr. (₹) | Cr. (₹) |

| Premium for Goodwill A/c | 50,000 | |

| To Tejas’s Capital A/c To Prem’s Capital A/c (Being Parul’s share of premium for Goodwill credited to sacrificing partners in their sacrificing ratio) | 40,000 10,000 |

Determine the new profit-sharing ratio of Tejas, Prem and Parul.

Solution:-

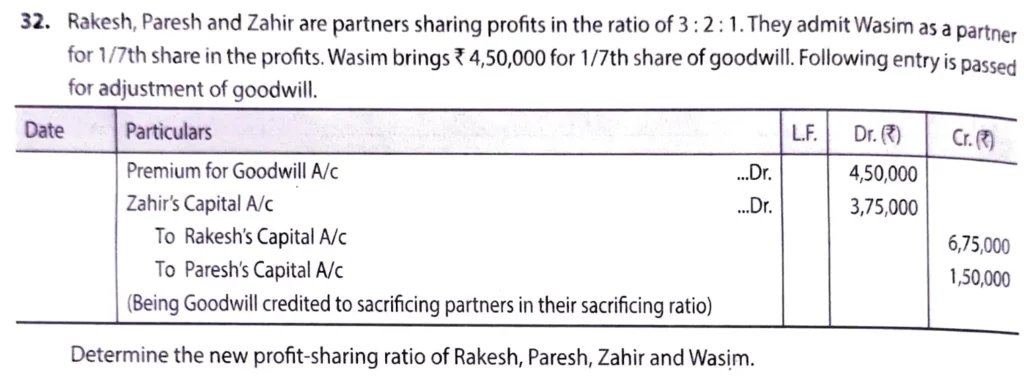

Rakesh, Paresh and Zahir are partners sharing profits in the ratio of 3 : 2 : 1. They admit Wasim as a partner for 1/7th share in the profits. Wasim brings ₹ 4,50,000 for 1/7th share of goodwill. Following entry is passed for adjustment of goodwill.

| Particulars | Dr. | Cr. |

| Premium for Goodwill A/c Dr. Zahir’s Capital A/c Dr. | 4,50,000 3,75,000 | |

| To Rakesh’s Capital A/c To Paresh’s Capital A/c | 6,75,000 1,50,000 |

Determine the new profit sharing ratio of Rakesh, Paresh, Zahir and Wasim.

Solution:-

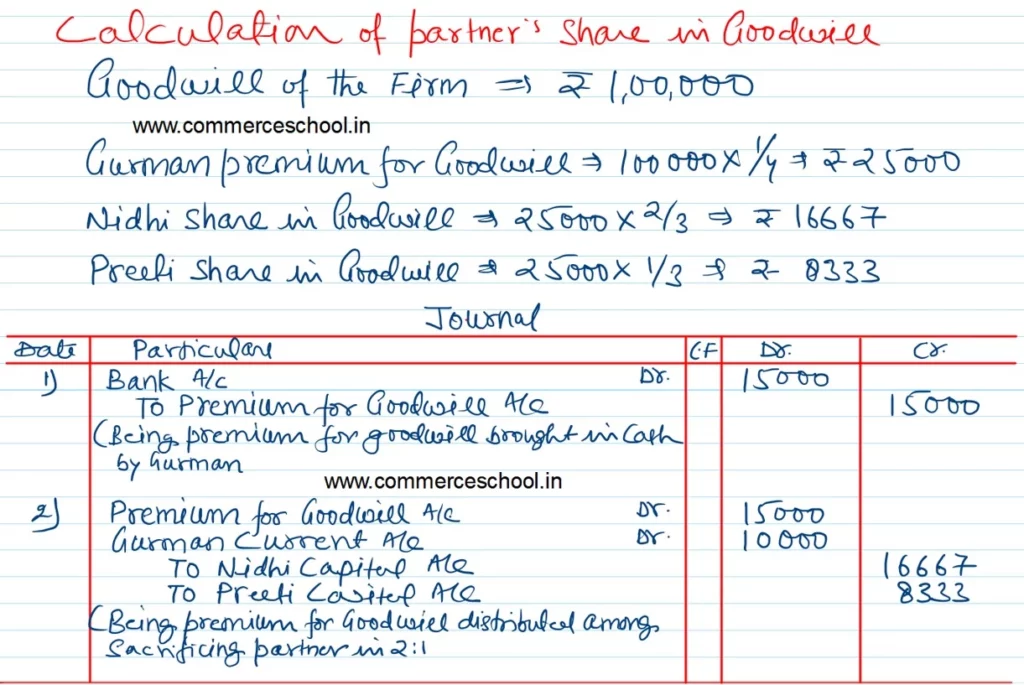

Nidhi and Preeti are partners sharing profits and losses in the ratio of 3 : 2. They admit Gurman into the firm for 1/4th share in profits which he gets 1/6th from Nidhi and 1/12th from Preeti. Gurman brings in 60% of his share of firm’s goodwill. Goodwill of the firm is valued at ₹ 1,00,000. Pass necessary Journal entries to record this arrangement.

Solution:-