[CBSE] Q. 61,62,63,64 Solution of Accounting Ratios TS Grewal Class 12 (2026-27)

Solution of Question 61, 62, 63, 64 Accounting Ratios of TS Grewal Book 2026-27 session CBSE Board

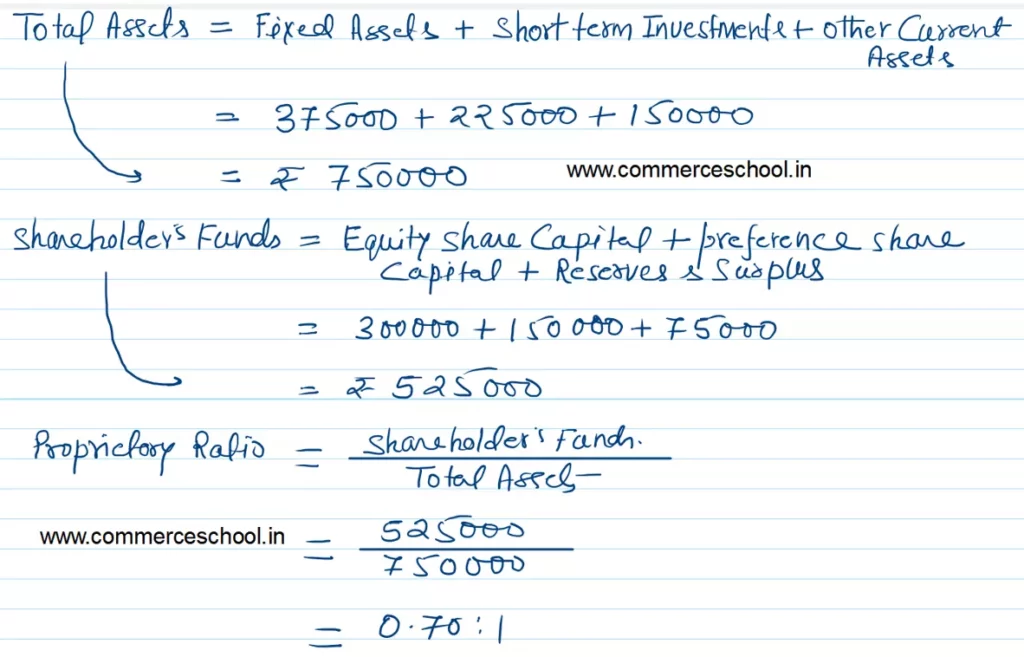

Q. 61. From the following information, Calculate Proprietary Ratio:

| Equity Share Capital | 3,00,000 |

| Preference Share Capital | 1,50,000 |

| Reserves and Surplus | 75,000 |

| Debentures | 1,80,000 |

| Trade Payables | 45,000 |

| Total | 7,50,000 |

| Property, Plant and Equipment | 3,75,000 |

| Short-term Investments | 2,25,000 |

| Other Current Assets | 1,50,000 |

| Total | 7,50,000 |

[Ans.: Proprietary Ratio = 0.70 : 1 or 70%.]

Solution:-

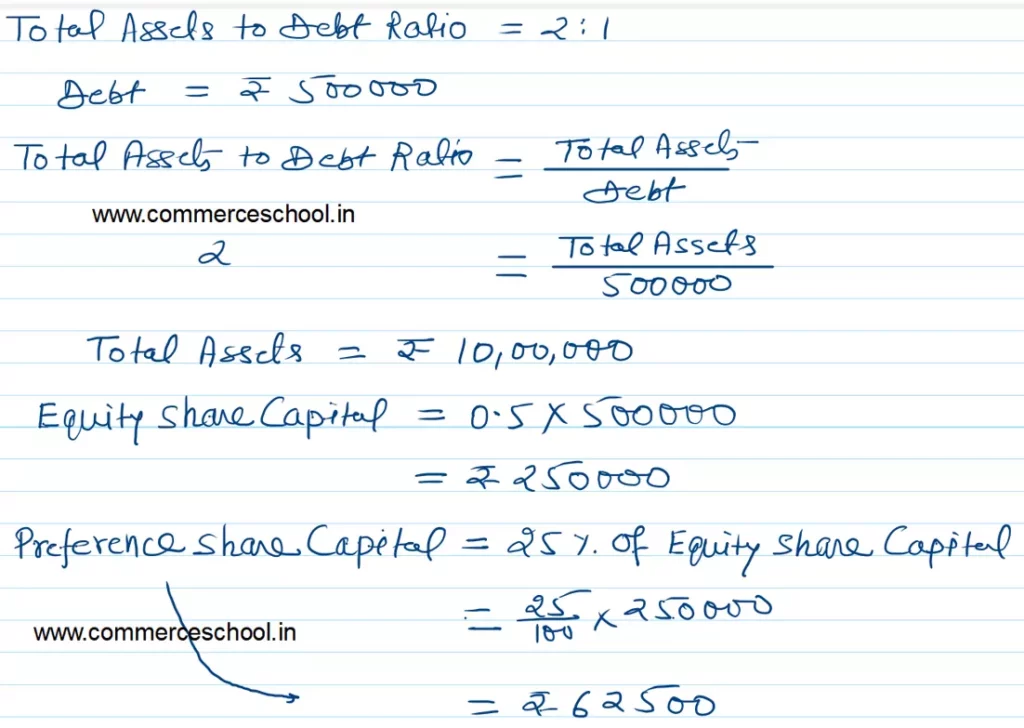

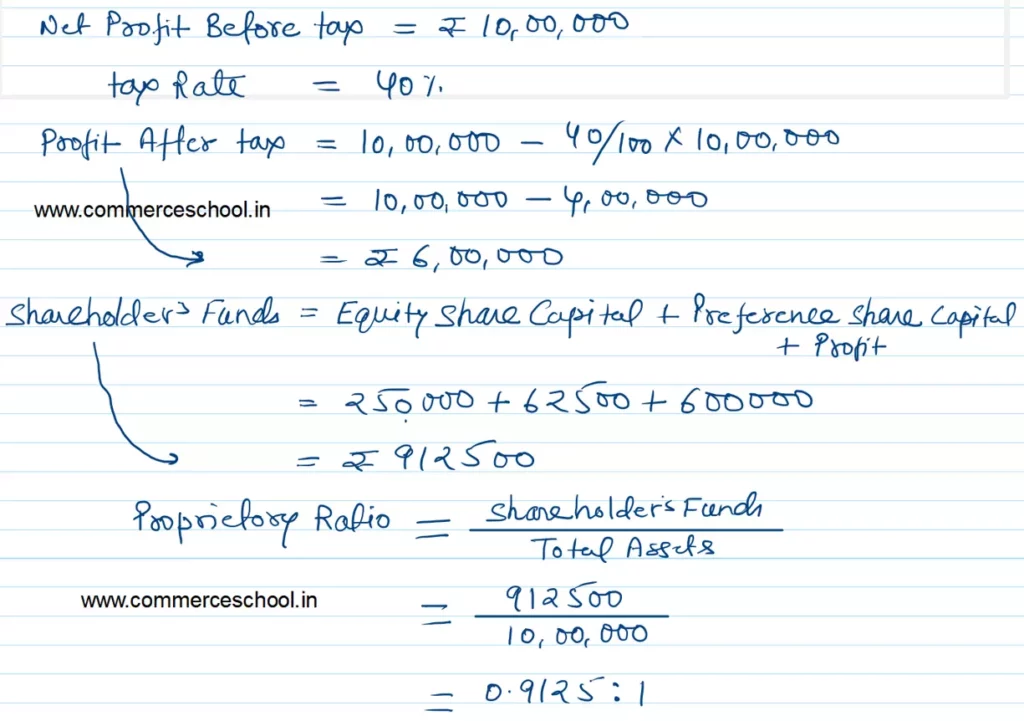

Q. 62. Calculate Proprietary Ratio, if Total Assets to Debt Ratio is 2 : 1. Debt is ₹ 5,00,000.

Equity Shares Capital is 0.5 times of debt. Preference Shares Capital is 25% of equity share capital. Net Profit before tax is ₹ 10,00,000 and rate of tax is 40%.

[Ans.: Proprietary Ratio = 0.912 : 1 or 91.2:.]

Solution:-

Q. 63. State, with reason, whether the Proprietary Ratio will improve, decline or will not change because of the following transactions if Proprietary Ratio is 0.8 : 1.

(i) Obtained a loan of ₹ 5,00,000 from State Bank of India payable after five years.

(ii) Purchased machinery of ₹ 2,00,000 by cheque.

(iii) Redeemed 7% Redeemable Preference Shares ₹ 3,00,000.

(iv) Issued equity shares to the vendor of building purchased for ₹ 7,00,000.

(v) Redeemed 10% redeemable debentures of ₹ 6,00,000.

[Ans.: (i) Decline; (ii) No Change, (iii) Decline; (iv) Improve, (v) Improve.]

Solution:-

(i) Obtained a loan of ₹ 5,00,000 from State Bank of India payable after five years.

The proprietary ratio will be affected by obtaining a loan of ₹ 5,00,000 payable after five years, and here’s how:

Proprietary Ratio Formula:

= Shareholder’s Funds/Total Assets

- Shareholders’ Funds: Includes share capital, reserves, and retained earnings.

- Total Assets: Includes both fixed and current assets.

- Effect of Loan:

- By obtaining a loan, total assets increase because the cash received from the loan is added to the company’s assets.

- However, shareholders’ funds remain unchanged, as the loan is a liability and does not affect equity.

- Impact on Proprietary Ratio:

- The numerator (shareholders’ funds) remains constant.

- The denominator (total assets) increases due to the addition of ₹ 5,00,000 from the loan.

- Since the denominator increases while the numerator stays constant, the proprietary ratio will decrease from its original value of 0.8 : 1, reflecting lower reliance on shareholders’ funds compared to total assets.

(ii) Purchased machinery of ₹ 2,00,000 by cheque.

The purchase of machinery worth ₹ 2,00,000 by cheque will affect the proprietary ratio, and here’s how:

Proprietary Ratio Formula:

= Shareholder’s Funda/Total Assets

- Shareholders’ Funds: Includes share capital, reserves, and retained earnings.

- Total Assets: Includes both fixed and current assets.

- Impact of Transaction:

- Purchasing machinery increases fixed assets (part of total assets) by ₹ 2,00,000.

- Simultaneously, paying via cheque reduces cash/bank balance, so the total assets remain unchanged.

- Shareholders’ funds are also unaffected because this transaction does not involve equity adjustments.

- Final Effect:

- Since neither the numerator (shareholders’ funds) nor the denominator (total assets) changes, the proprietary ratio remains the same at 0.8 : 1.

(iii) Redeemed 7% Redeemable Preference Shares ₹ 3,00,000.

Given the assumed values:

- Shareholders’ Funds (before redemption): ₹ 8,00,000

- Total Assets (before redemption): ₹ 10,00,000

Let’s calculate the proprietary ratio before redemption:

Proprietary Ratio

= Shareholder’s Funds/Total Assets =

= 8,00,000/10,00,000 = 0.8 : 1

Now, consider the redemption of ₹ 3,00,000 preference shares:

- Shareholders’ Funds (after redemption): [ 8,00,000 – 3,00,000 = ₹ 5,00,000 ]

- Total Assets (after redemption): [ 10,00,000 – 3,00,000 = ₹ 7,00,000 ]

Recalculate the proprietary ratio after redemption:

Proprietary Ratio = Shareholders’ Funds\Total Assets

= 5,00,000/7,00,000 = 0.714 : 1 (approx)

Impact: The proprietary ratio decreases from 0.8 : 1 to 0.714 : 1, reflecting reduced reliance on shareholders’ funds relative to total assets.

Reason:-

Shareholders’ Funds:– Includes equity share capital, reserves, and retained earnings. Preference shares (redeemable) are part of shareholders’ funds until redeemed.

Total Assets:- Includes all fixed and current assets.

Impact of Redemption:– Redeeming preference shares decreases shareholders’ funds by ₹ 3,00,000, as this amount is paid out to the preference shareholders.

If the redemption is made from cash or bank balances, total assets also decrease by ₹ 3,00,000.

(iv) Issued equity shares to the vendor of building purchased for ₹ 7,00,000.

Let’s analyze the effect of issuing equity shares to the vendor for a building worth ₹ 7,00,000, given:

- Shareholders’ Funds (before transaction): ₹ 8,00,000

- Total Assets (before transaction): ₹ 10,00,000

Proprietary Ratio (before transaction):

= Shareholders’ Funds\Total Assets

= 8,00,000/10,00,000 = 0.8 : 1

Effects of the Transaction:

- Increase in Shareholders’ Funds:

- Equity shares worth ₹ 7,00,000 are issued, increasing shareholders’ funds to: [ 8,00,000 + 7,00,000 = ₹ 15,00,000 ]

- Increase in Total Assets:

- The building is added as an asset worth ₹ 7,00,000, increasing total assets to: [ 10,00,000 + 7,00,000 = ₹ 17,00,000 ]

Proprietary Ratio After the Transaction:

Proprietary Ratio} = Shareholders’ Funds\Total Assets

= 15,00,000/17,00,000

= 0.882 : 1 (approx)

Impact:

The proprietary ratio increases from 0.8 : 1 to approximately 0.882 : 1. This reflects a stronger reliance on shareholders’ funds compared to total assets, indicating improved financial stability.

(v) Redeemed 10% redeemable debentures of ₹ 6,00,000.

Let’s analyze the effect of redeeming ₹ 6,00,000 worth of 10% redeemable debentures, given:

- Shareholders’ Funds (before redemption): ₹ 8,00,000

- Total Assets (before redemption): ₹ 10,00,000

Proprietary Ratio (before redemption):-

Proprietary Ratio = Shareholders’ Funds\Total Assets

= 8,00,000/10,00,000

= 0.8 : 1

Effects of the Redemption:

- No Change to Shareholders’ Funds:

- Redeeming debentures does not affect shareholders’ funds, as these are liabilities and not part of equity.

- Decrease in Total Assets:

- If ₹ 6,00,000 is paid for the redemption from cash or bank balances, total assets will decrease by ₹ 6,00,000.

Revised Values:

- Shareholders’ Funds (after redemption): ₹ 8,00,000 (unchanged)

- Total Assets (after redemption): [ 10,00,000 – 6,00,000 = ₹ 4,00,000 ]

Proprietary Ratio After Redemption:

Proprietary Ratio = Shareholders’ Funds\Total Assets

= 8,00,000/4,00,000

= 2 : 1

Impact:

- The proprietary ratio increases significantly, from 0.8 : 1 to 2 : 1, indicating a stronger reliance on shareholders’ funds relative to total assets.

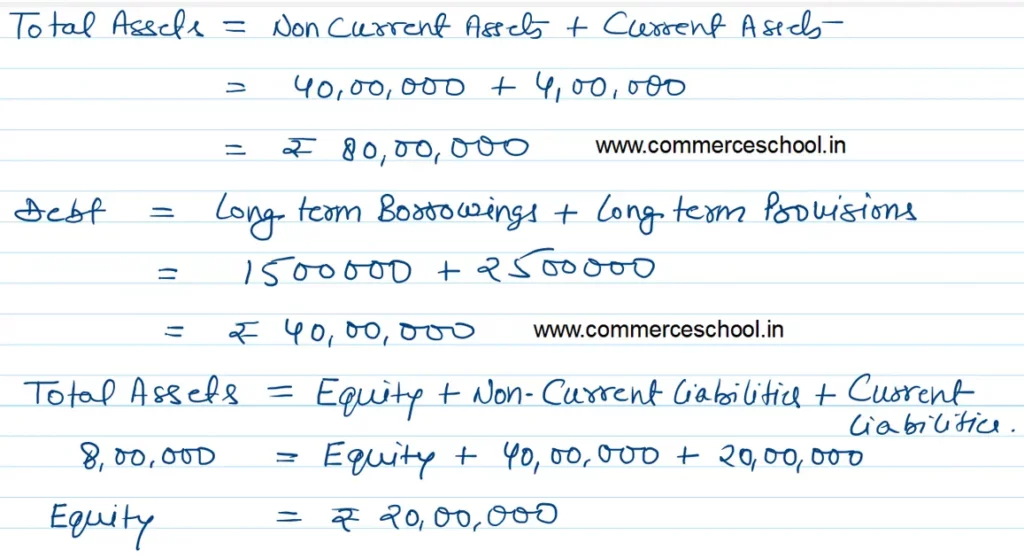

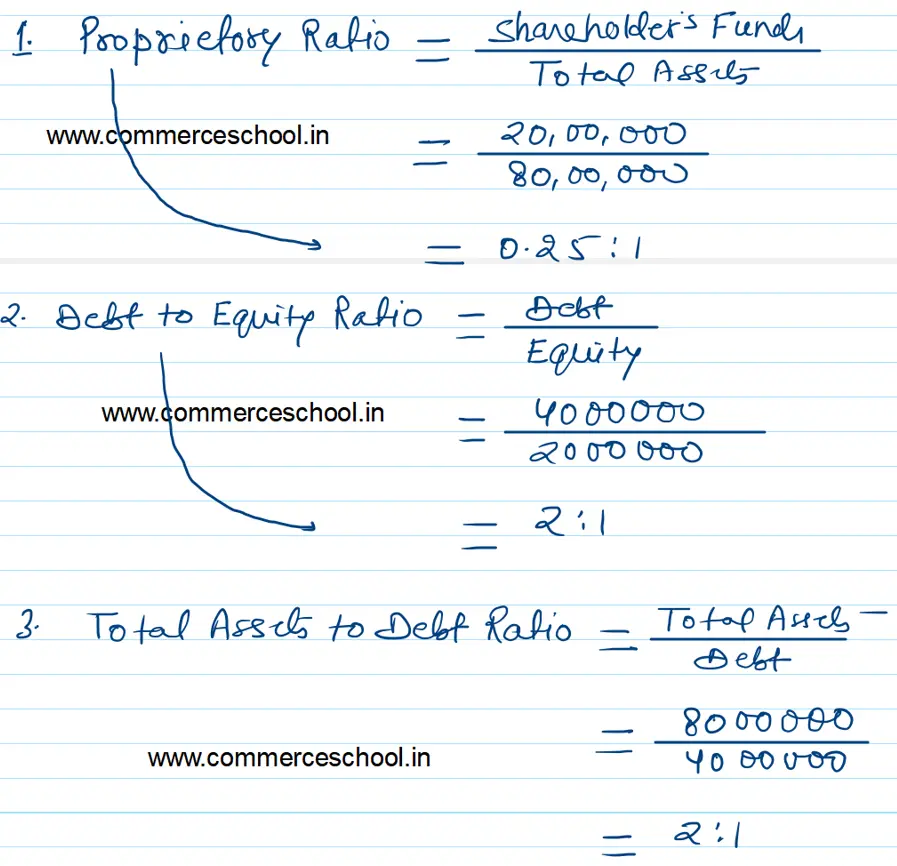

Q. 64. From the following information, calculate:

(a) Proprietary Ratio;

(b) Debt to Equity Ratio; and

(c) Total Assets to Debt Ratio.

| Current Assets | ₹ 40,00,000 |

| Long-term Borrowings | ₹ 15,00,000 |

| Non-Current Assets | ₹ 40,00,000 |

| Current Liabilities | ₹ 20,00,000 |

| Long-term Provisions | ₹ 25,00,000 |

[Ans.: (a) Proprietary Ratio = 25%; (b) Debt to Equity Ratio = 2 : 1; (c) Total Assets to Debt Ratio = 2 : 1.]

Solution:-