[DK Goel] Q. 89,90,91,92 Accounting Ratios Solutions Class 12 CBSE (2026-27)

the solutions of Question number 89, 90, 91, 92 of Accounting Ratios chapter 5 of DK Goel Class 12 CBSE (2026-27)

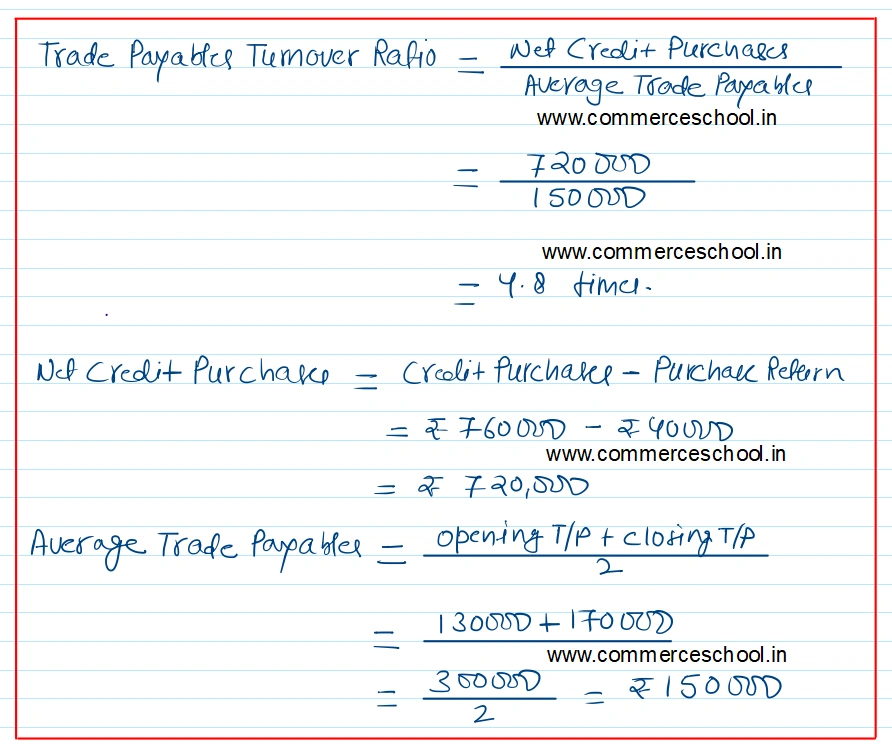

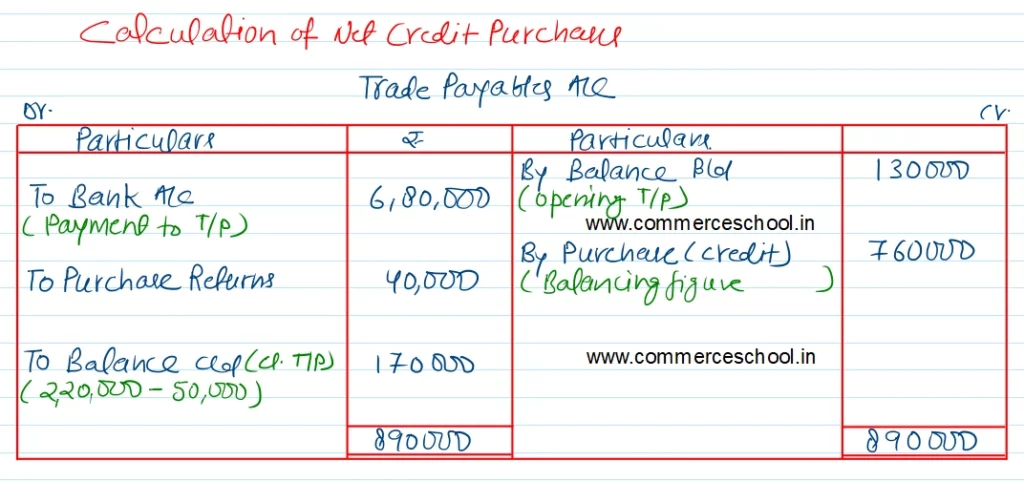

Q. 89. Calculate Trade Payables Turnover Ratio from the following information:

| ₹ | |

| Opening Trade Payables | 1,30,000 |

| Payment to Trade Payables | 6,80,000 |

| Purchase Returns | 40,000 |

| Closing Trade payables (including ₹ 50,000 due to a supplier of machinery) | 2,20,000 |

[Ans. Trade Payables Turnover Ratio : 4.8 times.]

Solution:-

Q. 90. From the following information, find out Opening and Closing Trade Payables:

Total Purchases ₹21,60,000

Cash Purchases are 20% of Credit Purchases

Trade Payables Turnover Ratio is 5 times,

Closing trade payables are one and half times of opening trade payables.

[Ans. Opening Trade Payables 2,88,000; Closing Trade Payables 4,32,000.]

Solution:-

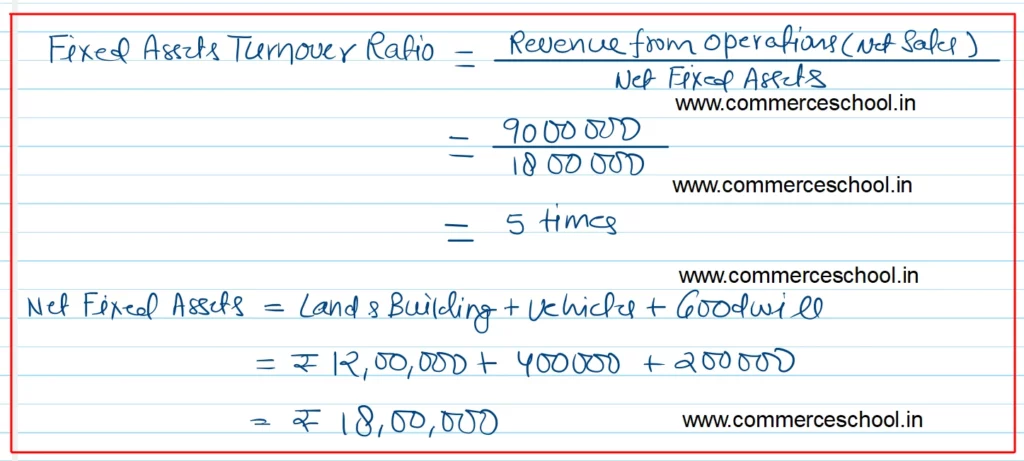

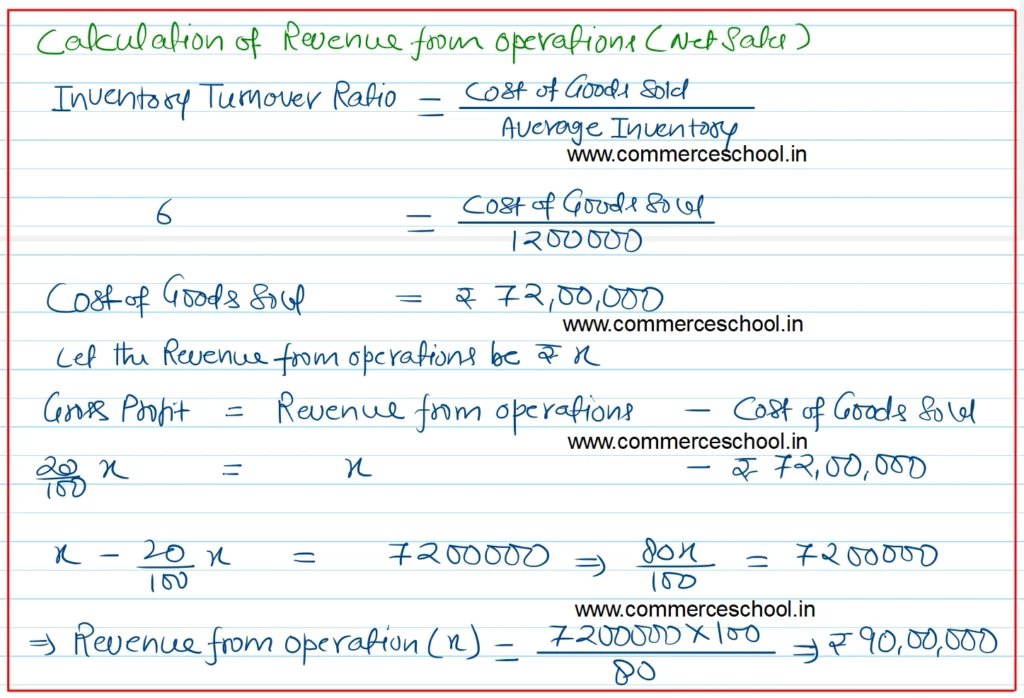

Q. 91. Calculate Fixed Assets Turnover Ratio from the following information:

| ₹ | |

| Land & Building | 12,00,000 |

| Vehicles | 4,00,000 |

| Goodwill | 2,00,000 |

| Cash & Cash Equivalents | 2,00,000 |

| Average Inventory | 12,00,000 |

| Inventory Turnover Ratio | 6 Times |

| Gross Profit | 20% |

[Ans. Fixed Assets Turnover Ratio = 5 Times]

Hints: (I) Cash & Cash Equivalents will be ignored.

(ii) Gross Profit will be considered as 20% on Sales.

Solution:-

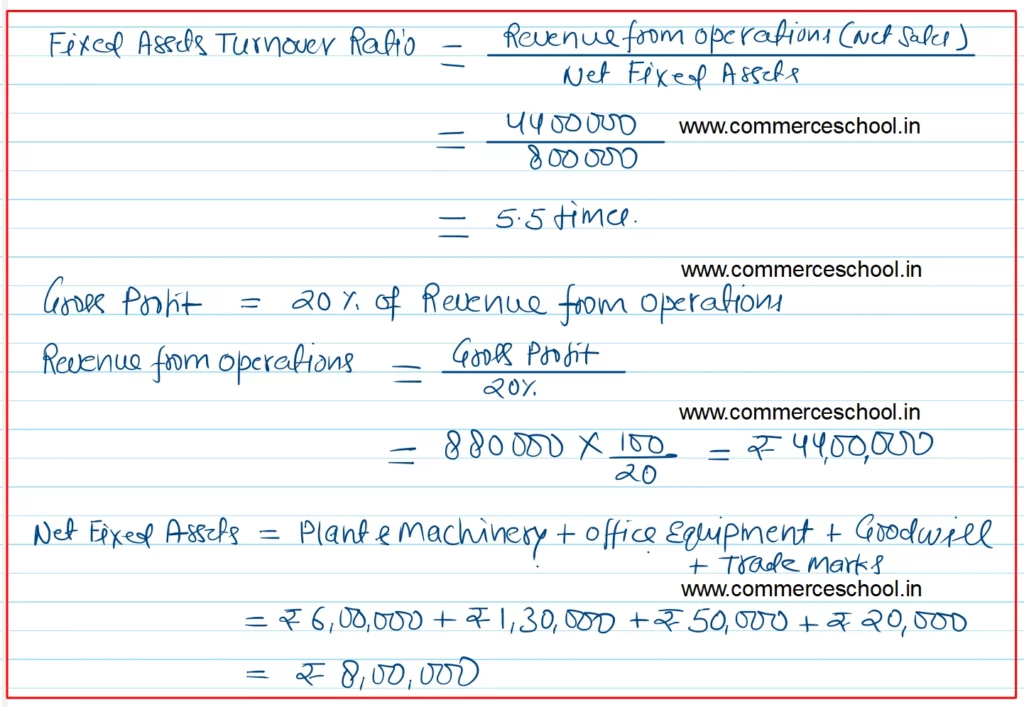

Q. 92. Following information is related to X Ltd.:

| ₹ | |

| Gross Profit | 8,80,000 |

| Ratio of Gross Profit on Sales | 20% |

| Plant & Machinery | 6,00,000 |

| Office Equipment | 1,30,000 |

| Trade Receivables | 2,00,000 |

| Goodwill | 50,000 |

| Trade Marks | 20,000 |

Calculate Fixed Assets Turnover Ratio.

[Ans. Fixed Assets Turnover Ratio = 5.5 Times.]

Solution:-