[DK Goel] Q. 16 Financial Statements (with Adjustments) Solutions Class 11 CBSE (2025-26)

Solutions of Question number 16 of Chapter 20 Financial Statements (with Adjustments) DK Goel class 11 CBSE (2025-26)

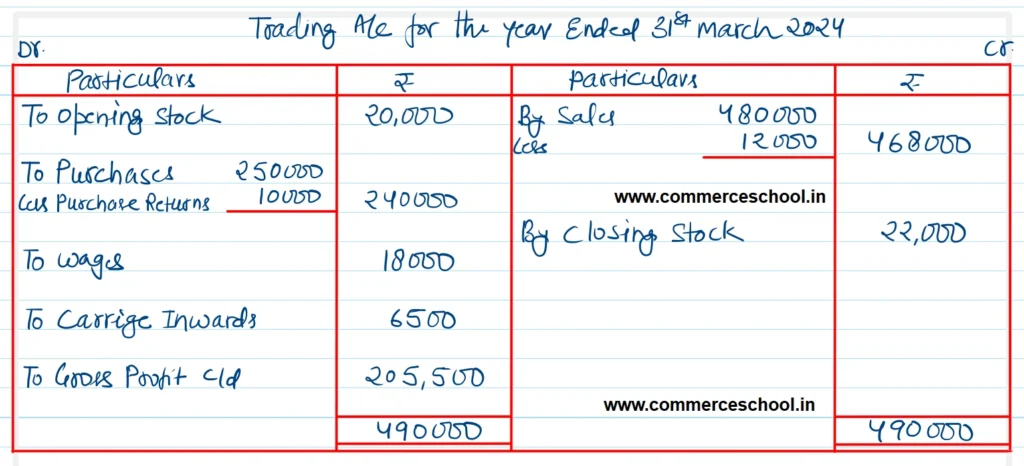

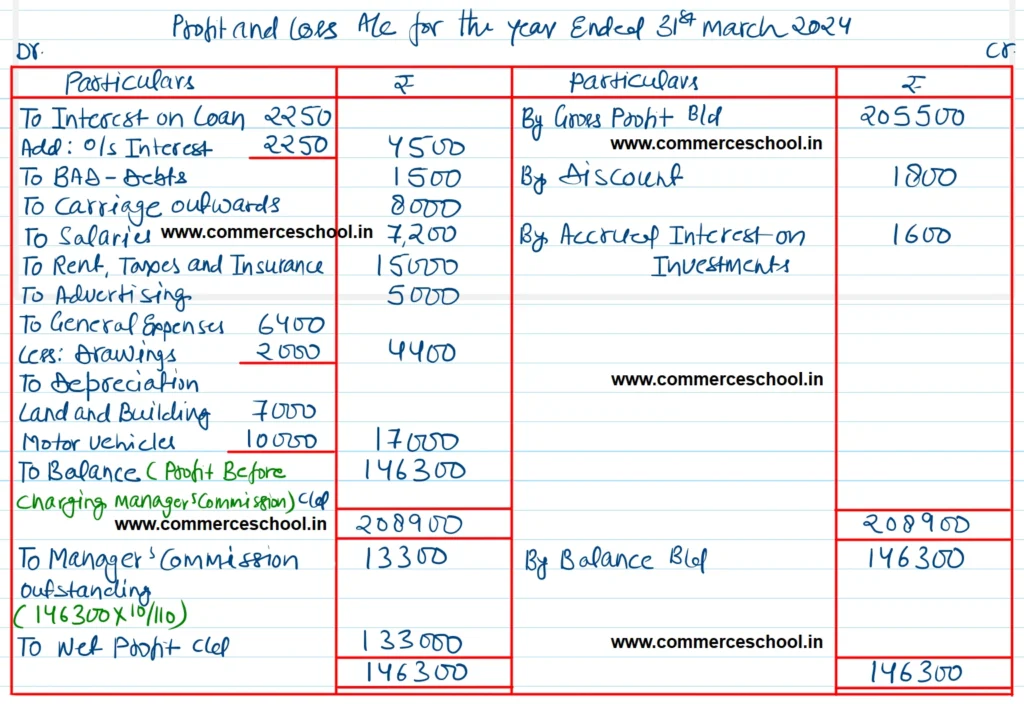

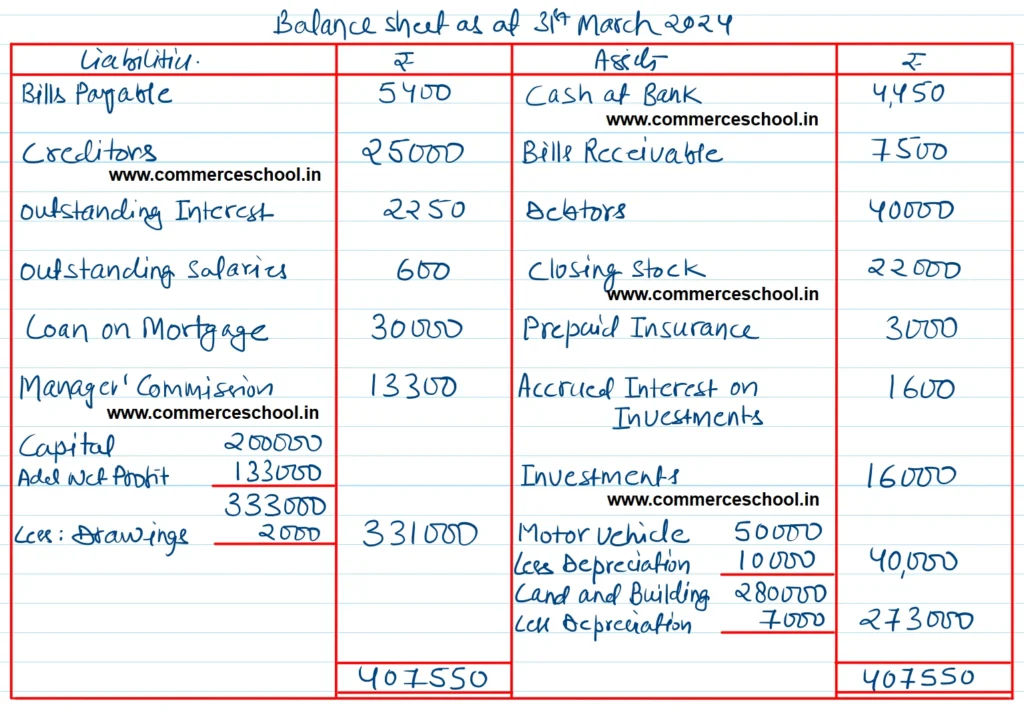

Q. 16 (A). On 31st March, 2023 the following Trial Balance Was extracted from the books of Sh. Ghanshyam Das:-

| Particulars | Dr. (₹) | Cr. (₹) |

| Capital Account | 2,00,000 | |

| Debtors and Creditors | 40,000 | 25,000 |

| Loan on Mortgage | 30,000 | |

| Interest on Loan | 2,250 | |

| Discount | 1,800 | |

| Stock on 1st April, 2022 | 20,000 | |

| Motor Vehicle | 50,000 | |

| Cash at Bank | 4,450 | |

| Investments | 16,000 | |

| Wages | 18,000 | |

| Land and Building | 2,80,000 | |

| Bad-debts | 1,500 | |

| Purchases and Sales | 2,50,000 | 4,80,000 |

| Purchases and Sales Return | 12,000 | 10,000 |

| Carriage Outward | 8,000 | |

| Carriage Inward | 6,500 | |

| Salaries | 7,200 | |

| Outstanding Salaries | 600 | |

| Rates, Taxes and Insurance | 15,000 | |

| Advertising | 5,000 | |

| General Expenses | 6,400 | |

| Bills Receivable and Payable | 7,500 | 5,400 |

| Prepaid Insurance | 3,000 | |

| 7,52,800 | 7,52,800 |

Prepare Trading and Profit & Loss Account for the year ended 31st March, 2023 and Balance Sheet as at that date, after making adjustments for the following matters:

(1) Depreciate Land and Building at 2.5% and Motor Vehicles at 20%.

(2) Interest on Loan at 15% p.a. is unpaid for six months.

(3) Ghanshyam Das withdrew ₹ 2,000 for his private use. The amount was included in general expenses.

(4) Interest on Investments is receivable for full year @ 10%.

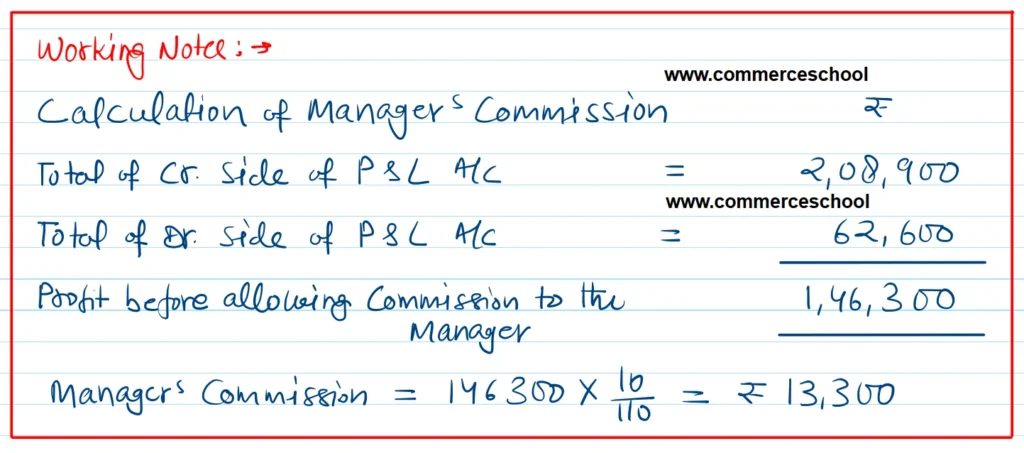

(5) Provide for Manager’s Commission at 10% on Net Profit after charing such commission.

(6) Stock in hand on 31st March, 2023 was valued at ₹ 25,000 (Realisable Value ₹ 22,000).

[Ans. G.P ₹ 2,05,500; N.P. ₹ 1,33,000; B/S Total ₹ 4,07,550.]

Solution:-

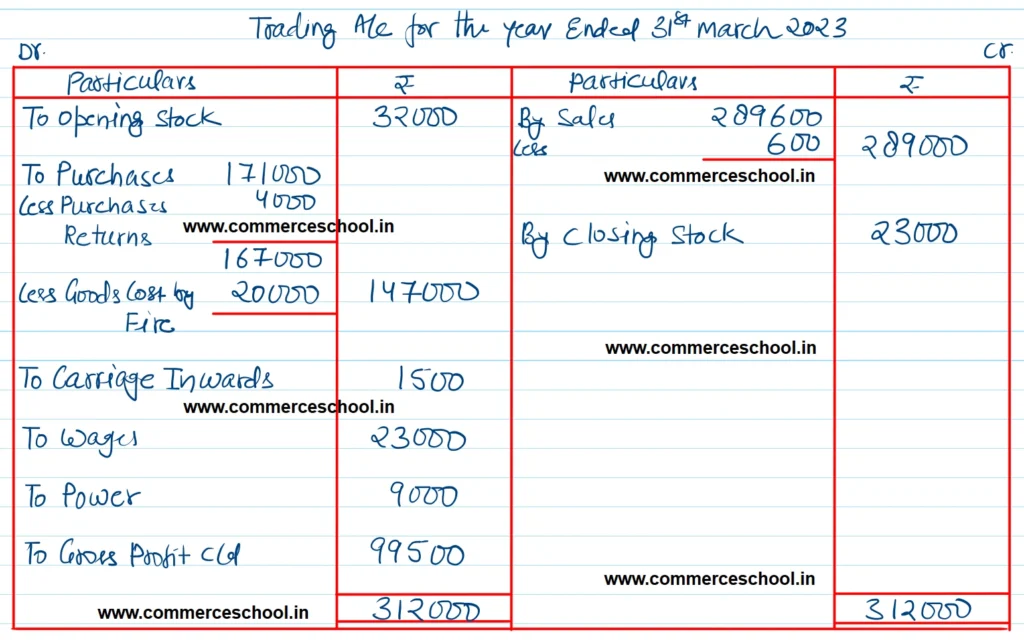

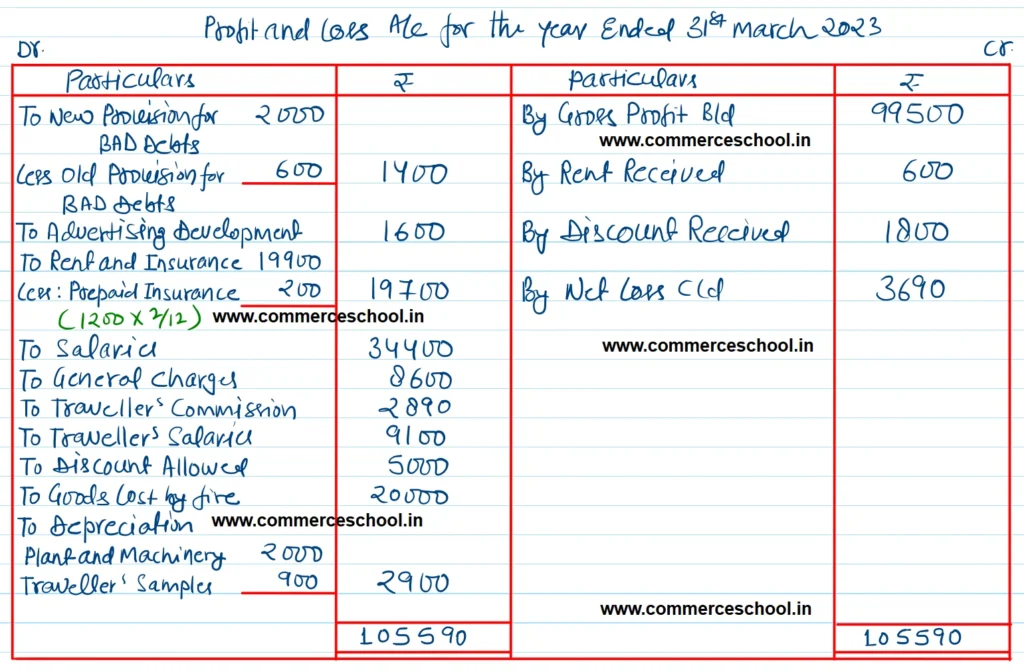

Q. 16 (B) Prepare Trading and Profit and Loss Account and Balance Sheet as at 31st March, 2023 from the following Balances of Mr. Sardari Lal:

| Particulars | ₹ | Particulars | ₹ |

| Capital Account | 41,000 | Drawings | 5,000 |

| Creditors – Trade | 30,000 | Purchases | 1,71,000 |

| Creditors – Expenses | 6,800 | Carriage Inwards | 1,500 |

| Rent Received | 600 | Wages | 23,000 |

| Purchases Returns | 4,000 | Power | 9,000 |

| Sales | 2,89,600 | Rent and Insurance | 19,900 |

| Bad-debts Provision on 1s April, 2022 | 600 | Salaries | 34,400 |

| Advertising Development | 8,000 | Discount Received | 1,800 |

| Goodwill | 5,000 | General Charges | 8,600 |

| Plant and Machinery | 20,000 | Sales Returns | 600 |

| Traveller’s Samples | 2,700 | Traveller’s Commission | 2,890 |

| Stock on 1-4-2022 | 32,000 | Traveller’s Salaries | 9,100 |

| Debtors | 14,600 | Discount Allowed | 5,000 |

| Cash at Bank | 2,000 | ||

| Cash in Hand | 110 |

Adjustments:- The Closing stock was ₹ 23,000 but there has been a loss by fire on 20th March, 2023, to the extent of ₹ 20,000, not covered by insurance. Depreciate Plant and Machinery by 10% and Traveller’s Samples by 331/3%. Increase the Bad-debts Provision to ₹ 2,000. Write 20% off Advertising Development Account. Annual premium on insurance expiring 1st June, 2023 was ₹ 1,200. Provide for Manager’s commission @ 5% on Net Profits after charging such Commission.

[Ans. G.P. ₹ 99,500, Net Loss ₹ 3,690, B/S Total ₹ 69,110.]

Solution:-

Hints:-

(1) Creditors Trade and Creditors Expenses, both will be shown on the Liabilities side.

(2) Insurance is prepaid for the two months of April and May. As such, the Prepaid Insurance will be ₹ 1,200 x 2/12 = ₹ 200.

(3) Manager will not be entitled to any Commission because there is Net Loss instead of Net Profit in the Question.

Below is the list of all solutions

| S.N | Solutions |

| 1 | Question – 1 |

| 2 | Question – 2 |

| 3 | Question – 3 |

| 4 | Question – 4 |

| 5 | Question – 5 |

| 6 | Question – 6 |

| 7 | Question – 7 |

| 8 | Question – 8 |

| 9 | Question – 9 |

| 10 | Question – 10 |

| S.N | Solutions |

| 11 | Question – 11 |

| 12 | Question – 12 |

| 13 | Question – 13 |

| 14 | Question – 14 |

| 15 | Question – 15 |

| 16 | Question – 16 |

| 17 | Question – 17 |

| 18 | Question – 18 |

| 19 | Question – 19 |

| 20 | Question – 20 |

| S.N | Solutions |

| 21 | Question – 21 |

| 22 | Question – 22 |

| 23 | Question – 23 |

| 24 | Question – 24 |

| 25 | Question – 25 |

| 26 | Question – 26 |

| 27 | Question – 27 |

| 28 | Question – 28 |

| 29 | Question – 29 |

| 30 | Question – 30 |

| S.N | Solutions |

| 31 | Question – 31 |

| 32 | Question – 32 |

| 33 | Question – 33 |

| 34 | Question – 34 |

| 35 | Question – 35 |

| 36 | Question – 36 |

| 37 | Question – 37 |

| 38 | Question – 38 |

| 39 | Question – 39 |