[200] MCQs of Admission of Partner chapter Class 12

A and B are partners sharing profits and losses in 3:2. They admit C into a partnership for 3/10th share in the profits. A surrenders 1/3rd of his share and B surrenders 1/4th of his share in favour of C. Goodwill of the firm is valued at ₹3,00,000 but C is unable to bring his share of goodwill in cash. Credit will be given to:

a) A ₹54,000; B ₹36,000

b) A ₹60,000; B ₹30,000

c) A ₹2,00,000; B ₹1,00,000

d) A ₹1,80,000; B ₹1,20,000

Ans:- b)

Explanation:-

A surrenders = 3/5 x 1/3 = 3/15

B Surrenders = 2/5 x 1/4 = 2/20

Sacrificing ratio of A & B after making base equal

= 3/15 x 4/4 : 2/20 x 3/3 i.e., 2 : 1

C’s premium for goodwill

= 3,00,000 x 3/10 = ₹ 90,000

A will be credited

= 90,000 x 2/3 = ₹ 60,000

B will be credited

= 90,000 x 1/3 = ₹ 30,000

A and B are two partners sharing profits in the ratio of 2:1. C, a new partner admitted for 1/4th share. At the time of admission, loss from revaluation is ₹9,000. Pass a necessary journal entry for distribution of loss between the partners?

a) A’s Capital A/c Dr 6,000

B’s Capital A/c Dr 3,000

To Revaluation A/c 9,000

b) A’s Capital A/c Dr 9,000

To B’s capital A/c 9,000

c) Revaluation A/c Dr 9,000

To A’s Capital A/c 6,000

To B’s Capital A/c 3,000

d) B’s Capital A/c 9,000

To A’s Capital A/c 9,000

Ans:- a)

Explanation:-

Revaluation loss will be debited to A and B in 2 : 1

A will be debited

= 9,000 x 2/3 = ₹ 6,000

B will be debited

= 9,000 x 1/3 = ₹ 3,000

When a new partner doesn’t bring his share of goodwill in cash, the amount is debited to:

a) Cash A/c

b) Current A/c of a new partner

c) Capital A/cs of an old partner

d) Premium for Goodwill A/c

Ans:- b)

A and B are partners sharing profits in the ratio of 7:5. C is admitted into the partnership for 1/6th share which he acquires 1/24th from A and 1/8th from B. C does not pay anything for his share of goodwill. On C’s admission, firm’s goodwill was valued at ₹1,80,000. Credit

will be given to:

a) A ₹22,500; B ₹ 7,500

b) A ₹7,500; B ₹22,500

c) A ₹45,000; B ₹1,35,000

d) A ₹1,35,000; B ₹45,000

Ans:- b)

Explanation:-

Sacrificing ratio of A and B after making base equal is

= 1/24 : 1/8 x 3/3 = 1 : 3

C’s premium for goodwill

= 1,80,000 x 1/6 = ₹ 30,000

A will be credited

= 30,000 x 1/4 = ₹ 7,500

B will be credited

= 30,000 x 3/4 = ₹ 22,500

A and B are partners in a firm with a capital of ₹1,80,000 and ₹2,00,000. C was admitted for 1/3rd share in profit and brings ₹3,40,000 as capital. Calculate the amount of goodwill.

a) ₹2,40,000

b) ₹1,00,000

c) ₹1,50,000

d) ₹3,00,000

Ans:- d)

Explanation:-

Total Capital of the firm (Including goodwill)

C’s Capital x reciprocal of his share

= 3,40,000 x 3 = ₹ 10,20,000

Total Capital of the firm (excluding goodwill)

A’s Capital + B’s Capital + C’s Capital

= ₹ 1,80,000 + ₹ 2,00,000 + ₹ 3,40,000

= ₹ 7,20,000

Goodwill of the firm = Total Capital of the firm (Including goodwill) – Total Capital of the firm (Excluding goodwill)

= ₹ 10,20,000 – ₹ 7,20,000

= ₹ 3,00,000

X and Y are partners in a firm sharing profits in the ratio of 5:3. They admitted Z as a new partner. The new profit sharing ratio will be 4:3:2. The firm’s goodwill on Z’s admission was valued at ₹1,26,000. But Z could not bring any amount of goodwill in cash. Credit

will be given to:

a) X ₹17,500; Y ₹10,500

b) X ₹16,000; Y ₹12,000

c) X ₹22,750; Y ₹5,250

d) X ₹1,02,375; Y ₹23,625

Ans:- c)

Explanation:-

Sacrificing ratio of X and Y is

X sacrifices

= 5/8 – 4/9 = 13/72

Y sacrifices = 3/8 – 3/9 = 3/72

Sacrificing ratio of X and Y is 13 : 3

Z’s premium for goodwill

= 1,26,000 x 2/9 = ₹ 28,000

X will be credited

= 28,000 x 13/16 = ₹ 22,750

Y will be credited

= 28,000 x 3/16 = ₹ 4,250

If, at the time of admission, some profit and loss account balance appears in the books, it will be transferred to:

a) Profit and Loss-Adjustment A/c

b) Revaluation A/c

c) Old partner’s capital account

d) All partner’s capital accounts

Ans:- c)

A and B are partners sharing profits in the ratio of 3:2. They admit C into the partnership with 1/4th share in future profits. The new profit sharing ratio is 5:4:3. The firm’s goodwill on C’s admission was valued at ₹1,44,000. But C could not bring any amount for goodwill in cash. Credit will be given to:

a) A ₹80,000; B ₹64,000

b) A ₹20,000; B ₹16,000

c) A ₹1,05,600; B ₹38,400

d) A ₹26,400; B ₹9,600

Ans:- d)

Explanation:-

A sacrifices = 3/5 – 5/12 = 11/60

B sacrifices = 2/5 – 4/12 = 4/60

Sacrificing ratio of A and B is 11 : 4

C’s premium for goodwill

= 1,44,000 x 3/12 = ₹ 36,000

A will be credited

= 36,000 x 11/15 = ₹ 26,400

B will be credited

= 36,000 x 4/15 = ₹ 9,600

If at the time of admission, the revaluation A/c shows a loss, it should be:

a) Credited to old partners capital A/c in the old ratio

b) Credited to old partners capital A/c in sacrificing ratio

c) Debited to old partners capital A/c in the old ratio

d) Debited to old partners capital A/c in sacrificing ratio

Ans:- c)

P, Q and R share profits in the ratio of 5:3:2. S is entitled for 1/5th share in profits which he acquires equally from P, Q and R. Goodwill of the firm is to be valued at three year’s purchase of last four years profits which are ₹50,000; ₹60,000; (-) ₹30,000 and ₹40,000. S can not bring his share of goodwill in cash. Credit will be given to:

a) P ₹30,000; Q ₹30,000; R ₹30,000

b) P ₹6,000; Q ₹6,000; R ₹6,000

c) P ₹45,000; Q ₹27,000; R ₹18,000

d) P ₹9,000; Q ₹ 9,000; R ₹9,000

Ans:- b)

Calculation of Goodwill of the firm

Total Profit of last 4 years

= ₹ 50,000 + ₹ 60,000 – ₹ 30,000 + ₹ 40,000 = ₹ 1,20,000

Average Profit of last 4 years

= 1,20,000/4 = ₹ 30,000

Goodwill of the firm

= Average Profit of last 4 years x 3 years purchase

= 30,000 x 3 = ₹ 90,000

S’s premium for goodwill

= 90,000 x 1/5 = ₹ 18,000

Sacrificing ratio of P, Q and R is 1 : 1 : 1

P, Q and R will be credited each

= 18,000 x 1/3 = ₹ 6,000

Revaluation A/c is a:

a) Real account

b) Asset account

c) Personal account

d) Nominal account

Ans:- d)

Explanation:-

Revaluation account follows nominal account rule, debit all expenses/losses and credit all revenue/gain.

When a new partner brings his share of goodwill in cash, the amount is debited to:

a) Goodwill A/c

b) Capital A/c of the new partner

c) Cash A/c

d) Capital A/cs of the old partners

Ans:- c)

L and M are partners sharing profits in the ratio of 3:2 respectively. N was admitted for 1/5th share of profit. Machinery (Book value ₹80,000) would be appreciated by 10% and Building (Book value ₹2,00,000) would be depreciated by 20%. Unrecorded debtors of ₹1,250 would be brought into books and a creditor amounting to ₹2,750 died and need not pay anything on this account. What will be profit/loss on revaluation?

a) Loss ₹28,000

b) Profit ₹28,000

c) Loss ₹40,000

d) Profit ₹40,000

Ans – a)

Ans:- a)

Explanation:-

When a new partner does not bring his share of goodwill in cash, the amount is debited to:

a) Cash A/c

b) Premium A/c

c) Current A/c of the new partner

d) Capital A/cs of the old partners

Ans:- c)

A and B are partners sharing profits in the ratio of 2:1. C is admitted for 1/4th share of profits which he acquired equally from A and B. C brings ₹30,000 as goodwill, it will be credited to old partners as:

a) ₹ 15,000 each

b) ₹ 20,000, ₹ 10,000 respectively

c) ₹ 10,000, ₹ 20,000 respectively

d) None of these

Ans:- a)

Explanation:-

sacrificing ratio of A and B is 1 : 1

A and B will be credited each

= 30,000 x 1/2 = ₹ 15,000

If at the time of admission, some profit and loss amount balance appears in the books, it will be transferred to:

a) Profit and Loss Adjustment Account

b) All partner’s Capital Accounts

c) Old Partner’s Capital Accounts

d) Revaluation Account

Ans:- c)

A and B are sharing profits and losses in the ratio of 4:1. C is admitted as a new partner for 1/3rd share of profits for which he pays ₹3,00,000 as goodwill. If A and B agree to share future profits equally. then the amount of goodwill to be credited to A is:

a) ₹3,00,000

b) ₹9,00,000

c) ₹4,80,000

d) ₹4,20,000

Ans:- d)

Explanation:-

As C comes for 1/3rd share & A and B would share remaining profit in 1 : 1, A, B and C would become equal partner for 1 : 1 :1

A sacrifices

= 4/5 – 1/3 = 7/15

B sacrifices

= 1/5 – 1/3 = – 2/15

Goodwill of the firm

= 3,00,000 x 3 = ₹ 9,00,000

A will be credited

= 9,00,000 x 7/15 = ₹ 4,20,000

If at the time of admission, there is some unrecorded liability, it will be:

a) Debited to Revaluation Account

b) Credited to Revaluation Account

c) Debited to Goodwill Account

d) Credited to partner’s capital A/c

Ans:- a)

A and B are partners sharing profits and losses in the ratio of 3:2. C is admitted into a partnership for 1/5th share in profit. He pays ₹ 1,00,000 as goodwill. The ratio of the partner’s A, B and C in the new firm would be 3:1:1. Goodwill will be credited to:

a) only A ₹1,00,000

b) only B ₹1,00,000

c) A ₹60,000; B ₹40,000

d) A ₹75,000; B ₹25,000

Ans:- b)A sacrifices = 3/5 – 3/5 = 0/5

B sacrifices = 2/5 – 1/5 = 1/5

As only B sacrifices, he will only be credited by ₹ 1,00,000.

If the new partner brings his share of goodwill in cash, it will be shared by old partners in:

a) Ratio of sacrifice

b) Old profit sharing ratio

c) New profit sharing ratio

d) In capital ratio

Ans:- a)

P and Q share profits and losses equally. They have ₹20,000 each as capital. They admit S as an equal partner and goodwill was valued at ₹30,000. S is to bring in ₹30,000 as his capital and necessary cash towards his share of goodwill. Goodwill Account will not remain open in books. If the profit on revaluation is ₹13,000, the closing balance of the capital account of P, Q and R are

a) ₹31,500; ₹31,500; ₹30,000

b) ₹31,500; ₹31,500; ₹20,000

c) ₹26,500; ₹26,500; ₹30,000

d) ₹20,000; ₹20,000: ₹30,000

Ans:- a)

Explanation:-

C’s Premium for Goodwill

= 30,000 x 1/3 = ₹ 10,000

Sacrificing ratio of A and B is 1 : 1

A will be credited

10,000 x 1/2 = ₹ 5,000

B will be credited

10,0000 x 1/2 = ₹ 5,000

Revaluation Profit = ₹ 13,000

A will be credited

= 13,000 x 1/2 = ₹ 6,500

B will be credited

= 13,000 x 1/2 = ₹ 6,500

A’s Closing Capital

= ₹ 20,000 + ₹ 5,000 + ₹ 6,500 = ₹ 31,500

B’s Closing Capital = ₹ 20,000 + ₹ 5,000 + ₹ 6,500 = ₹ 31,500

C’s Closing Capital

= ₹ 30,000

At the time of admission of a new partner, General Reserve is appearing in the old Balances Sheet is transferred to:

a) All Partner’s Capital Accounts in new ratio

b) Old Partner’s Capital Accounts in sacrificing ratio

c) Old Partner’s Capital Accounts in the old ratio

d) None of these

Ans:- c)

In the absence of an express agreement as to who will contribute to the new partner’s share of profit, it is implied that the old partners will contribute:

a) Equally

b) In the ratio of their capitals

c) In their old profit sharing ratio

d) In the gaining ratio

Ans:- c)

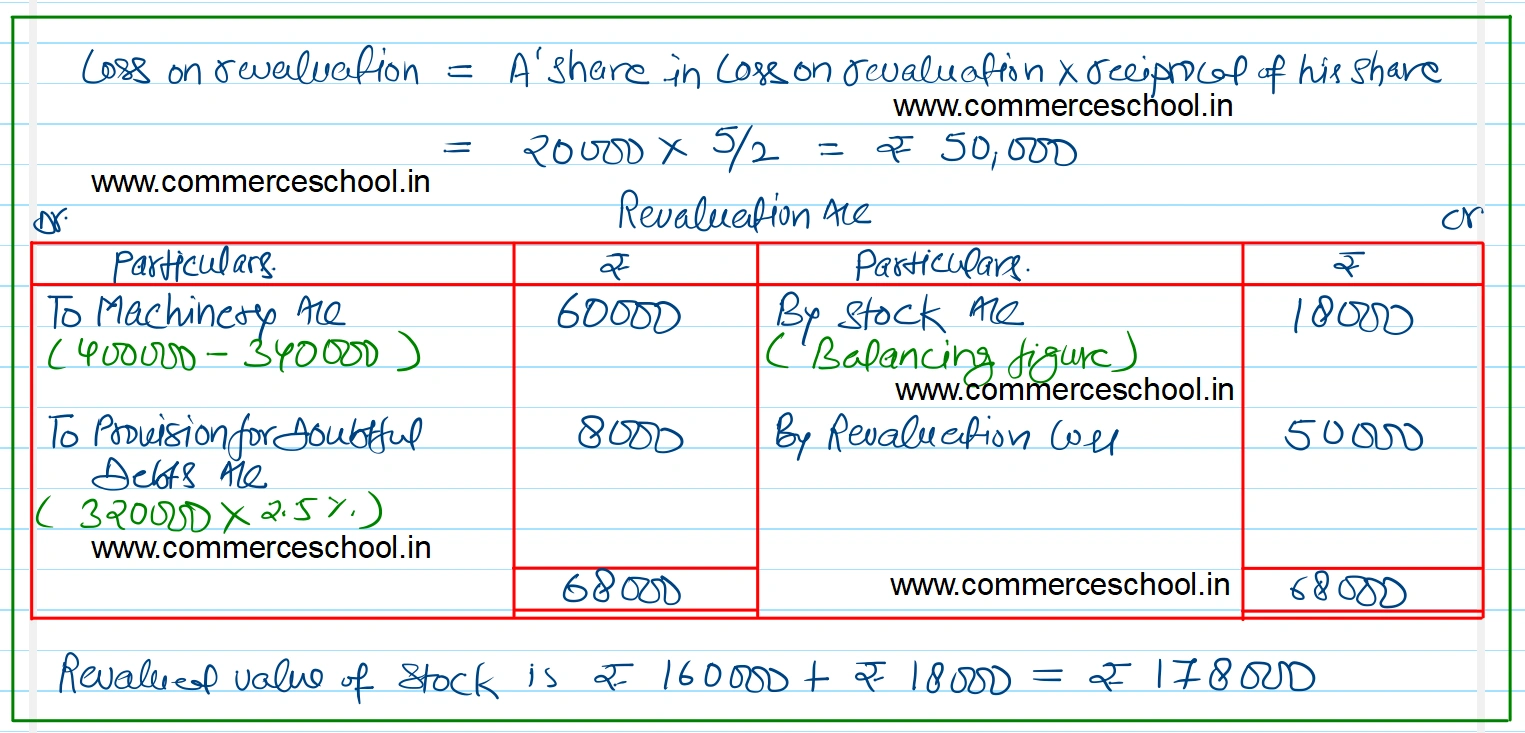

A and B are partners sharing profits in the ratio of 2:3. Their balance sheet shows machinery at ₹4,00,000; stock at ₹1,60,000 and Debtors at ₹3,20,000. C is admitted and a new profit sharing ratio is agreed at 6:9:5. Machinery is revalued at ₹3,40,000 and a provision is made for doubtful debts @2.5%. A’s share in loss on revaluation amounts to ₹20,000. Revalued value of the stock will be:

a) ₹98,000

b) ₹1,00,000

c) ₹1,78,000

d) ₹62,000

Ans:- c)

Explanation:-

When a new partner brings goodwill in cash, it is credited to:

a) his capital A/c

b) Sacrificing Partner’s Capital A/c

c) Old Partner’s Capital A/cs

d) All Partner’s Capital A/cs

Ans:- b)

For which of the following situations, the old profit sharing ratio of partners is used at the time of admission of a new partner?

a) When a new partner brings only a part of his share of goodwill.

b) When a new partner is not able to bring his share of goodwill

c) When at the time of admission, goodwill already appears in the balance sheet.

d) When a new partner brings his share of goodwill in cash

Ans:- c)

If the incoming partner brings the amount of goodwill in cash and also a balance exists in the goodwill account, then this goodwill account is written off among the old partners in

a) The new profit sharing ratio

b) The old profit sharing ratio

c) The sacrificing ratio

d) The gaining ratio

Ans:- b)

X and Y are the partners in firm sharing profits and losses in the ratio of 5:3. Z is admitted who acquires 1/3rd of Y’s share. The new ratio among partners will be:

a) 5:4:1

b) 4:5:1

c) 1:4:5

d) 5:2:1

Ans:- d)

Explanation:-

Z surrenders to Y = 3/8 x 1/3 = 1/8

X’s new share = 5/8 – 0/1 = 5/8

Y’s new share = 3/8 – 1/8 = 2/8

New Profit sharing ratio after making base equal

= 5/8 : 2/8 : 1/8 i.e., 5 : 2 : 1

If at the time of admission, the revaluation A/c shows a profit, it should be credited to:

a) Old partners capital accounts in the old profit sharing ratio.

b) All partners capital accounts in the new profit sharing ratio

c) Old partners capital accounts in the new profit sharing ratio

d) Old partners capital accounts in the sacrificing ratio.

Ans:- a)

Revaluation Account or Profit and Loss Adjustment A/c is a

a) Real Account

b) Persona Account

c) Nominal Account

d) Asset Account

Ans:- c)

A and B are partners in the firm. C is admitted for 1/4th share of profit. He brought ₹2,00,000 as capital and ₹40,000 for goodwill. The total value of goodwill of the firm is:

a) ₹50,000

b) ₹80,000

c) ₹2,40,000

d) ₹1,60,000

Ans – d)

Ans:- d)

In case of admission of a partner, the entry for unrecorded investments will be:

a) Debit Partners Capital A/cs and Credit Investment A/c

b) Debit Revaluation A/c and Credit Investment A/c

c) Debit Investment A/c and Credit Revaluation A/c

d) None of the above

Ans – c)

Ans:- c)

X and Y are partners sharing profits in the ratio 3:2. C is admitted. X surrenders 1/6 from his share and Y surrenders 1/4th of his share. C’s share of profit will be:

a) 5/9

b) 2/13

c) 7/12

d) 4/15

Ans:- d)

Explanation:-

X surrenders = 1/6

Y surrenders = 2/5 x 1/4 = 2/20

C’s share in profit

= 1/6 + 2/20 = 4/15

When the balance sheet is prepared after the new partnership agreement, the assets and liabilities are recorded at :

a) Historical Cost

b) Current Cost

c) Realisable value

d) Revalued figures

Ans:- d)

Any change in the relationship of existing partners results in an end of the existing agreement and formation of a new one is:

a) Revaluation of partnership

b) Reconstitution of partnership

c) Realisation of partnership

d) None of these

Ans:- b)

Goodwill of a firm of A and B is valued at ₹30,000. It is appearing in the books at ₹12,000. C is admitted for 1/4share. What amount he is supposed to bring for goodwill?

a) ₹3,000

b) ₹4,500

c) ₹7,500

d) ₹10,500

Ans:- c)

Explanation:-

C’s premium for goodwill

= 30,000 x 1/4 = ₹ 7,500

The balance of Investment Fluctuation Fund after meeting the fall in the book value of the investment at the time of admission of a partner is transferred to:

a) Capital A/cs of old partners

b) Capital A/cs of all partners

c) Revaluation A/c

d) General Reserve

Ans:- a)

Explanation:-

Investment Fluctuation fund is the part of the past accumulated Profits, thus it is to be credited to old partner in old rati.

A and B are partners in a firm. They admit C as a partner with 1/5th share in the profits of the firm. C brings ₹4,00,000 as his hare of capital. Calculate the value of C’s share of goodwill on the basis of his capital, given that the combined capital of A and B after all adjustments is ₹10,00,000.

a) ₹1,20,000

b) ₹6,00,000

c) ₹14,00,000

d) ₹20,00,000

Ans:- a)

Explanation:-

Total Capital of the firm (Including Goodwill)

C’s Capital x reciprocal of his share

= 4,00,000 x 5 = ₹ 20,00,000

Total Capital of the firm (excluding Goodwill)

= A’s & B’s Capital + C’s Capital

= ₹ 10,00,000 + ₹ 4,00,000 = ₹ 14,00,000

Goodwill of the firm = ₹ 20,00,000 – ₹ 14,00,000 = ₹ 6,00,000

C’s share in goodwill = ₹ 6,00,000 x 1/5 = ₹ 1,20,000

A and B are in partnership sharing profits and losses in the ratio of 3:2. They admit C into partnership with 1/5th share which he acquires equally from A and B. Accountant has calculated a new profit sharing ratio as 5:3:2. Is accountant correct?

a) True

b) False

c) Partially True

d) Can’t say

Ans:- a)

Explanation:-

Old Profit sharing ratio of A and B is 3 : 2

A sacrifices = 1/5 x 1/2 = 1/10

B sacrifices = 1/5 x 1/2 = 1/10

A’s new share = 3/5 – 1/10 = 5/10

B’s new share = 2/5 – 1/10 = 3/10

New profit sharing ratio after making base equal

= 5/10 : 3/10 : 1/5 x 2/2

= 5 : 3 : 2

A and B are partners sharing profits in the ratio of 3:2. They admit C into the firm for 1/4th share of profits. C take 1/5th of his share from A and the rest from B. The new profit sharing ratio is:

a) 11:5:4`

b) 11:4:5

c) 11:6:5

d) 13:3:4

Ans:- b)

Explanation:-

A sacrifices = 1/4 x 1/5 = 1/20

B sacrifices = 1/4 x 4/5 = 4/20

A’s new share = 3/5 – 1/20 = 11/20

B’s new share = 2/5 – 4/20 = 4/20

new profit sharing ratio of A, B and C after making base equal

= 11/20 : 4/20 : 1/4 x 5/5

= 11 : 4 : 5

Swati and Aman were partners in a firm. Their fixed capitals were ₹9,00,000 and ₹3,00,000, respectively. They shared profits in the ratio of their capitals. Divya was admitted as a new partner for 1/4th share in the profits of the firm.

Divya brought ₹60,000 as her share of goodwill premium and ₹6,00,000 as her capital. The amount of goodwill premium credited to Swati’s account will be

a) ₹60,000

b) ₹30,000

c) ₹45,000

d) ₹15,000

Ans:- c)

Explanation:-

Sacrificing ratio of Swati & Aman is 3 : 1

Swati will be credited

= 60,000 x 3/4 = ₹ 45,000.

X and Y are partners sharing profits in the ratio 5:3. They admitted Z for 1/5th profits, for which he paid ₹60,000 against capital and ₹30,000 against goodwill. Find the capital balance for each partner taking Z’s capital as base capital.

a) ₹1,50,000; ₹60,000 and ₹60,000

b) ₹1,50,000; ₹60,000 and ₹90,000

c) ₹1,50,000; ₹90,000 and ₹60,000

d) ₹1,50,000; ₹90,000 and ₹90,000

Ans:- c)

Explanation:-

Calculation of new profit sharing ratio of X, Y and Z

Remaining share 1 – 1/5 = 4/5

X’s new share = 4/5 x 5/8 = 20/40

Y’s new share = 4/5 x 3/8 = 12/40

new profit sharing ratio after making base equal

= 20/40 : 12/40 : 1/5 x 8/8

= 5 : 3 : 2

Total Capital of the firm

= 60,000 x 5 = ₹ 3,00,000

X’s capital in new firm

= 3,00,000 x 5/10 = ₹ 1,50,000

Y’s Capital in new firm

= 3,00,000 x 3/10 = ₹ 90,000

Goodwill of the firm of X and Y is valued at ₹45,000. It is appearing in the books at ₹18,000. Z is admitted in the firm. What amount is she supposed to bring on account of goodwill?

a) ₹15,000

b) ₹6,0000

c) ₹9,0000

d) Can’t be determined

Ans:- a)

Explanation:-

Z’s premium for goodwill

= 45,000 x 1/3 = ₹ 15,000

A, B, C and D are four partners sharing profits in the ratio of 4:3:2:1. They decide to admit their manager E as a partner for 1/4th share which he acquires from A and B in the ratio of 7:3. The sacrificing ratio of A and B will be:

a) 3:7

b) 7:3

c) 1:1

d) None of these

Ans:- b)

Explanation:-

A sacrifices

= 1/4 x 7/10 = 7/40

B sacrifices

= 1/4 x 3/10 = 3/40

sacrificing ratio of A and B

= 7/40 : 3/40 i.e., 7 : 3

When premium for goodwill is paid privately by a new partner (at the time of admission), the new partner’s account is credited.

a) True

b) Partially true

c) False

d) Can’t say

Ans:- c)

Explanation:-

No entry is passed for goodwill paid privately

Remesh and Suresh are partners sharing profits in the ratio of 2:1 respectively. Ramesh Capital is ₹1,02,000 and Suresh Capital is ₹73,000. They admit Mahesh and agree to give him 1/5th share in future profit. Mahesh brings ₹14,000 as his share of goodwill. He agrees to contribute

capital in the new profit sharing ratio. How much capital will be brought by Mahesh?

a) ₹43,750

b) ₹45,000

c) ₹47,250

d) ₹48,000

Ans:- c)

Explanation:-

Combined Adjusted Capital of Ramesh and Suresh

= ₹ 1,02,000 + ₹ 73,000 + ₹ 14,000

= ₹ 1,89,000

Combined Share of Ramesh and Suresh

= 1 – 1/5 = 4/5

Total Capital in new Firm

= 1,89,000 x 5/4 = ₹ 2,36,250

Ramesh Capital

= 2,36,250 x 1/5 = ₹ 47,250

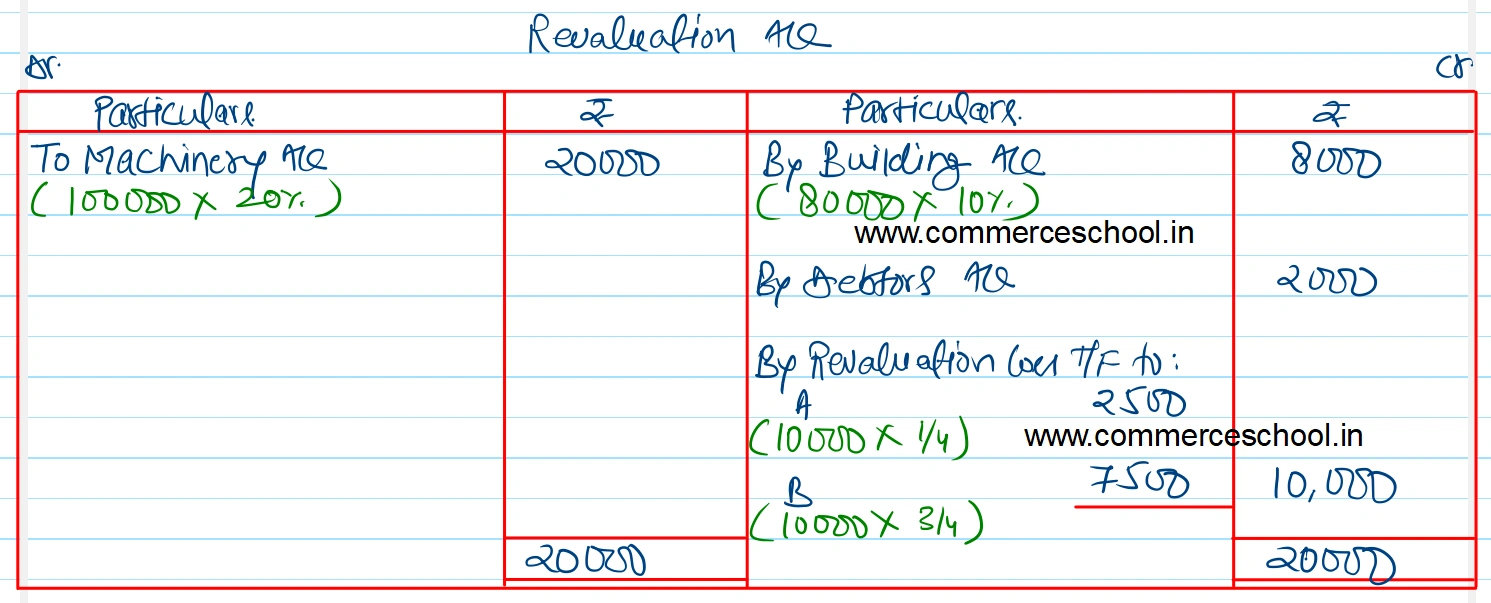

A and B are partners in a firm sharing profits/losses in a ratio of 1:3. C was admitted for 1/4th share of profit. Machinery would be depreciated by 20% (book value ₹1,00,000) and the building would be appreciated by 10% (book value ₹80,000) Unrecorded debtors of ₹2,000 would be brought in books. What was B’s and C’s share of revaluation?

a) ₹2,500, ₹7,500

b) ₹7,500, ₹2,500

c) ₹7,500, ₹0

d) ₹2,500, ₹0

Ans:- c)

Explanation:-

A and R are partners with respective capital of ₹1,50,000 and ₹1,30,000. C comes as a new partner for 1/5th share and contribute ₹1,20,000 as his capital and necessary amount for his share of goodwill in cash. The goodwill brought by C will be:

a) ₹40,000

b) ₹50,000

c) ₹1,00,000

d) ₹80,000

Ans:- a)

Explanation:-

Total Capital of the firm (including premium)

= 1,20,000 x 5 = ₹ 6,00,000

Total Capital of the firm (excluding goodwill)

= A’s Capital + R’s Capital + C’s Capital

₹ 1,50,000 + ₹ 1,30,000 + ₹ 1,20,000 = ₹ 4,00,000

Goodwill of the firm

= ₹ 6,00,000 – ₹ 4,00,000 = ₹ 2,00,000

C’s premium for Goodwill

= 2,00,000 x 1/5 = ₹ 40,000