[200] MCQs of Admission of Partner chapter Class 12

Contingency reserve, profit and loss account (credit) balance and deferred revenue expenditure account are credited to capital accounts of an old partner in the old ratio at the time of admission of new partners.

a) True

b) False

c) Partially true

d) Can’t say

Ans:- c)

Explanation:-

Only Proift and Loss A/c (credited balance) and contingency reserve is credited to old partners in old ratio. Deferred Revenue Expenditure a/c is debited to old partners in old ratio.

Disha and Abha were partners in a firm. Farad was admitted as a new partner for 1/5th share in the profits of the firm. Farad brought proportionate capital. The capitals of Disha and Abha after all adjustments were ₹64,000 and ₹46,000 respectively. Capital brought by Farad

was:

a) ₹22,000

b) ₹27,500

c) ₹55,000

d) ₹28,000

Ans:- b)

Explanation:-

Combined Adjusted Capital of Disha and Abha

= ₹ 64,000 + ₹ 46,000 = ₹ 1,10,000

Combined share of Disha and Abha

= 1 – 1/5 = 4/5

Total Capital of the firm

= 1,10,000 x 5/4 = ₹ 1,37,500

Farad’s Capital

= 1,37,500 x 1/5 = ₹ 27,500

Aditya and Shiv were partners in a firm with capitals of ₹3,00,000 and ₹2,00,000, respectively. Naina was admitted as a new partner for 1/4th share in the profits of the firm. Naina brought ₹1,20,000 for her share of goodwill premium and ₹2,40,000 for her capital. The amount of goodwill premium credited to Aditya will be

a) ₹40,000

b) ₹30,000

c) ₹72,000

d) ₹60,000

Ans:- d)

Explanation:-

Sacrificing ratio of Aditya and Shiv

= 1 : 1

Aditya will be credited

= 1,20,000 x 1/2 = ₹ 60,000

Onkar, Nitisha and Sheetal were partners sharing profits in the ratio of 3:1:1. They decided to admit Raman as a partner. On revaluation of assets, it was found that Machinery is overvalued by 25% (the Book value of Machinery was ₹6,25,000). This implies:

a) Revaluation Profit of ₹1,25,000

b) Revaluation Loss of ₹1,25,000

c) Revaluation Loss of ₹1,56,250

d) Revaluation Profit of ₹1,56,250

Ans:- b)

Explanation:-

Let the Previous value of machinery be x

As per the Question

= x + 25x/100 = 6,25,000

= 125x/100 = 6,25,000

= x = 62500000/125

= x = ₹ 5,00,000

Revaluation Loss

= ₹ 6,25,000 – ₹ 5,00,000

= ₹ 1,25,000

When the existing goodwill in books is written off at the time of admission of a new partner, the new partner’s capital accounts is not debited.

a) True

b) Partially false

c) False

d) Can’t say

Ans:- a)

A and B are in partnership sharing profits in the ratio of 3:2. They take C as a new partner. Goodwill of the firm is valued at ₹3,00,000 and C brings ₹30,000 as his share of goodwill in cash which is entirely credited to the Capital Account of A. New profit sharing ratio will

be:

a) 3:2:1

b) 6:3:1

c) 5:4:1

d) 4:5:1

Ans:- c)

Explanation:-

C’s share in Profit = 30,000/3,00,000 = 1/10

A’s new share

3/5 – 1/10 = 5/10

B’s new share

= 2/5 – 0/1 = 2/5

New Profit sharing ratio of A, B and C after making base equal

= 5/10 : 2/5 x 2/2 : 1/10

= 5 : 4 : 1

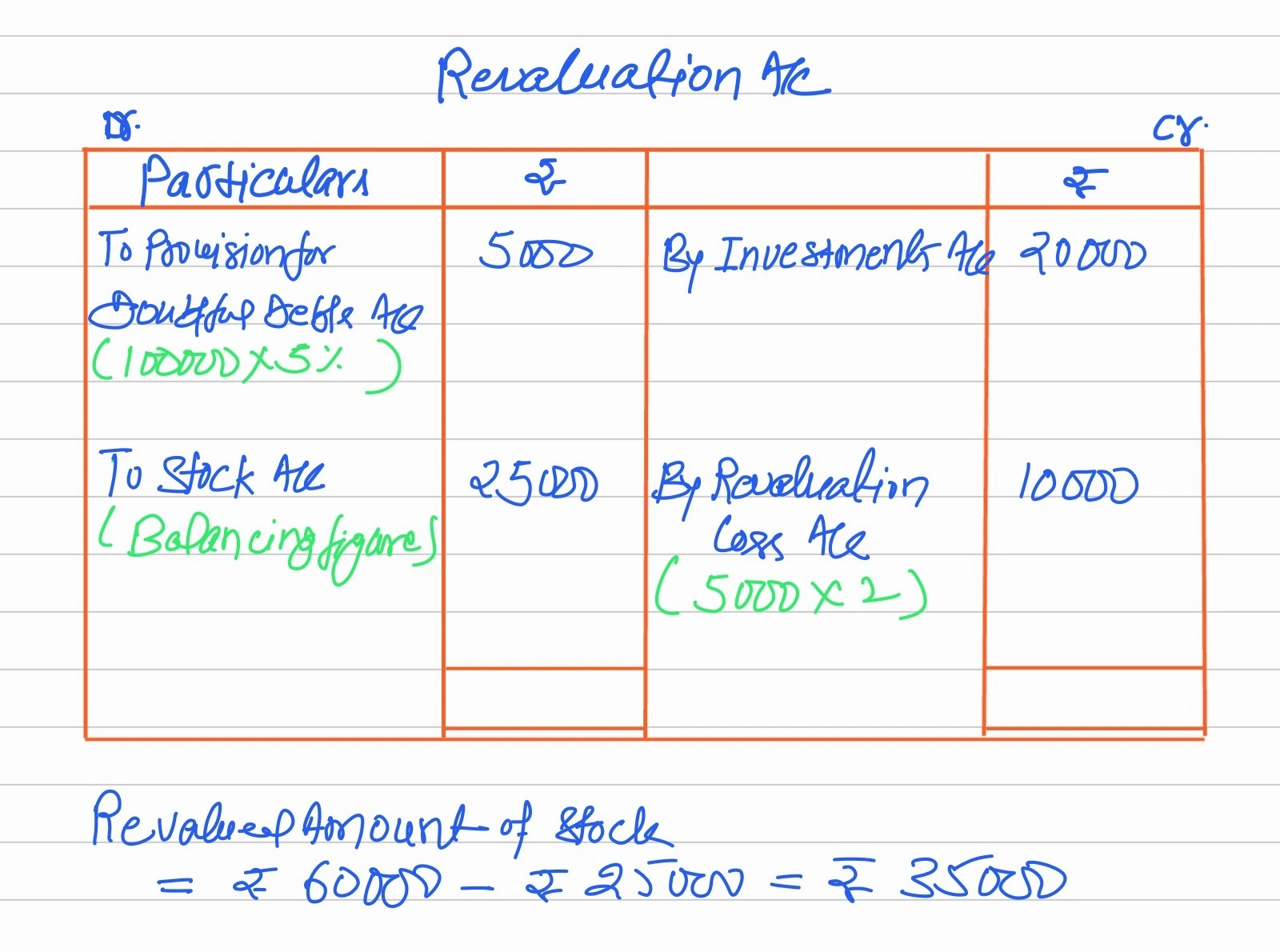

A and B are partners sharing profits and losses equally. At the time of admission of C, revaluation of assets and liabilities was done. Investments were raised by ₹20,000 and there was a provision created on debtors @5% (debtors being ₹1,00,000), the stock was also revalued, loss on realisation for A was ₹5,000. New profit sharing ratio of A:B:C would be 1:1:2. Find the revalued amount of stock, if initially, the stock was ₹60,000.

a) ₹35,000

b) ₹85,000

c) ₹55,000

d) ₹65,000

Ans:- a)

Explanation:-

A and B are partners sharing profits in the ratio 3:2. C is admitted as a new partner. A sacrificed 1/6th of his share and B sacrificed 1/8th from his share. The sacrificing ratio of A and B is:

a) 3:2

b) 3:4

c) 4:5

d) 2:5

Ans:- c)

Explanation:-

A sacrifices

= 3/5 x 1/6 = 1/10

B sacrifices = 1/8

Sacrificing ratio of A and B after making base equal

= 1/10 x 8/8 : 1/8 x 10/10

= 8 : 10 i.e., 4 : 5

Maan and Shaan are partners in firm sharing profits equally. Their capitals were ₹90,000 and ₹1,00,000 respectively. Aan was admitted for 1/3rd share in profits/losses and brought ₹1,70,000 as capital. Calculate the amount of goodwill

a) ₹5,10,000

b) ₹3,20,000

c) ₹1,50,000

d) can’t be determined

Ans:- c)

Explanation:-

Total Capital of the firm (Including Goodwill)

= Aan’s Capital x reciprocal of his share

= 1,70,000 x 3 = ₹ 5,10,000

Total Capital of the firm (Excluding goodwill)

= Maan’s Capital + Shaan’s Capital + Aan’s Capital

= ₹ 90,000 + ₹ 1,00,000 + ₹ 1,70,000

= ₹ 3,60,000

Goodwill of the firm

= ₹ 5,10,000 – ₹ 3,60,000 = ₹ 1,50,000

X and Y are partners sharing profits in the ratio of 4:3. Z is admitted for 1/5th share and he brings in ₹1,40,000 as his share of goodwill in cash of which ₹1,20,000 is credited to X and the remaining amount to Y. New profit sharing ratio will be:

a) 4:3:5

b) 2:2:1

c) 1:2:2

d) 2:1:2

Ans:- b)

Explanation:-

Sacrificing ratio of X and Y is

= 1,20,000 : 20,000

= 6 : 1

X sacrifices = 1/5 x 6/7 = 6/35

Y Sacrifices = 1/5 x 1/7 = 1/35

X’s new share

= 4/7 – 6/35 = 14/35

Y’s new share

= 3/7 – 1/35 = 14/35

New Profit sharing ratio after making base equal

= 14/35 : 14/35 : 1/5 x 7/7

= 14 : 14 : 7 i.e., 2 : 2 : 1

Zafar and Zubin are partners with a profit-sharing ratio as 2:3. They admitted Zannat who brought ₹80,000 as goodwill which was credited to Zafar’s and Zubin’s Capital account as ₹60,000 and ₹20,000 respectively goodwill of the firm is ₹4,00,000 calculate new profit sharing ratio.

a) 2:3:5

b) 5:11:4

c) 5:12:3

d) Can’t be determined

Ans:- b)

Explanation:-

Zannat’s Share in Profit

= Zannat’s Premium for Goodwill/Goodwill of the firm

= 80,000/4,00,000 = 1/5br>Sacrificing ratio of Zafar and Zubin

= 60,000 : 20,000 = 3 : 1

Zafar sacrifices 1/5 x 3/4 = 3/20

Zubin Sacrifices = 1/5 x 1/4 = 1/20

Zafar’s new share

= 2/5 – 3/20 = 5/20

Zubin’s new share = 3/5 – 1/20 = 11/20

New Profit sharing ratio after making base equal

= 5/20 : 11/20 : 1/5 x 4/4

= 5 : 11 : 4

On admission of a partner, an increase in provision for doubtful debts will be _________.

a) Credited to Revaluation A/c

b) Debited to Revaluation A/c

c) Debited to Capital A/c

d) Credited to cash A/c

Ans:- b)

According to AS – 10, the value of goodwill should be adjusted through the capital accounts of the partners.

a) True

b) False

c) Partially true

d) Can’t say

Ans:- c)

Explanation:-

While AS – 10 does emphasize the adjustment of goodwill through the capital accounts of the partners, it does not restrict the treatment of goodwill solely to capital accounts. Goodwill can also be adjusted through other methods, such as the revaluation of assets and liabilities or the creation of a goodwill reserve.

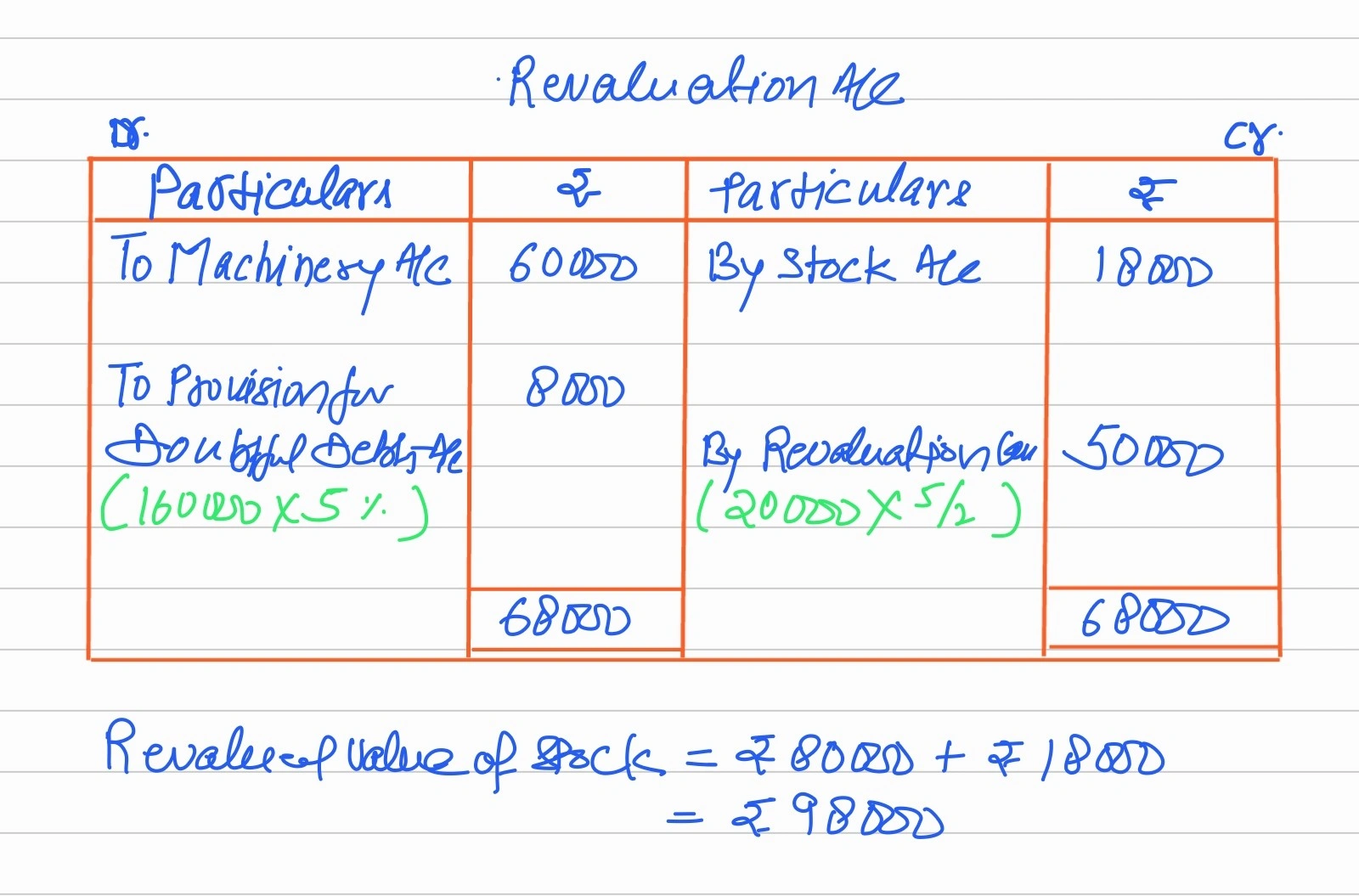

A and B are partners sharing profits in the ratio of 2:3. Their Balance Sheet shows Machinery at ₹2,00,000; Stock at ₹80,000 and Debtors at ₹1,60,000. C is admitted and a new profit sharing ratio is agreed at 6:9:5. Machinery is revalued at ₹1,40,000 and a provision is made for doubtful debts @5%. A’s share in loss on revaluation amounts to ₹20,000. Revalued value of the stock will be:

a) ₹62,000

b) ₹1,00,000

c) ₹60,000

d) ₹98,000

Ans:- d)

Explanation:-

P and Q are partners sharing profit or loss in a ratio of 2:1. A surrenders 1/4th of his share and B surrenders 1/3rd of his share in favour of R a new partner. What will be R share?

a) 7/12

b) 5/12

c) 13/36

d) 5/18

Ans:- d)

Explanation:-

P sacrifices

= 2/3 x 1/4 = 2/12

Q sacrifices

= 1/3 x 1/3 = 1/9

R’s share

= 2/12 + 1/9 = 5/18

X and Y are partners sharing profits and losses in the ratio 3:2. Z is admitted for 1/6th share which he gets from X and Y in the ratio 3:2. The new profit sharing ratio of X, Y and Z will be:

a) 1:1:1

b) 3:2:1

c) 12:8:4

d) None of these

Ans:- b)

Explanation:-

X sacrifices = 1/6 x 3/5 = 3/30

Y sacrifices = 1/6 x 2/5 = 2/30

X’s new share

= 3/5 – 3/30 = 15/30

Y’s new share

= 2/5 – 2/30 = 10/30

New profit sharing ratio after making base equal

= 15/30 : 10/30 : 1/6 x 5/5

= 3 : 2 : 1

On the admission of a new partner, the old partnership continues.

a) True

b) Partially true

c) False

d) Can’t say

Ans:- c)

Explanation:-

on the admission of a new partner, the old partnership comes to an end and new partnership firm constituted. but the firm continues to exist.

A B and C are partners sharing profits in a ratio of 3:2:1. They agree to admit D into the firm. A, B and C agreed to give 1/3rd, 1/6th, 1/9th share of their profit. The share of profit of D will be:

a) 1/10

b) 11/54

c) 12/54

d) 13/54

Ans:- d)

Explanation:-

A sacrifices = 3/6 x 1/3 = 1/6

B sacrifices = 2/6 x 1/6 = 1/18

C sacrifices = 1/6 x 1/9 = 1/54

D’s share in Profit

= 1/6 + 1/18 + 1/54 = 13/54

A and B are partners in a firm having a capital of ₹54,000 and ₹36,000 respectively. They admitted C for 1/3rd share in the profits. C brought the proportionate amount of capital. The capital brought in by C would be

a) ₹90,000

b) ₹45,000

c) ₹5,4000

d) ₹36,600

Ans:- b)

Explanation:-

Combined Capital of A and B is

= ₹ 54,000 + ₹ 36,000

= ₹ 90,000

Combined Share of A and B

= 1 – 1/3 = 2/3

Total Capital of the firm

= Combined Capital of A and B x reciprocal of combined share

= 90,000 x 3/2 = ₹ 1,35,000

C’s Capital

= 1,35,000 x 1/3 = ₹ 45,000

X and Y are partners sharing profits and losses in the ratio 3:2. Z is admitted for 1/6th share which he gets from X and Y in the ratio 3:2. The new profit sharing ratio of X, Y and Z will be:

a) 1:1:1

b) 3:2:1

c) 12:8:4

d) None of these

Ans:- b)

Explanation:-

X sacrifices = 1/6 x 3/5 = 3/30

Y sacrifices = 1/6 x 2/5 = 2/30

X’s new share

= 3/5 – 3/30 = 15/30

Y’s new share

= 2/5 – 2/30 = 10/30

New profit sharing ratio after making base equal

= 15/30 : 10/30 : 1/6 x 5/5

= i.e., 3 : 2 : 1

Shishu and Pranav are partners in a firm and share profits and losses in the ratio of 3:2. Extract of their balance sheet on 31st March 2020 is as follows

Liabilities – Provision for Doubtful Debts ₹4,000

Assets – Debtors ₹10,000

At the time of admission of Shiv as a partner, if provision for doubtful debts is to be maintained at 10% of receivables as on 31st March 2020, when what amount of provision for doubtful debts will be shown in the reconstituted balance sheet?

a) ₹1,000

b) ₹3,000

c) ₹400

d) ₹6,000

Ans:- a)

Explanation:-

= 10,000 x 10% = ₹ 1,000

When incoming partner acquires his share from existing partners in their profit sharing ratio, the steps for calculation of new profit sharing ratio are given as

i) Calculate old partner’s new share as part of the combined share

ii) Convert the new shares of all partners and find out the new profit sharing ratio

iii) Calculate the combined share of old partners in the new firm by deducting new partners share from 1

Arrange the steps in the correct order

a) i), iii), ii)

b) iii), i), ii)

c) ii), iii),i)

d) iii), ii), i)

Ans:- b)

X and Y are partners sharing profits in the ratio 2:3. They admitted Z for 1/5th share of profits, for which he paid ₹1,20,000 against capital and ₹60,000 as goodwill. Find the capital balances for each partner taking Z’s capital as base capital.

a) ₹3,00,000, ₹1,20,000, ₹1,20,000

b) ₹3,00,000, ₹1,20,000, ₹1,80,000

c) ₹1,92,000, ₹2,88,000, ₹1,20,000

d) ₹3,00,000, ₹1,80,000, ₹1,80,000

Ans:- c)

Explanation:-

Calculation of New Profit sharing ratio of X and Y

Remaining Share = 1 – 1/5 = 4/5

X’s new share = 4/5 x 2/5 = 8/25

Y’s new share = 4/5 x 3/5 = 12/25

New profit sharing ratio of X, Y and Z

= 8/25 : 12/25 : 1/5 x 5/5

= 8 : 12 : 5

Total Capital of the firm

= 1,20,000 x 5 = ₹ 6,00,000

X’s Capital

= 6,00,000 x 8/25 = ₹ 1,92,000

Y’s Capital

= 6,00,000 x 12/25 = ₹ 2,88,000

A and B are partners sharing profits and losses in the ratio of 2:1. C is admitted and the profit-sharing ratio becomes 4:3:2. Goodwill is valued at ₹94,500. C brings required goodwill in cash. Calculate the amount of goodwill to be credited to A and B is:

a) ₹14,000 and ₹7,000 respectively

b) ₹1,05,000 each

c) ₹21,000 to A

d) ₹21,000 to B

Ans:- c)

Explanation:-

C’s Premium for Goodwill

= 94,500 x 2/9 = ₹ 21,000

A sacrifices = 2/3 – 4/9 = 2/9

B sacrifices = 1/3 – 3/9 = 0/9

A will be credited as he only sacrifices

A, B, C and D are partners. A and B share 2/3rd of profits equally and C and D share remaining profits in the ratio of 3:2. Find the profit-sharing ratio of A. B, C and D.

a) 5:5:3:2

b) 7:7:6:4

c) 2.5:2.5:8:6

d) 3:9:8:3

Ans:- a)

Explanation:-

A’s share = 2/3 x 1/2 = 2/6

B’s share = 2/3 x 1/2 = 2/6

C’s share = 1/3 x 3/5 = 3/15

D’s share = 1/3 x 2/5 = 2/15

Profit sharing ratio of A, B, C and D after making base equal

= 2/6 x 5/5 : 2/6 x 5/5 : 3/15 x 2/2 : 2/15 x 2/2

= 10 : 10 : 6 : 4

i.e., 5 : 5 : 3 : 2

A, B, C, D are in partnership sharing profit and losses in the ratio of 1:2:3:4. E joins for 25% share. The new profit sharing ratio among A, B, C, D will be 4:3:2:1 what is the new profit sharing ratio among A, B, C, D, E?

a) 4:3:2:1:4

b) 8:6:4:2:8

c) 12:9:6:3:10

d) Can’t be determined

Ans:- c)

Explanation:-

Remaining Share = 2 – 25/100 = 3/4

A’s new share = 3/4 x 4/10 = 12/40

B’s new share = 3/4 x 3/10 = 9/40

C’s new share = 3/4 x 2/10 = 6/40

D’s new share = 3/4 x 1/10 = 3/40

New profit sharing ratio after making base equal

= 12/40 : 9/40 : 6/40 : 3/40 : 1/4 x 10/10

= i.e., 12 : 9 : 6 : 3 : 10

Sacrificing ratio is used to distribute _______ in case of admission of a partner:

a) Reserves

b) Goodwill

c) Revaluation Profit

d) Balance in Profit and Loss Account

Ans:- b)

On the admission of a new partner:

a) Old firm is dissolved

b) old partnership is dissolved

c) both old partnership and firm are dissolved

d) neither partnership nor firm is dissolved

Ans:- b)

Explanation:-

On the admission of a new partner old partnership comes to an end but firm continues to exist.

The new partner, at the time of admission, may acquire his share from old partners in

a) Old profit sharing ratio

b) Some agreed ratio

c) particular fraction from some of the partners

d) All of these

Ans:- d)

X and Y are partners in a firm with the capital of ₹1,80,000 and ₹2,00,000. Z was admitted for 1/3rd share in profits and brings ₹3,40,000 as capital, calculate the amount of goodwill:

a) ₹2,40,000

b) ₹1,00,000

c) ₹1,50,000

d) ₹3,00,000

Ans:- d)

Explanation:-

Total Capital of the firm (Including goodwill)

= Z’s Capital x reciprocal of his share

= 3,40,000 x 3 = ₹ 10,20,000

Total Capital of the firm (excluding goodwill)

= X’s Capital + Y’s Capital + Z’s Capital

= ₹ 1,80,000 + ₹ 2,00,000 + ₹ 3,40,000

= ₹ 7,20,000

Goodwill of the firm

= ₹ 10,20,000 – ₹ 7,20,000 = ₹ 3,00,000

Which of the following is not a right of a newly admitted partner?

a) Right to share profits of the firm

b) Right to inspect the books of accounts

c) Right to participate in affairs of business

d) None of these

Ans:- d)

A and B are partners sharing profits and losses in the ratio of 5:3. On admission, C brings ₹70,000 as cash and ₹43,000 against Goodwill. New profit ratio between A, B and C is 7:5:4. The sacrificing ratio of A and B is:

a) 3:1

b) 1:3

c) 4:5

d) 5:9

Ans:- a)

Explanation:-

A sacrifices = 5/8 – 7/16 = 3/16

B sacrificies = 3/8 – 5/16 = 1/16

sacrificing ratio of A and B

= 3/16 : 1/16 i.e., 3 : 1

The ratio in which a partner receives a rise in his share of profits is known as:

a) New ratio

b) Sacrificing ratio

c) Capital ratio

d) Gaining ratio

Ans:- d)

Ram and Shyam are partners sharing profits in the ratio of 3:2. They admit Tarun as a new partner. After his admission, the profit-sharing ratio becomes 5:5:3. On the date of Tarun’s Admission, the goodwill of the firm is valued at ₹13,00,000. The amount of goodwill brought in by Tarun will be

a) ₹5,00,000

b) ₹10,00,000

c) ₹3,00,000

d) ₹13,00,000

Ans:- c)

Explanation:-

Tarun’s Premium for Goodwill

= 13,00,000 x 3/13 = ₹ 3,00,000

A and B are partners in a firm having capitals of ₹54,000 and ₹36,000 respectively. They admitted C for 1/3rd share in the profits. C brought the proportionate amount of capital. The Capital brought in by C would be:

a) ₹90,000

b) ₹45,000

c) ₹54,000

d) ₹36,000

Ans:- b)

Explanation:-

Combined Capital of A and B

= ₹ 54,000 + ₹ 36,000 = ₹ 90,000

Combined Share of A and B

= 1 – 1/3 = 2/3

Total Capital of the firm

= 90,000 x 3/2 = ₹ 1,35,000

C’s Capital

= 1,35,000 x 1/3 = ₹ 45,000

X and Y are sharing profits and losses in the ratio of 3:2. Z is admitted with 1/5th share in profits of the firm which he gets entirely from X. Find out the new profit sharing ratio.

a) 12:8:5

b) 8:12:5

c) 2:2:1

d) 2:2:2

Ans:- c)

Explanation:-

X’s new share = 3/5 – 1/5 = 2/5

Y’s new share = 2/5 – 0/1 = 2/5

new profit sharing ratio of X, Y and Z

= 2/5 : 2/5 : 1/5 i.e., 2 : 2 :1

The ratio in which a partner surrenders his share in favour of a partner is known as:

a) New profit sharing ratio

b) Sacrificing ratio

c) Gaining ratio

d) Capital ratio

Ans:- b)

P and Q are in partnership sharing profits and losses in the ratio of 2:1 respectively. R joins the partnership for 1/5th share. The sacrificing ratio of P and Q after R’s admission is:

a) 2:1

b) 3:2

c) 4:3

d) 5:2

Ans:- a)

Explanation:-

In the absence of any additional information about the share of new partner. The sacrificing ratio is always equal to the old ratio.

Nikki and Tikki were partners sharing profits and losses in the ratio of 3:2. On 31st December 2019, the extract of their balance sheet is as follows:

Assets – Land and Building – 1,00,000

At the time of admission of new partner Chikki, if the value of land and building is to be appreciated by 10%, then what will be the amount of Land and Building which is to be shown in the new balance sheet?

a) ₹90,000

b) ₹1,00,000

c) ₹10,000

d) ₹1,10,000

Ans:- d)

Explanation:-

Value of Land and Building in new Balance Sheet

= 1,00,000 + 10% x 1,00,000

= ₹ 1,10,000

X, Y and Z are partners in the ratio of 3:2:1. W is admitted with 1/6th share in profits. Z would retain his original share. The new profit sharing ratio of X, Y and A and W is:

a) 4:3:2:2

b) 3:3:1:1

c) 12:8:5:5

d) 5:2:1:1

Ans:- c)

Explanation:-

Remaining Share after W and Z share

= 1 – 1/6 – 1/6 = 2/3

remaining share would be distributed by X and Y in their profit sharing ratio i.e., 3 : 2

X’s new share = 2/3 x 3/5 = 6/15

Y’s new share = 2/3 x 2/5 = 4/15

New profit sharing ratio after making base equal

= 6/15 : 4/15 : 1/6 x 5/5 : 1/6 x 5/5

= i.e., 12 ; 8 : 5 : 5

Mona and Tina were partners in firm sharing profits in the ratio of 3:2. Naina was admitted with 1/6th share in the profits of the firm. At the time of admission, Workmen’s Compensation Reserve appeared in the Balance Sheet of the firm at ₹32,000. The claim on account of workmen’s compensation was determined at ₹40,000. Excess of claim over the reserve will be:

a) Credited to Revaluation Account

b) Debited to Revaluation Account

c) Credited to old partner’s capital Accounts

d) Debited to old partner’s capital Accounts

Ans:- b)

Surya and Ishaan are partners. They admitted Hardik, At the time, there was a debit balance of profit and loss account in the balance sheet of ₹66,000. Journalise.

a) Surya’s Capital A/c Dr 33,000

Ishaan’s Capital A/c Dr 33,000

To Profit and Loss A/c 66,000

b) Profit and Loss A/c Dr 66,000

To Surya’s Capital A/c 33,000

To Ishaan’s Capital A/c 33,000

c) Surya’s Capital A/c Dr 22,000

Ishaan’s Capital A/c Dr 22,000

Hardik’s Capital A/c Dr 22,000

To Profit and Loss A/c 66,000

d) Profit and Loss A/c Dr 66,000

To Surya’s Capital A/c 22,000

To Ishaan’s Capital A/c 22,000

To Hardik’s Capital A/c 22,000

Ans:- a)

In the case of workmen Compensation Reserve, if the amount claimed is more than the amount lying in WCR, then the shorfall will be recorded in :

a) Revaluation Account

b) Partner’s Capital Account

c) Balance Sheet

d) None of these

Ans:- a)

A and B are partners sharing profits and losses in the ratio of 5:4. C is admitted for 1/5th share. A and B decide to share equally in future. Sacrificing ratio will be.

a) 5:4

b) 2:7

c) 7:2

d) 1:1

Ans:- c)

Explanation:-

Remaining Share = 1 – 1/5 = 4/5

It would be distributed by A and B in 1 : 1

A’s new share = 4/5 x 1/2 = 4/10

B’s new share = 4/5 x 1/2 = 4/10

new profit sharing ratio after making base equal

= 4/10 : 4/10 : 1/5 x 2/2

= 4 : 4 : 2 = 2 : 2 : 1

A’s sacrifice = 5/9 – 2/5 = 7/45

B’s sacrifice = 4/9 – 2/5 = 2/45

sacrificing ratio of A and B is

= 7/45 : 2/45 = 7 : 2

Dana and Lana were sharing profits in the ratio of 2:1. Jana was admitted for 1/3rd share and claim on workmen compensation reserve was ₹10,000. Journalise.

Liabilities – Workmens Compensation Reserve – ₹18,000

a) Workmen Compensation Reserve A/c Dr 18,000

To Dana’s Capital A/c 12,000

To Lana’s Capital A/c 6,000

b) Workmen Compensation Reserve A/c Dr 18,000

To Dana’s Capital A/c 8,000

To Lana’s Capital A/c 4,000

To Jana’s Capital A/c 6,000

c) Workmen Compensation Reserve A/c Dr 18,000

To Claim on Workmen compensation A/c 10,000

To Dana’s Capital A/c 5,333

to Lana’s Capital A/c 2,667

d) Workmen Compensation Reserve A/c Dr 10,000

To Claim on Workmen Compensation A/c 3,556

To Dana’s Capital A/c 1,778

To Jana’s Capital A/c 2,666

Ans:- c)

X and Y are partners in a firm sharing profits and losses in the proportion of 2:1. They admit a new partner Z for 1/6th share in profit. What is the new profit sharing ratio of X, Y and Z?

a) 5:3:10

b) 2:1:6

c) 1:1:1

d) 10:5:3

Ans:- d)

Explanation:-

Remaining Share = 1 – 1/6 = 5/6

X’s new share = 5/6 x 2/3 = 10/18

Y’s new share = 5/6 x 1/3 = 5/18

new profit sharing ratio after making base equal

= 10/18 : 5/18 : 1/6 x 3/3

= 10 : 5 : 3

The Emi, Nemi and Kimi are partners sharing profits in the ratio of 5:3:2. They have admitted Vimi into the partnership for 1/6th share. An Extract of their balance sheet on 1st April 2020 is as follows

Liabilities – Investment Fluctuation Fund ₹27,000

Assets – Investment (Cost) ₹3,00,000

If the market value of investments is ₹2,90,000, then the investment fluctuation fund will be credited to partners

a) ₹27,000

b) ₹20,000

c) ₹17,000

d) ₹13,000

Ans:- c)

Sun and Star were partners in a firm sharing profits in the ratio of 2:1. Moon was admitted as a new partner in the firm. The new profit sharing ratio was 3:3:2. Moon brought the following assets towards his share of goodwill and his capital:

Machinery ₹2,00,000; Furniture ₹1,20,000; Stock ₹80,000; Cash ₹50,000. If his capital is considered as ₹3,80,000, the goodwill of the firm

will be:

a) ₹70,000

b) ₹2,80,000

c) ₹4,50,000

d) ₹1,40,000

Ans:- b)

Explanation:-

Machinery A/c Dr. 2,00,000

Furniture A/c Dr. 1,20,000

Stock A/c Dr. 80,000

Cash A/c Dr. 50,000

To Moon’s Capital A/c 3,80,000

To Premium for goodwill A/c 70,000

Goodwill of the firm

= Moon’s premium for goodwill x reciprocal of his share

= 70,000 x 8/2 = ₹ 2,80,000

A and B are partners in the ratio of 3:1. C was admitted for 1/5th share and he could not bring his share of goodwill. Goodwill of the firm is valued at ₹1,00,000. Journalise.

a) Premium for Goodwill A/c Dr 1,00,000

To A’s Capital A/c 75,000

To B’s Capital A/c 25,000

b) C’s Capital A/c Dr 1,00,000

To A’s Capital A/c 75,000

To B’s Capital A/c 25,000

c) C’s Capital A/c Dr 20,000

To A’s Capital A/c 10,000

To B’s Capital A/c 10,000

d) C’s Capital A/c Dr 20,000

To A’s Capital A/c 15,000

To B’s Capital A/c 5,000

Ans:- d)

Explanation:-

C’s Premium for Goodwill

= 1,00,000 x 1/5 = ₹ 20,000

it would be credited to A and B in their sacrificing ratio i.e. 3 : 1

A will be credited

= 20,000 x 3/4 = ₹ 15,000

B will be credited

= 20,000 x 1/4 = ₹ 5,000

Journal Entry

C’s Current A/c Dr. 20,000

To A’s Capital A/c 15,000

To B’s Capital A/c 5,000

X and Y are partners in a firm. They admit Z for 1/3 share. Z brought ₹2,00,000 as his capital and ₹60,000 for premium. Journalise the transaction.

a) Bank A/c Dr 2,60,000

To Z’s capital 2,00,000

To Premium for Goodwill A/c 60,000

b) Z’s Capital A/c Dr 2,00,000

To Bank A/c 2,00,000

c) Z’s Capital A/c Dr. 2,00,000

Premium for Goodwill A/c 60,000

To Bank A/c 2,60,000

d) Bank A/c Dr 2,00,000

To Z’s Capital A/c 2,00,000

Ans:- a)

A and B are partners sharing profits in an equal ratio. A’s capital is ₹90,000 and B’s capital is ₹60,000. They admit C and agree to give 1/5th share in future profit. C brings ₹70,000 as his capital. Value of hidden goodwill at the time of admission of C is:

a) ₹70,000

b) ₹1,30,000

c) ₹3,50,000

d) ₹1,50,000

Ans:- b)

Explanation:-

Total Capital of the firm (including goodwill)

= C’s Capital x reciprocal of his share

= 70,000 x 5 = ₹ 3,50,000

Total Capital of the firm (excluding goodwill)

= A’s Capital + B’s Capital + C’s Capital

= ₹ 90,000 + ₹ 60,000 + ₹ 70,000

= ₹ 2,20,000

Goodwill of the firm

= ₹ 3,50,000 – ₹ 2,20,000

= ₹ 1,30,000

A and B are two partners sharing profits in the ratio of 2:1. C, a new partner admitted for 1/4th share. At the time of admission, loss from revaluation is ₹9,000. Pass a necessary journal entry for distribution of loss between the partners?

a) A’s Capital A/c Dr 6,000

B’s Capital A/c Dr 3,000

To Revaluation A/c 9,000

b) A’s Capital A/c Dr 9,000

To B’s capital A/c 9,000

c) Revaluation A/c Dr 9,000

To A’s Capital A/c 6,000

To B’s Capital A/c 3,000

d) B’s Capital A/c 9,000

To A’s Capital A/c 9,000

Ans:- a)