[DK Goel] Q. 23, 24 Retirement of Partner Solutions Class 12 CBSE (2026-27)

Here are the solutions of Question number 23 and 24 of Retirement of Partner chapter 5 of DK Goel Class 12 CBSE (2026-27)

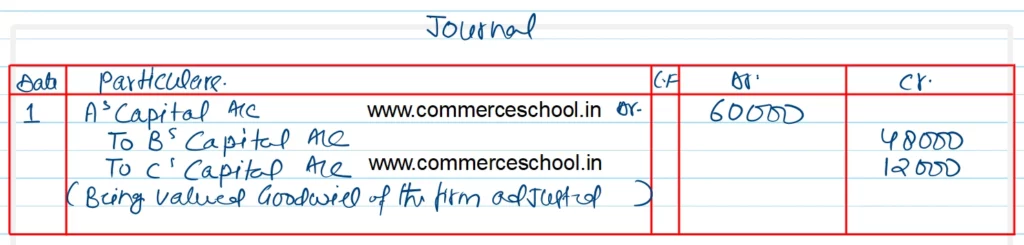

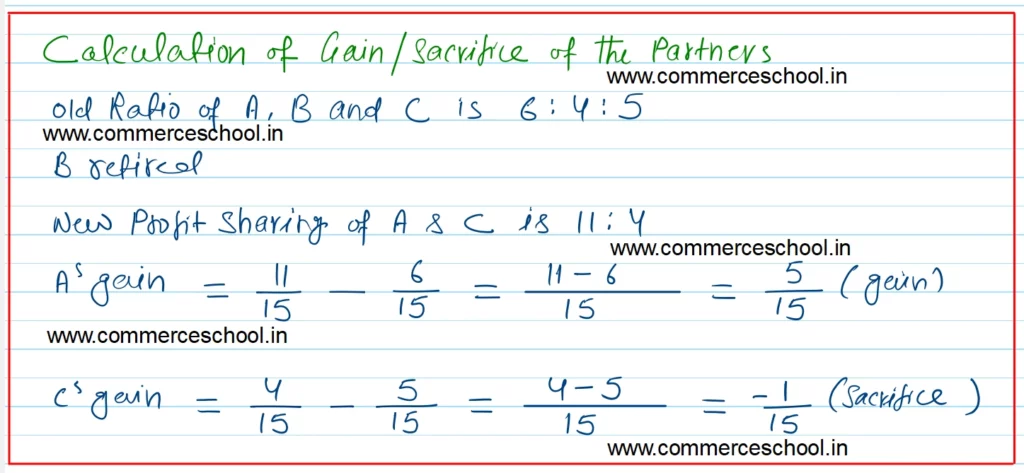

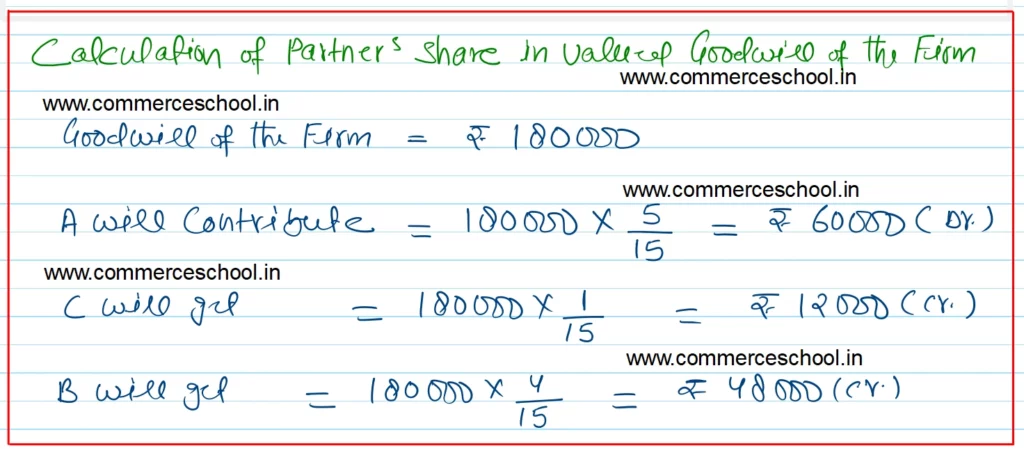

Q. 23 (A). A, B and C were partners sharing profits in the ratio of 6 : 4 : 5. Their capitals were A – ₹ 1,00,000, B – ₹ 80,000 and C – ₹ 60,000. On 1st April 2023, B retired from the firm and the new profit sharing ratio between A and C was decided as 11 : 4. On B’s retirement the goodwill of the firm was valued at ₹ 1,80,000. Showing your calculations clearly pass necessary journal entry for the treatment of goodwill on B’s retirement.

[Ans. Only A gains 5/15. C has also sacrificed 1/15. Hence A will be debited by ₹ 60,000 and B and C will be credited by ₹ 48,000 and ₹ 12,000 respectively.]

Solution:-

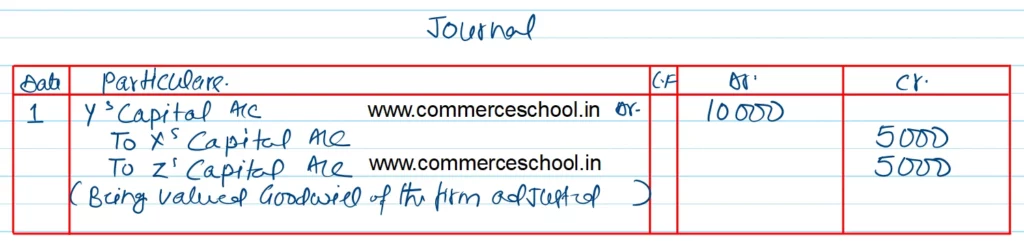

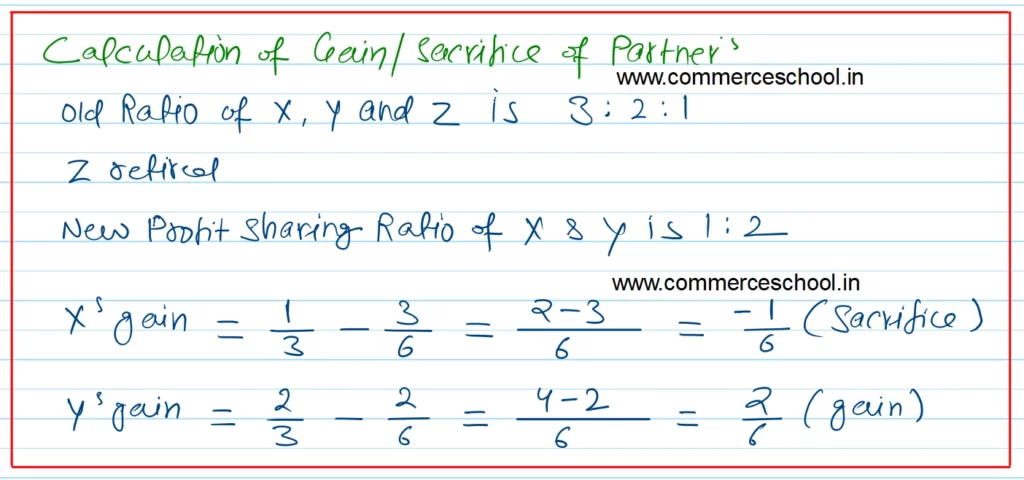

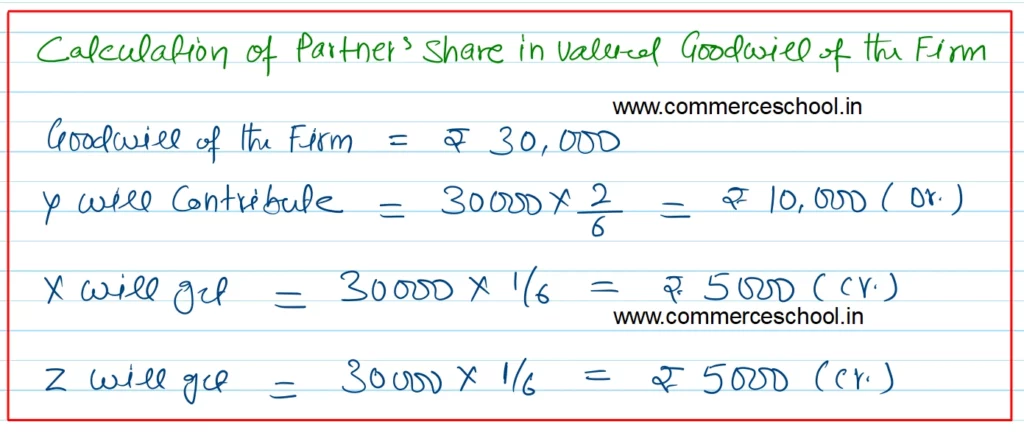

Q. 23 (B). X, Y and Z were partners in a firm sharing profits in the ratio of 3 : 2 : 1. Z retired and the new profit sharing ratio between X and Y was 1 : 2. On Z’s retirement the goodwill of the firm was valued at ₹ 30,000. Pass necessary journal entry for the treatment of goodwill on Z’s retirement.

[Ans. Only Y gains 2/6, X has also sacrificed 1/6. Hence Y will be debited from ₹ 10,000 and X and Z will be credited from ₹ 5,000 each.]

Solution:-

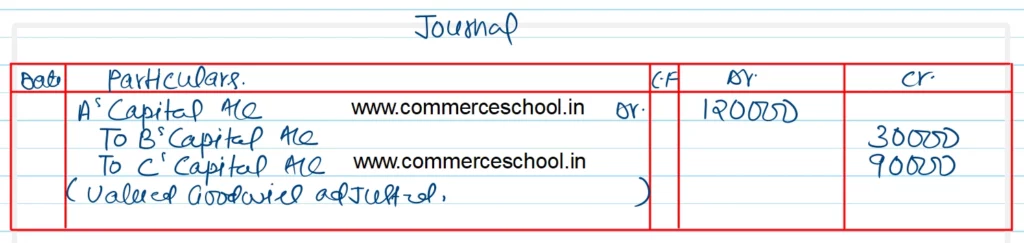

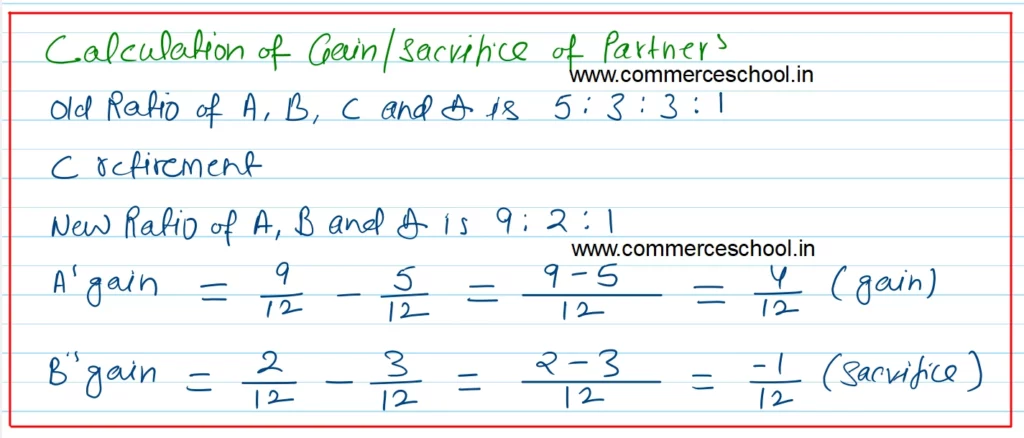

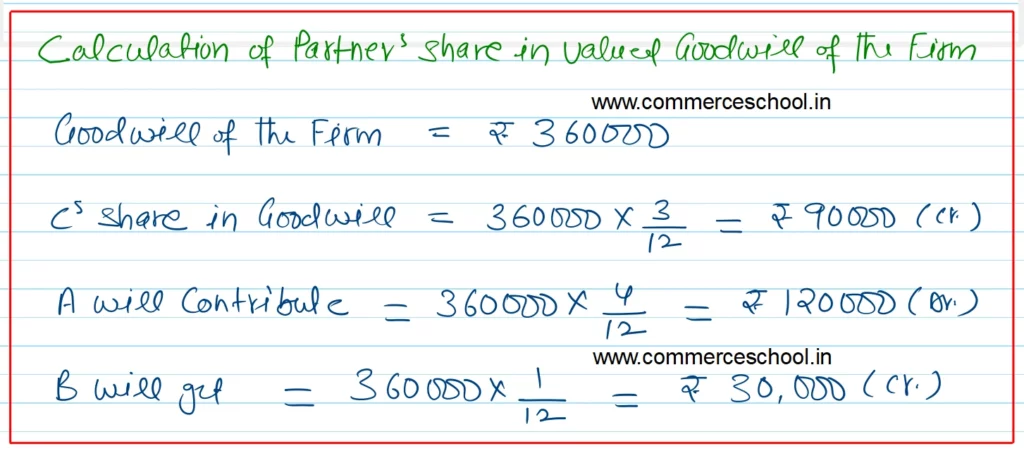

Q. 24. A, B, C and D are partners sharing profits in the ratio of 5 : 3 : 3 : 1. On the retirement of C, goodwill was valued at ₹ 3,60,000. C’s share of goodwill will be adjusted into the Capital accounts of A, B and D. Pass necessary entry for the treatment of goodwill when new profit sharing ratio is decided at 9 : 2 : 1.

[Ans. Only A gains 4/12. B has also sacrificed 1/12. Hence A will be debited by ₹ 1,20,000 and B and C will be credited by ₹ 30,000 and ₹ 90,000 respectively.]

Solution:-