[DK Goel] Q. 95, 96 Retirement of Partner Solutions Class 12 CBSE (2026-27)

Here are the solutions of Question number 95 and 96 of Retirement of Partner chapter 5 of DK Goel Class 12 CBSE (2026-27)

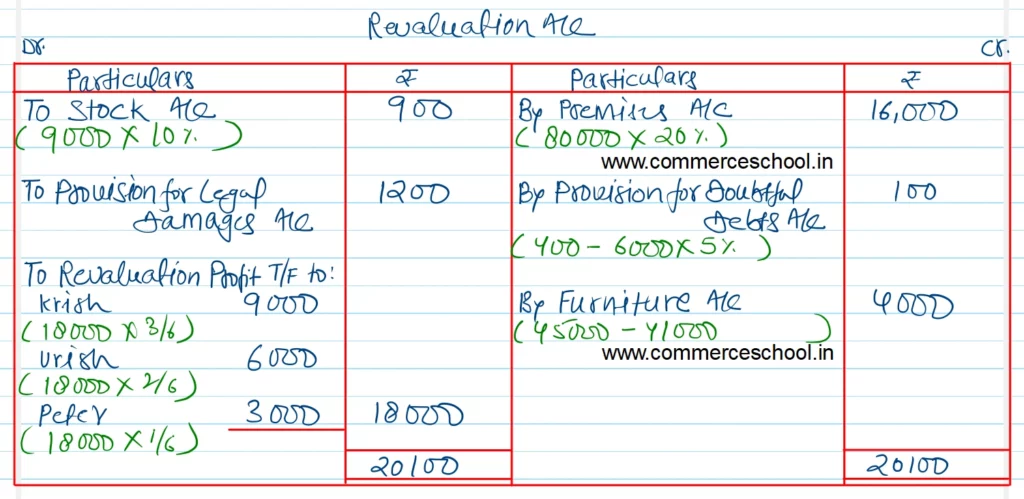

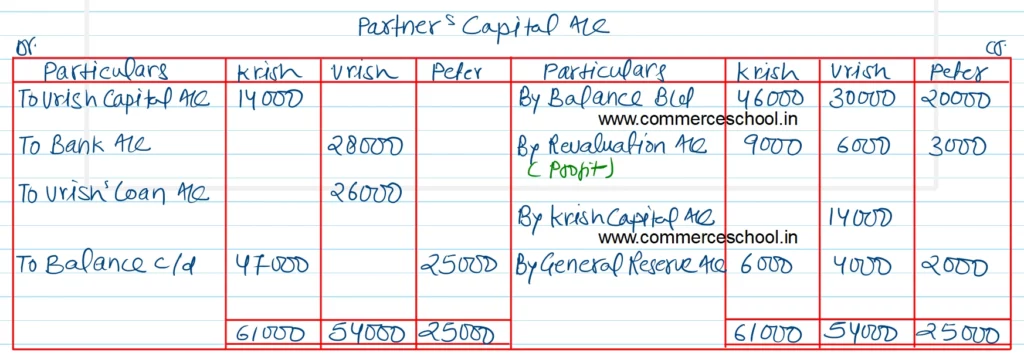

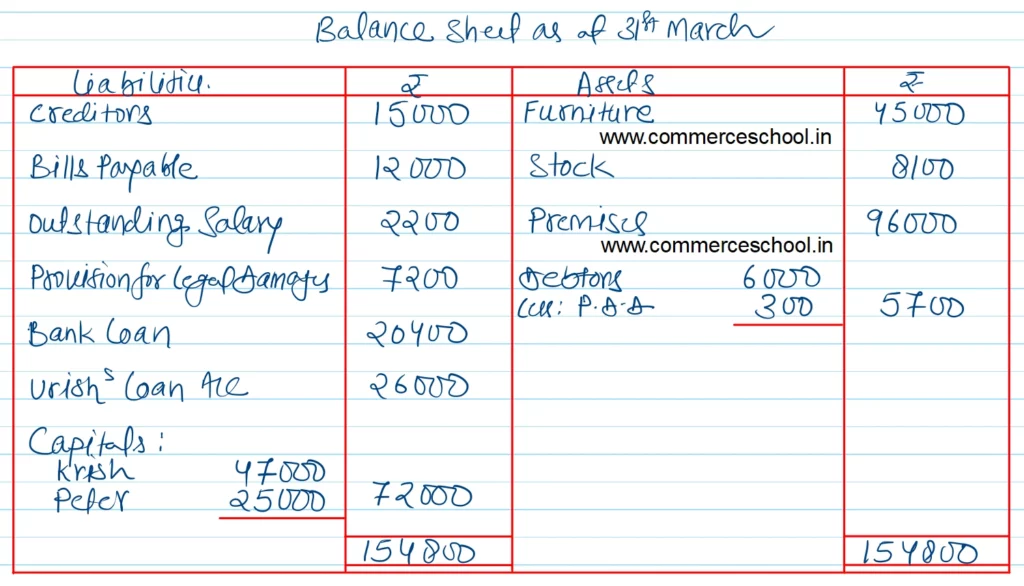

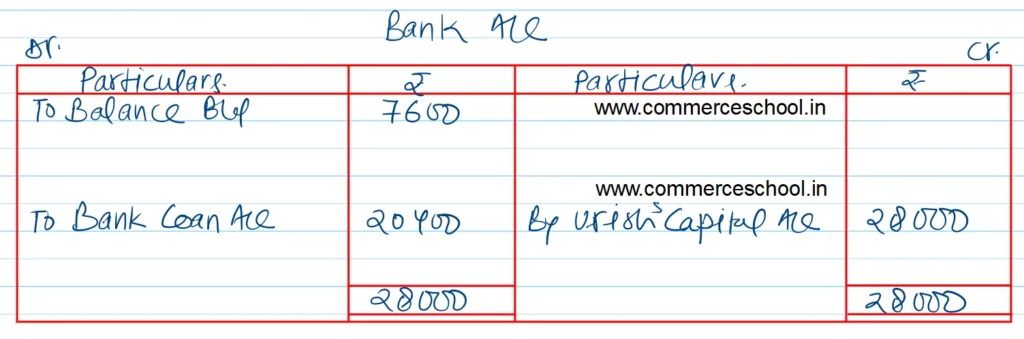

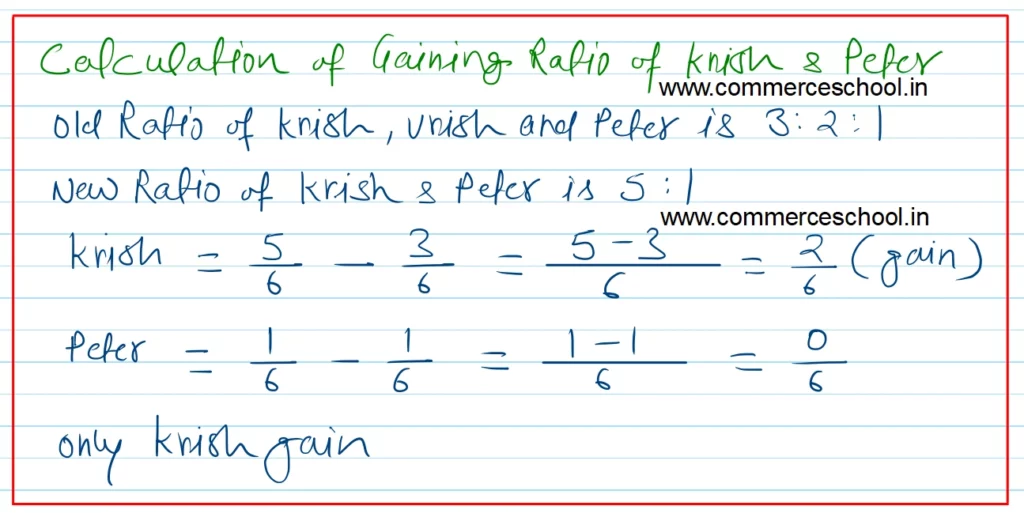

Q. 95. Krish, Vrish and Peter are partners sharing profits in the ratio of 3 : 2 : 1. Vrish retired from the firm. On that date the balance Sheet of the firm was as follows:

Balance Sheet as at 31st March, 2020

| Liabilities | ₹ | Assets | ₹ |

| Creditors | 15,000 | Bank | 7,600 |

| General Reserve | 12,000 | Furniture | 41,000 |

| Bills Payable | 12,000 | Stock | 9,000 |

| Outstanding Salary | 2,200 | Premises | 80,000 |

| Provision for Legal Damages | 6,000 | Debtors 6,000 Less; Provision for Doubtful Debts 400 | 5,600 |

| Capitals: Krish Vrish Peter | 46,000 30,000 20,000 | ||

| 1,43,200 | 1,43,200 |

Additional Information:

(i) Premises to be appreciated by 20%, Stock to be depreciated by 10% and Provision for doubtful debts was to be maintained @ 5% on Debtors. Further, provision for legal damages is to be increased by 1,200 and furniture to be brought up to ₹ 45,000.

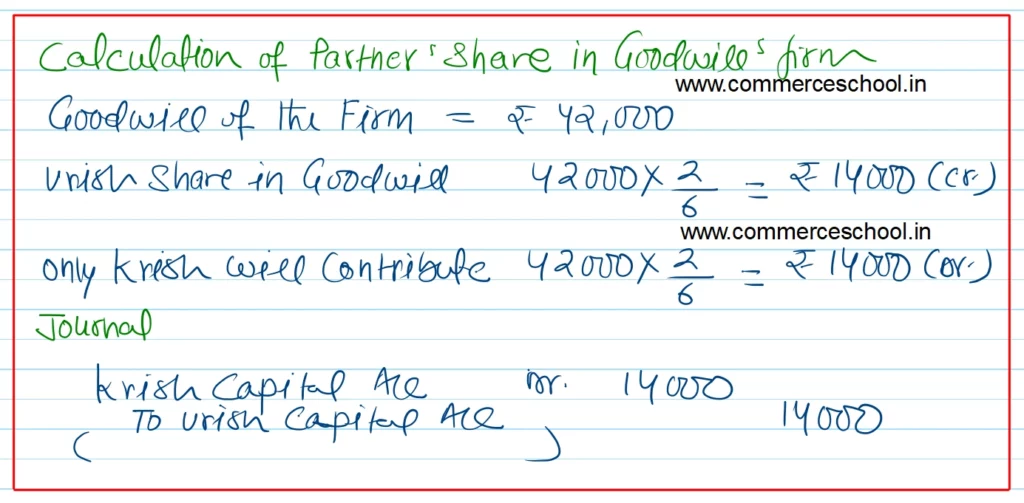

(ii) Goodwill of the firm is valued at ₹ 42,000.

(iii) ₹ 26,000 from Vrish’s Capital Account be treansferred to his loan account and balance to be paid through bank; if required, necessary loan may be obtained from bank.

(iv) New profit sharing ratio of Krish and Peter is decided to be 5 : 1.

Prepare Revaluation Account, Partners Capital Accounts and Balance Sheet.

[Ans. Gain on Revaluation ₹ 18,000; Net amount paid to Vrish ₹ 28,000; Balance of Capital A/cs : Krish ₹ 47,000 and Peter ₹ 25,000; Balance Sheet Total ₹ 1,54,800.]

Solution:-

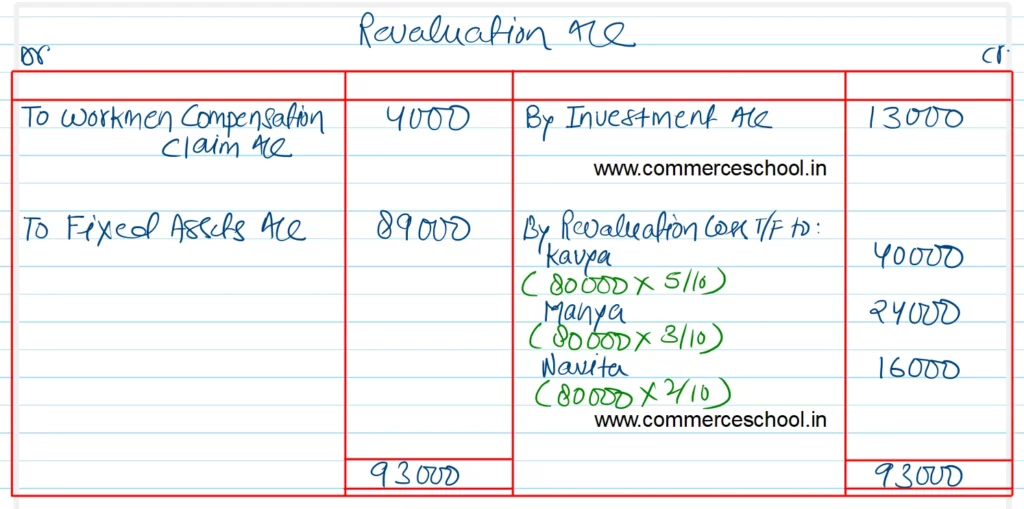

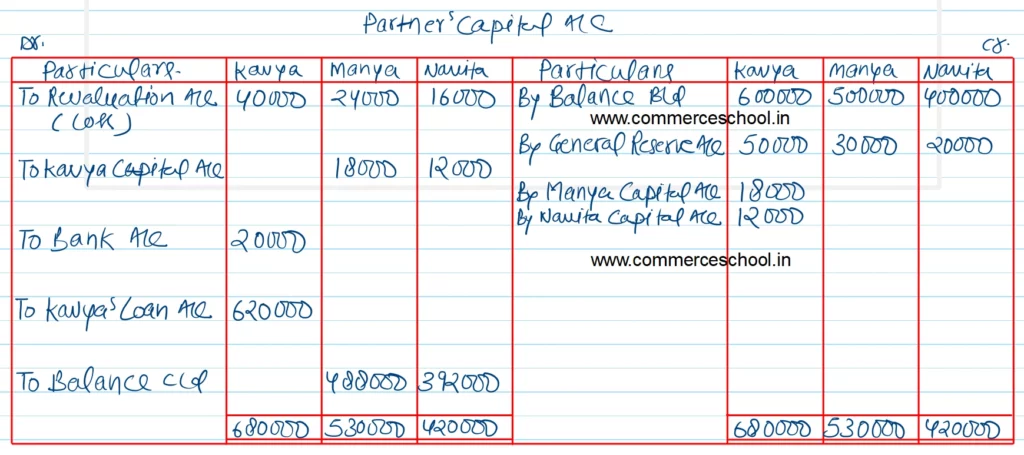

Q. 96. Kavya, Manya and Navita were partners sharing profits as 50%, 30% and 20% respectively. On 31-3-2016, their Balance sheet was as under:

| Liabilities | ₹ | Assets | ₹ |

| Creditors | 1,40,000 | Fixed Assets | 8,90,000 |

| General Reserve | 1,00,000 | Investments | 2,00,000 |

| Capitals: Kavya Manya Navita | 6,00,000 5,00,000 4,00,000 | Stock | 1,30,000 |

| Debtors 4,00,000 Less: Provision for Bad Debts 30,000 | 3,70,000 | ||

| Bank | 1,50,000 | ||

| 17,40,000 | 17,40,000 |

On the above date, Kavya retired and Manya and Navita agreed to continue the business on the following terms:

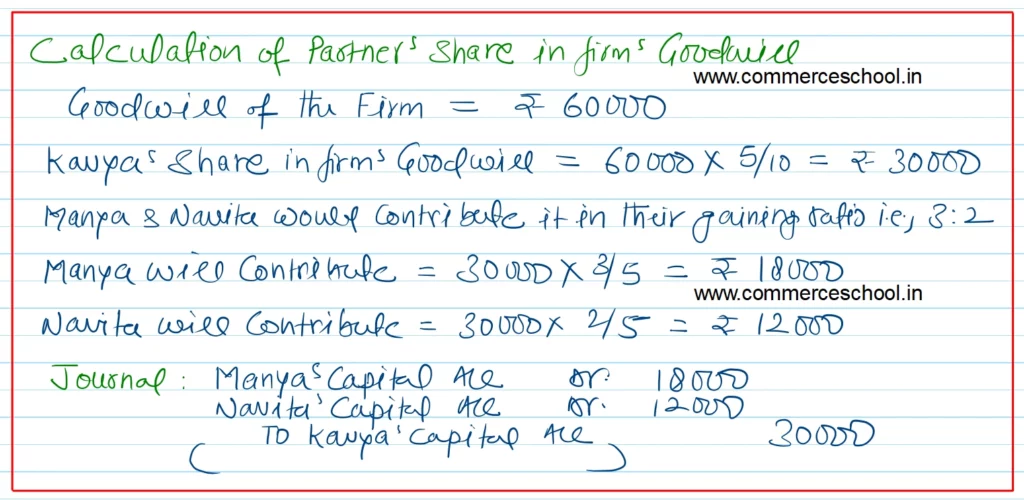

(a0 Firm’s goodwill was valued at ₹ 60,000 and it was decided to adjust Kavya’s share of goodwill in the capital accounts of continuing partners.

(b) There was a claim for workmen’s compensation to the extent of ₹ 4,000.

(c) Investments were revalued at ₹ 2,13,000.

(d) Fixed Assets were to be depreciated by 10%.

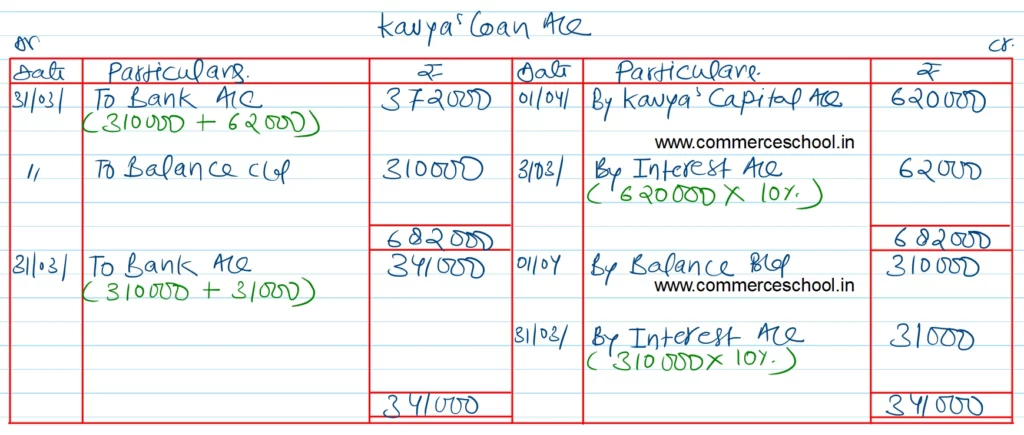

(e) Kavya was to be paid ₹ 20,000 through a bank draft and the balance was transferred to her loan account which will be paid in two equal annual instalments together with interest @ 10% p.a.

Prepare Revaluation A/c, Partner’s Capital Accounts and Kavya’s Loan Account till it is finally paid.

[Ans. Loss on Revaluation ₹ 80,000; Kavya’s Loan ₹ 6,20,000; Capital A/cs : Manya ₹ 4,88,000 and Navita ₹ 3,92,000.

Amount paid on 31st March 2017 : ₹ 3,10,000 + Interest ₹ 62,000.

Amount paid on 31st March 2018 : ₹ 3,10,000 + Interest ₹ 31,000]

Solution:-