[DK Goel] Q. 47, 48 Retirement of Partner Solutions Class 12 CBSE (2026-27)

Here are the solutions of Question number 47 and 48 of Retirement of Partner chapter 5 of DK Goel Class 12 CBSE (2026-27)

Q. 47. R, S and T were partners in a firm sharing profits in 2 : 2 : 1 ratio. On 1-4-2021 their Balance Sheet was as follows:

| Liabilities | ₹ | Assets | ₹ |

| Bank Loan | 12,800 | Cash | 51,300 |

| Sundry Creditors | 25,000 | Bills Receivable | 10,800 |

| Capitals: R S T | 80,000 50,000 40,000 | Debtors | 35,600 |

| Profit and Loss A/c | 9,000 | Stock | 44,600 |

| Furniture | 7,000 | ||

| Plant and Machinery | 19,500 | ||

| Building | 48,000 | ||

| 2,16,800 | 2,16,800 |

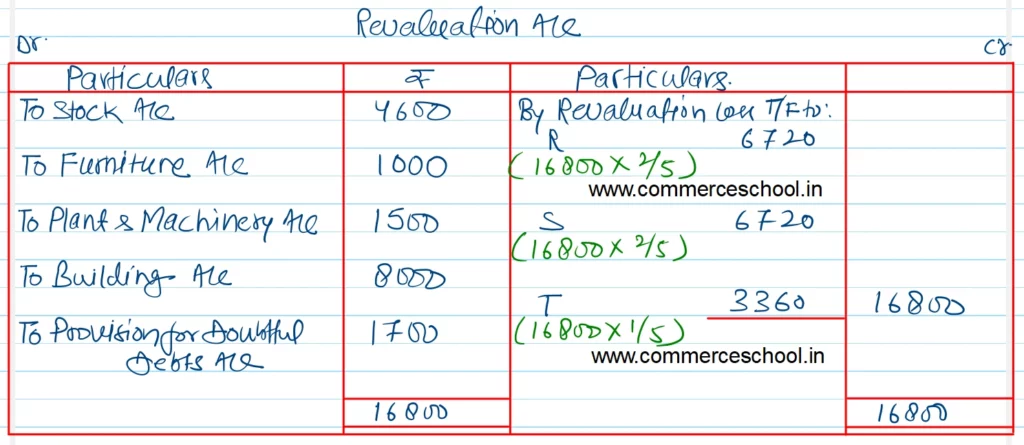

S retired from the firm on 1.4.2021 and his share was ascertined on the revaluation of assets as follows:

Stock ₹ 40,000; Furniture ₹ 6,000; Plant and Machinery ₹ 18,000; Building ₹ 40,000; ₹ 1,700 were to be provided for doubtful debts. The goodwill of the firm was valued at ₹ 12,000.

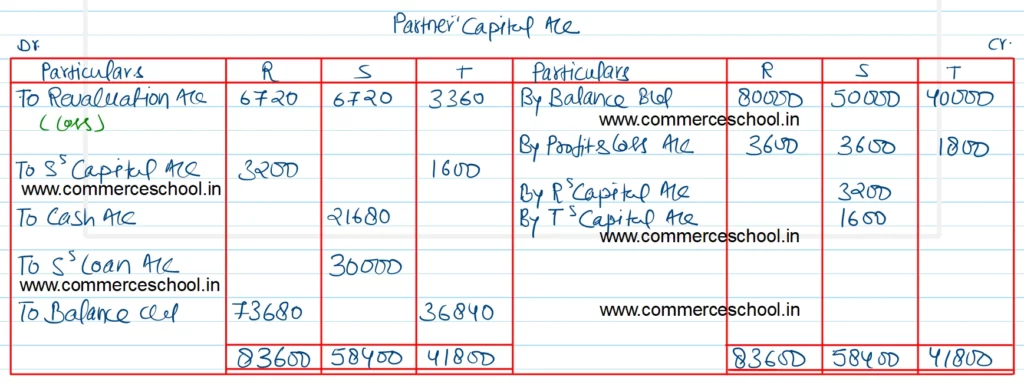

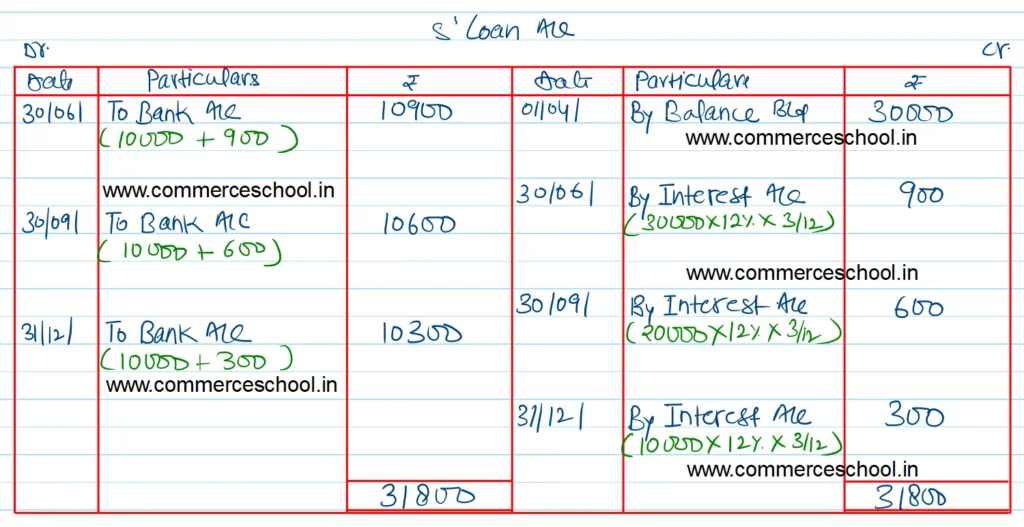

S was to be paid ₹ 21,680 in cash on retirement and the balance in three equal quarterly instalments (Starting from 30th June 2021) along with interest @ 12% p.a.

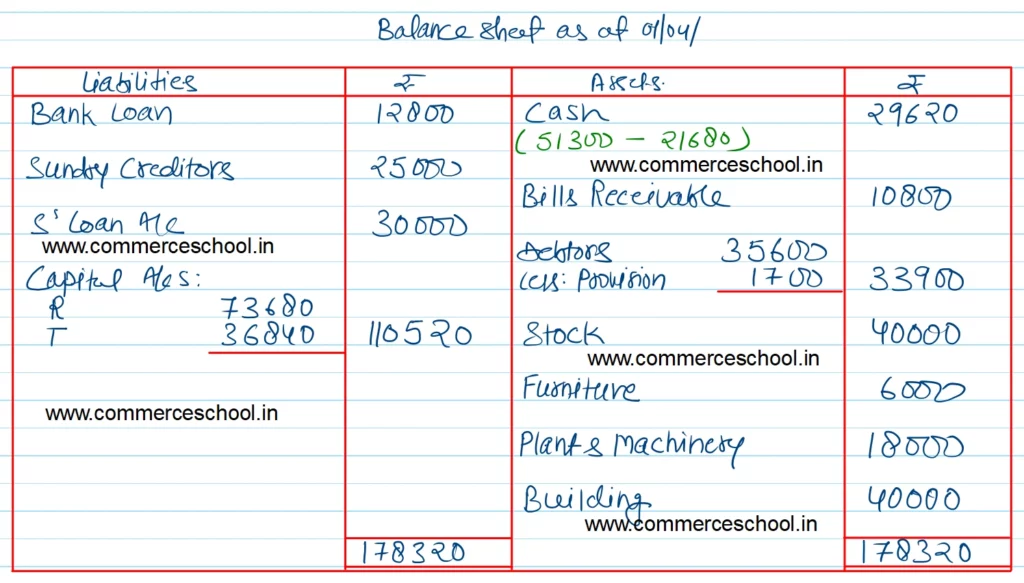

Prepare Revaluation Account, Partner’s Capital Accounts, S’s Loan Account and Balance Sheet on 1.4.2021.

[Ans. Loss on Revaluation ₹ 16,800; S’s Loan A/c ₹ 30,000; Capital A/cs : R ₹ 73,680 and T ₹ 36,840; Balance Sheet Total ₹ 1,78,320.]

Hint: Payment of S’s Loan A/c : ₹ 10,900 on 30th June 2021; ₹ 10,600 on 30th Sept. 2021 and ₹ 10,300 on 31st Dec. 2021.

Solution:-

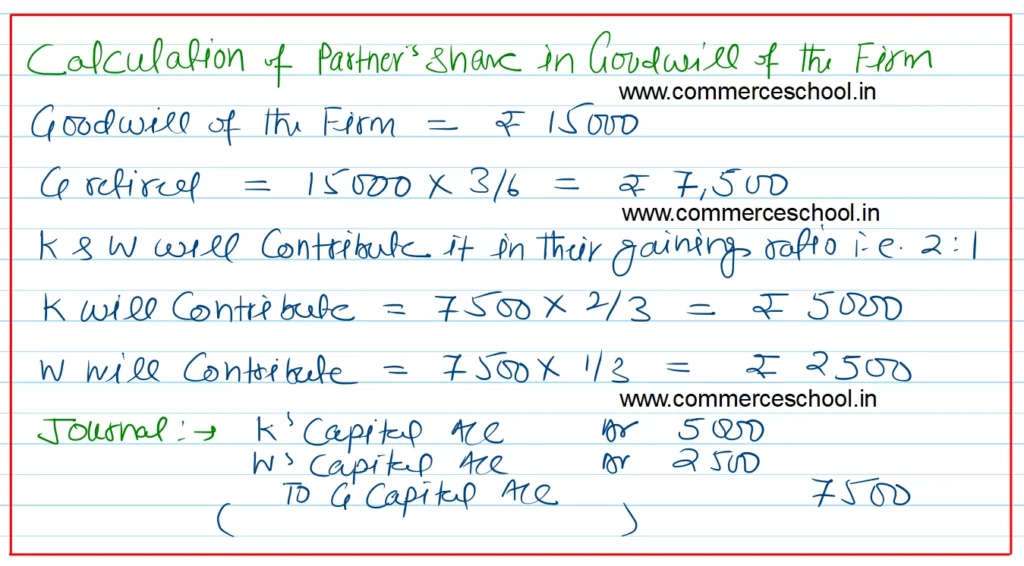

Following is the Balance Sheet of G, K & W as at 31st March, 2019 who share profits in the ratio of 3 : 2 : 1.

| Liabilities | ₹ | Assets | ₹ |

| Capital Accounts: G K W | 22,000 13,000 9,000 | Goodwill | 7,500 |

| Sundry Creditors | 10,000 | Stock | 12,500 |

| Bills Payable | 4,000 | Sundry Debtors | 12,000 |

| General Reserve | 12,000 | Land and Buildings | 15,000 |

| Plant and Machinery | 18,000 | ||

| Motor Vehicle | 5,000 | ||

| 70,000 | 70,000 |

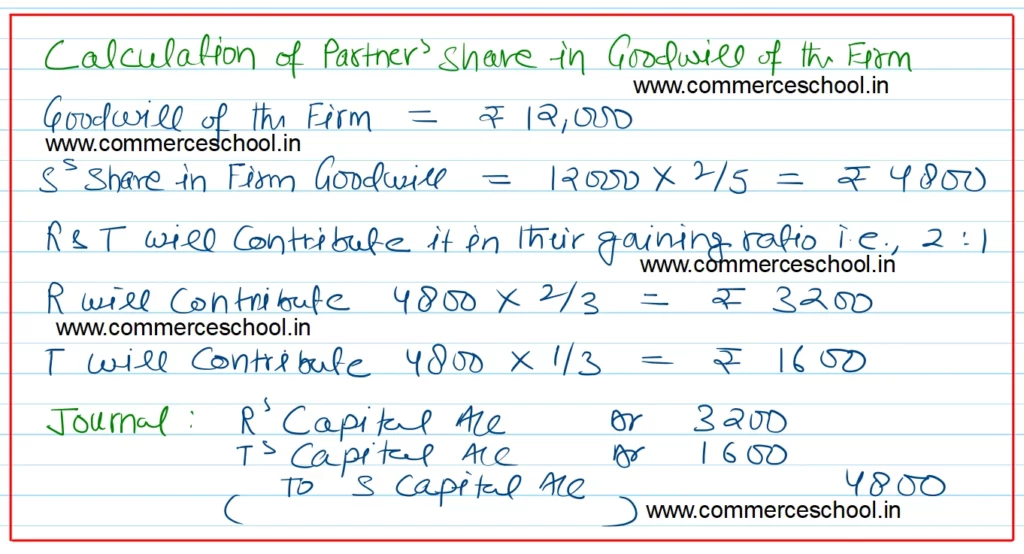

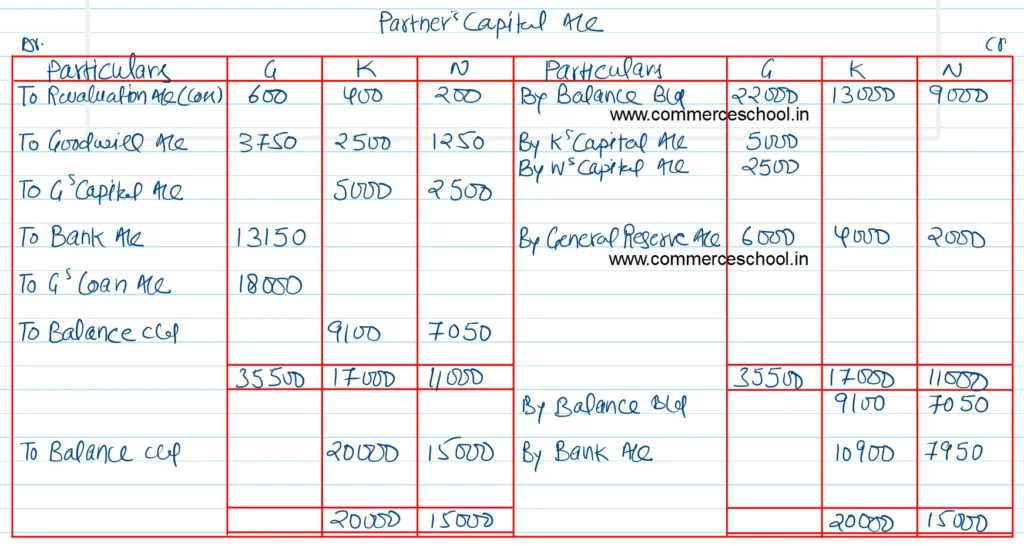

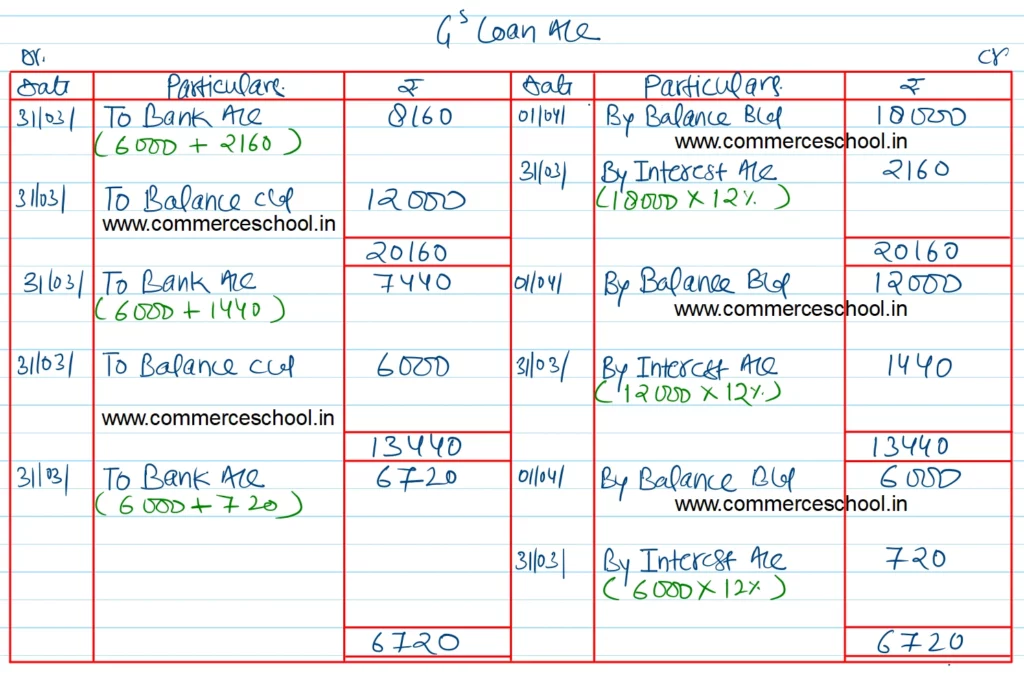

Q. 48. On 1st April, 2019, G retired and the following arrangements were agreed upon:

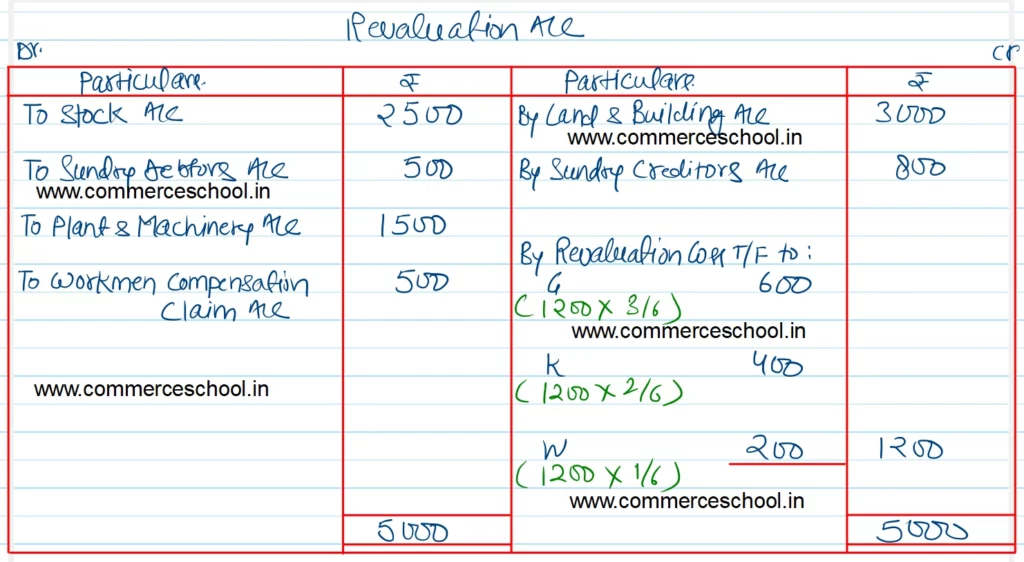

(1) Goodwill of the firm is to be valued at ₹ 15,000.

(2) The assets and liabilities are to be valued as under; Stock ₹ 10,000; Sundry Debtors ₹ 11,500; Land and Buildings ₹ 18,000; Plant and Machinery ₹ 16,500; and Sundry Creditors ₹ 9,200.

(3) Liability for Workmen’s Compensation amounting to ₹ 500 is to be brought into the books.

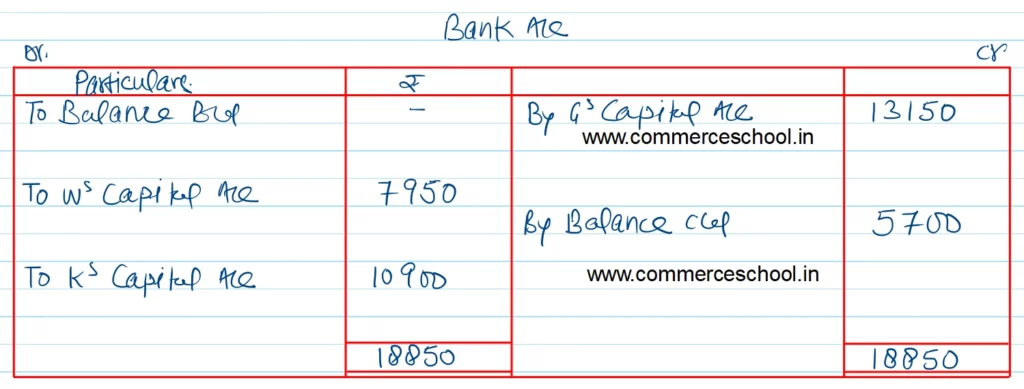

(4) The entire capital of the firm as newly constituted be fixed at ₹ 35,000 between K and W in the proportion of 4 : 3 and the actual cash to be paid off or to be brought in by continuing partners as the case may be.

(5) ₹ 13,150 were paid to G. The balance due to him was to be paid in three equal installments annually together with interest @ 12% per annum.

Give necessary ledger accounts, the Balance Sheet of the firm after G’s retirement and G’s Loan Account till it is finally paid off.

[Ans. Loss on Revaluation ₹ 1,200; Balance of G’s Loan A/c on 1st April, 2019 ₹ 18,000; Capital Accounts : K ₹ 20,000 and W ₹ 15,000; Cash brought in by K ₹ 10,900 and W ₹ 7,950; Cash Balance ₹ 5,700; B/S Total ₹ 66,700.]

Solution:-

Hint: 4 : 3 is not the new profit sharing ratio. Only the new partner will maintain their capital in the new firm in the ratio.