[ISC] Accounts Syllabus Class 11 (2026-27)

Comprehensive Accounts Syllabus of class 11 for ISC Board for 2026-27

There will be two papers in the subject:

Paper I – Theory 3 hours – 80 Marks

Paper II – Project Work – 20 Marks

| Syllabus PDF | Download Link |

| Accounts Class 11 Syllabus PDF (2026-27) | Click Here |

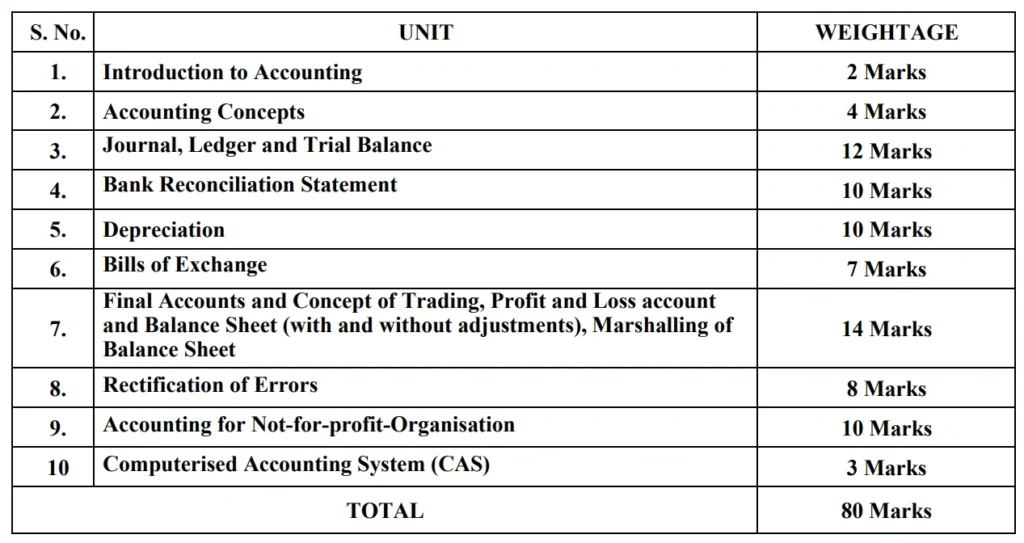

PAPER I (THEORY) : 80 Marks

1. Introduction to Accounting

Background of accounting and accountancy; types of accounts; basic terms used in accounting.

(i) A brief history of Accounting.

(ii) Basic Terms: Event, Transaction, Vouchers, Capital, Assets (intangible, tangible, fixed, current, liquid, wasting and fictitious), Liabilities (internal and external – current, long-term and contingent), Trade Debtors, Trade Creditors, Purchases, Sales, Goods traded in, Stock (raw material, work in progress and finished goods), Profit, Gain, Loss, Expense, Revenue, Income and Drawings.

(iii)Meaning and definition of Book-keeping, Accounting and Accountancy; difference between book-keeping, accounting and accountancy; accounting cycle.

(iv) Stakeholders of accounting information.

(v) Specialised fields of accounting: Meaning of financial accounting, cost accounting, and management accounting (brief introduction).

2. Accounting Concepts

GAAP (Generally Accepted Accounting Principles), Basis of Accounting; Accounting Standards; IFRS (International Financial Reporting Standards).

(i) GAAP: Going Concern, Accounting Entity, Money Measurement, Accounting Period, Complete Disclosure, Revenue Recognition, Verifiable Objective, Matching Principle, Historical Cost, Accrual

Concept, Dual Aspect Concept, Materiality, Consistency, Prudence and Timeliness, Industry Practice, Substance over legal form.

(ii) Basis of accounting : cash basis and accrual basis (meaning; difference).

(iii) Accounting Standards: Meaning; Utility/ Advantages.

(iv)IFRS (International Financial Reporting Standards) – Brief introduction

3. Journal, Ledger and Trial Balance

(i) Accounting equation: Meaning and usefulness, simple practical problems.

(ii) Journal: recording of entries in journal with narration.

(a) Classification of Accounts: traditional classification or modern approach.

(b) Double Entry System.

(c) Rules of journalizing : traditional classification or modern approach.

(d) Meaning of journal; Advantages of using a journal.

(e) Format of journal.

(f) Simple and compound journal entries.

(g) Opening Journal entry.

(h) Brief theoretical introduction to GST.

NOTE: Transactions with GST is excluded.

(iii) Ledger: Posting from journal to respective ledgers.

(a) Meaning of ledger.

(b) Format of a ledger.

(c) Mechanics of posting.

(d) Closing / Balancing of ledger accounts- expenses and revenues to be closed by transferring to Trading / P/L Account depending upon their direct/ indirect nature and balances of Assets, Liabilities and Capital to be carried down.

(e) Adjusting and closing journal entries.

(iv) Sub-division of journal : cash book [including simple cash book and triple column cash book (cash, bank and discount) with – contra entry pertaining to receipt of cheque not deposited on the same day; adjustments pertaining to a definite cash balance to be maintained / overdraft facility to be availed at the end of the month. Petty cash book, sales day book, purchases day book, sales return day book, purchases return day book and Journal proper.

(a) Cash book [including simple cash book and triple column cash book (cash, bank and discount) with contra entry pertaining to receipt of cheque not deposited on the same day; adjustments pertaining to a definite cash balance to be maintained / overdraft facility to be availed at the end of the period].

(b) Petty cash book (including analytical and imprest system).

(c) Sales day book, purchases day book- Simple (Date, Particulars, I. No, L.F, Details, Amount); Columnar (Date, Particulars, I. No, L.F, Details, Net Invoice, Goods, Carriage).

(d) Sales return day book, purchases return day book- Simple (Date, Particulars, Credit/ Debit Note No., L.F, Details, Amount).

(e) Journal proper.

(f) Mechanics of posting from special subsidiary books.

NOTE: Transactions with GST is excluded in Cash Book and Returns Books.

(v) Trial Balance.

(a) Meaning, objectives, advantages and limitations of a Trial Balance.

(b) Preparation of the Trial Balance by the balance method from the given ledger account balances.

4. Bank Reconciliation Statement

Bank Reconciliation statement.

(i) Meaning and need for bank reconciliation statement.

(ii) Preparation of a bank reconciliation statement from the given cash book balance / overdraft or pass book balance / overdraft.

(iii)Preparation of a bank reconciliation statement from the extract of the cash book as well as the pass book.

(iv) Preparation of an amended cash book and a b

5. Depreciation

Depreciation, Methods of charging depreciation, Method of recording depreciation.

(i) Depreciation: meaning, need, causes, objectives and characteristics.

(ii) Methods of charging depreciation: Straight Line and Written Down Value method; advantages, limitations of both the methods and differences between the two.

(iii)Methods of recording depreciation: charging to asset account, creating provision for depreciation / accumulated depreciation.

(iv) Problems relating to purchase and sale of assets (with or without asset disposal account) incorporating the application of depreciation under the two stated methods.

NOTE: Questions on change of method from SLM to WDV and vice-versa are not required.

6. Bills of Exchange

(i) Introduction to Negotiable Instruments: explanation of basic terms. Meaning of negotiable instruments; Bills of exchange, promissory note (including specimen and distinction), cheque, advantages and disadvantages of Bills of Exchange, explanation of basic terms – drawer, drawee, payee, endorser, endorsee, bill on demand / bill on sight, bill after date, bill after sight, tenure of the bill, days of grace, due date, endorsement and discounting of bills, bill sent for collection, dishonour of a bill, holder of a bill, noting charges, notary public, renewal of a bill, retirement of a bill and insolvency of the drawee/acceptor.

(ii) Practical problems on the above in the books of drawer, drawee and endorsee- Journal entries and Ledger accounts.

NOTE: (i) Accommodation Bill is not required. (ii) Recording in the books of the bank not required.

7. Final Accounts and Concept of Trading, Profit and Loss account and Balance Sheet (with and without adjustments), Marshalling of Balance Sheet

(i) Capital and Revenue Expenditure/Income.

(a) Meaning and difference between capital expenditure and revenue expenditure with examples.

(b) Meaning and difference between capital receipts and revenue receipts with examples.

(c) Meaning and difference between capital profit/income and revenue profit/ income with examples.

(d) Meaning and difference between capital loss and revenue loss with examples.

(e) Meaning of deferred revenue expenditure with examples.

(ii) Provisions and Reserves.

Meaning, importance; difference between provisions and reserves; types of reserves – revenue reserve, capital reserve, general reserve, specific reserve and secret reserve.

(iii)Trading, Profit and Loss Account and Balance Sheet of a sole trader, (Horizontal Format) without adjustments. Meaning, objectives, importance and preparation of Trading, Profit and Loss Account and Balance Sheet of a sole trader.

(iv) Preparation of Trading Account, Profit and Loss Account and Balance Sheet with necessary adjustments. Adjustments relating to closing stock, outstanding expenses, prepaid expenses, accrued income, income received in advance, depreciation, bad debts, provision for doubtful debts, provision for discount on debtors, manager’s commission (on the net profit before and after charging such commission), goods distributed as free samples, goods taken by the owner for personal use and abnormal loss; Treatment of Adjusted Purchases and calculation of cost of goods sold; Calculation of operating profit.

(v) Marshalling of a Balance Sheet: Order of permanence and order of liquidity.

(vi) Adjusting, closing and transfer entries.

NOTE:

(1) Practical problems on preparation of provision for doubtful debts account are not required.

(2) Since creating provision for doubtful debts accounts involves being prudent, in the absence of any information of the amount of the new provision, it will be assumed that the remaining amount / balance of debtors are good/ Apply same percentage of provision on the closing debtors as the percentage applied at the beginning of the year.

8. Rectification of Errors

Errors and types of errors: Rectification of errors after the preparation of Trial Balance and rectification of errors after the preparation of Final Accounts.

(i) Types of Errors: Errors of omission, errors of commission, errors of principle, compensating errors.

(ii) Rectification of errors after the preparation of trial balance and through suspense account if required.

(iii)Rectification of errors after the preparation of Final Accounts through P/L Adjustment A/c if required.

(iv) Preparation of Suspense Account.

NOTE: Redrafting of Balance Sheet not required.

- Accounting for Not-for-profit-Organisation

(i) Introduction to Not-for-profit-Organisation: Meaning, objectives, necessity and treatment of specific

items.

(ii) Different accounting books maintained and differences among them.

(a) Receipts and Payments Accounts: meaning, features, differences between Receipts and Payments

Account and Cash Book.

(b) Income and Expenditure Accounts: meaning, features, difference between Income and Expenditure

account and Profit and Loss account.

(c) Preparation of Balance Sheet.

(iii) Preparation of Income and Expenditure Account and Closing Balance Sheet. Preparation of Income and Expenditure Account and Balance Sheet when Receipts and Payments Account and other information is given.

(a)Entrance, admission fees, life membership fees, legacies, special grants and special donations are to be capitalised.

(b)General donations, general grants and all receipts of a recurring nature such as membership fees/ subscriptions are to be taken as revenue receipts.

NOTE 1: Preparation of accounts of incidental activities such as restaurant accounts are not required.

NOTE 2: Preparation of a Receipt and Payments Account only or an Income and Expenditure Account with a Balance Sheet from incomplete records need not be covered (in horizontal format).

10. Computerised Accounting System (CAS)

Introduction, Components of CAS, Salient features of CAS, Advantages and Limitations of CAS; and Accounting Information System.

PAPER II (PROJECT WORK) : 20 MARKS

Candidates will be expected to have completed two projects from any topic covered in Theory.

Mark allocation for each Project [10 marks]:

| Overall format | 1 Marks |

| Content | 4 Marks |

| Findings | 2 Marks |

| Viva-voce based on the Project only | 3 Marks |

A list of suggested Projects is given below:

1. Preparation of Journal / sub-division of journal, Ledger, Trial balance and Financial Statements of a trading organization on the basis of a case study.

- Develop a case study of a sole trader starting business with a certain amount of capital. The trader could have got the amount from his past savings or by borrowing from a bank by mortgaginghis personal assets or by winning a lottery or any other source.

- From this case study developed (which should have at least 15 transactions), pass the journal entries, post them into the ledger, prepare a Trial Balance and the Trading and Profit and Loss Account and Balance Sheet.

- The various expenses for comparison purposes, could be depicted in the form of bar diagrams and pie charts.

- Write in detail, his transactions during the year- his purchases – cash and credit, sales-cash and credit, expenses, purchase of fixed assets and depreciation charged on them, any outstanding expenses, prepaid expenses, accrued income, drawing bills of exchange, accepting bills payable, etc.

2. Preparation of the accounts of a Not-for-Profit-Organisation on the basis of a case study.

- Develop a case study of an NPO by beginning with the primary motive of establishing it, that is, why have you decided to open a club or a library or a hospital, etc.

- Write in detail about the sources of capital fund, subscriptions, donations (ordinary and special), other receipts and payments of your NPO as well as outstanding expenses, prepaid expenses, subscription due but not received, subscription received in advance, purchase of fixed assets and depreciation charged on

them, legacy received, etc. - From this case study developed (which should have at least 15 transactions), pass the journal entries, post them into the ledger, prepare a trial balance and thereafter prepare the NPO’s Cash Book, Receipts and Payment Account, its Income and Expenditure Account and its Balance Sheet.

- The various expenses, for comparison purposes, could be depicted in the form of bar diagrams and pie charts.

3. Prepare a Bank Reconciliation Statement and Amended Cash Book from the information given in your Cash Book and Bank Statement (Pass Book) with at least fifteen transactions.

4. Draw a specimen of bill of exchange – show how they differ from Promissory note and develop a question based on two bills of exchange, one of them being honoured and the other dishonoured and its renewal along with noting charges and interest.

5. Take any five accounting concepts and give any two practical examples of each to bring out clearly the understanding of the concept.

6. Develop a case study by creating an imaginary Trial Balance and develop any five-six adjustments and then prepare the Trading, Profit & loss account and Balance Sheet out of it, along with journal entries for those adjustments.

7. Prepare a case study containing purchase of more than one asset where:

- sale of an asset takes place resulting in either profit or loss/ no profit or loss.

- the purchase of an asset takes place during the year.

- a provision for depreciation/ accumulated depreciation account is to be maintained.

- depreciation is charged either through SLM or WDV method.

Candidates are required to prepare journal entries and related accounts.

8. Take up an internship programme for a week under any commercial /non-commercial organization and prepare a report that includes the following details:

- Organization profile (name, sector, type of organization, etc.)

- Internship activities (day-wise break up)

- Tasks done (vouchers prepared, BRS, etc.)

- Learning outcomes from internship.

- Documentation of the internship activity. (photographs, certificate, etc.)