[CBSE] Accountancy Syllabus class 12 (2026-27)

Looking for the syllabus of Accountancy class 12 of CBSE Board for the 2026-27 Session.

Here is the detailed syllabus with download link

Syllabus of Accounts class 12 CBSE Board 2026-27

| Accounts Syllabus Class 12 (2026-27) | Download link |

Read Here:- [CBSE] TS Grewal Accounts Solutions Class 12 (2026-27)

Read Here:- [CBSE] TS Grewal Accounts Solutions Class 12 (2025-26)

Theory Paper 80 Marks (3 Hour, 15 Mints Reading Time)

Project Work:- 20 Marks

Accountancy (Code No. 055)

| Units | Particulars | Periods | Marks |

| Part – A | Accounting for Partnership Firms and Companies | ||

| Unit 1. Accounting for Partnership Firms | 105 | 36 | |

| Unit 2. Accounting for Companies | 45 | 24 | |

| 150 | 60 | ||

| Part – B | Financial Statement Analysis | ||

| Unit 3. Analysis of Financial Statements | 30 | 12 | |

| Unit 4. Cash Flow Statement | 20 | 8 | |

| 50 | 20 | ||

| or | |||

| Part – B | Unit – 4. Computerized Accounting | 50 | 20 |

| Part – C | Project Work Project work will include: Project File (12 Marks) Viva Voce (8 Marks) | 20 | |

| Total | 100 |

Read Here:- Economics Syllabus of Class 12 CBSE Board 2023-24

Read Here:- Business Studies Syllabus of class 12 CBSE Board 2023-24

Part A

Unit 1: Accounting for Partnership Firms

Units/Topics

Partnership: features, Partnership Deed.

Provisions of the Indian Partnership Act 1932 in the absence of a partnership deed.

Fixed v/s fluctuating capital accounts. Preparation of Profit and Loss Appropriation account- a division of profit among partners, a guarantee of profits.

Past adjustments (relating to interest on capital, interest on drawing, salary, and profit-sharing ratio).

Goodwill: nature, factors affecting and methods of valuation – average profit, super profit, and capitalization

Note:

Interest on a partner’s loan is to be treated as a charge against profits.

Goodwill to be adjusted through partners’ capital/ current account.

Note:

Raising and writing off goodwill is excluded.

Accounting for Partnership firms – Reconstitution and Dissolution.

Change in the Profit Sharing Ratio among the existing partners – sacrificing ratio, gaining ratio, accounting for revaluation of assets and reassessment of liabilities, and treatment of reserves and accumulated profits.

Preparation of revaluation account and balance sheet.

Admission of a partner – effect of admission of a partner on change in the profit-sharing ratio, treatment of goodwill, treatment for revaluation of assets and re-assessment of liabilities, treatment of reserves and accumulated profits, adjustment of capital accounts, and preparation of balance sheet.

Retirement and death of a partner: effect of retirement/death of a partner on change in profit sharing ratio, treatment of goodwill, treatment for revaluation of assets and reassessment of liabilities, adjustment of accumulated profits and reserves, adjustment of capital accounts, and preparation of balance sheet.

Preparation of loan account of the retiring partner.

Calculation of deceased partner’s share of profit till the date of death. Preparation of the deceased partner’s capital account and his executor’s account.

Dissolution of a partnership firm: meaning of dissolution of partnership and partnership firm, types of dissolution of a firm. Settlement of accounts – preparation of realization

account, and other related accounts: capital accounts of partners and cash/bank a/c (excluding piecemeal distribution, sale to a company, and insolvency of partner(s)).

Note:

(i) If the realized value of an asset is not given, it is to be presumed that it has not realized any amount.

(ii) If a partner has borne and/ or paid the realization expenses, it should be stated.

Unit-2 Accounting for Companies

Units/Topics

Accounting for Share Capital

Share and share capital: nature and types.

Accounting for share capital: issue and allotment of equity and preferences shares. Public subscription of shares – over subscription and under subscription of shares; the issue at par and at a premium, call in advance and arrears (excluding interest), issue of shares for consideration other than cash.

Concept of Private Placement and Employee Stock Option Plan (ESOP).

Accounting treatment of forfeiture and reissue of shares.

Disclosure of share capital in the Balance Sheet of a company.

Accounting for Debentures

Debentures: Issue debentures at par, at a premium, and at a discount. Issue of debentures for consideration other than cash; Issue of debentures with terms of redemption; debentures as collateral security concept, interest on debentures. Writing off discount/loss on the issue of debentures.

Note: Discount or loss on issue of debentures to be written off in the year debentures are allotted from Security Premium Reserve/ Capital Reserve/ Statement of Profit and Loss as Financial Cost (AS 16) in that order.

Part B: Financial Statement Analysis

Units/Topics

Financial statements of a Company:

Statement of Profit and Loss and Balance Sheet in the prescribed form with major headings and subheadings (as per Schedule III to the Companies Act, 2013)

Note: Exceptional items, extraordinary items, and profit (loss) from discontinued operations are excluded.

Financial Statement Analysis: Objectives, importance, and limitations.

Tools for Financial Statement Analysis:

Comparative statements, common-size statements, cash flow analysis, ratio analysis.

Accounting Ratios: Meaning, Objectives, classification, and computation.

Liquidity Ratios: Current ratio and Quick ratio.

Solvency Ratios: Debt to Equity Ratio, Total Asset to Debt Ratio, Proprietary Ratio, and Interest Coverage Ratio.

Activity Ratios: Inventory Turnover Ratio, Trade Receivables Turnover Ratio, Trade Payables Turnover Ratio, and Working Capital Turnover Ratio.

Profitability Ratios: Gross Profit Ratio, Operating Ratio, Operating Profit Ratio, Net Profit Ratio, and Return on Investment.

Note: Net Profit Ratio is to be calculated on the basis of profit before and after tax.

Unit 4: Cash Flow Statement

Units/Topics

Meaning, objectives, and preparation (as per AS 3 (Revised) (Indirect Method only)

Note:

(i) Adjustments relating to depreciation and amortization, profit or loss on sale of assets including investments, dividend (both final and interim), and tax.

(ii) Bank overdraft and cash credit to be treated as short-term borrowings.

(iii) Current Investments to be taken as Marketable securities unless otherwise specified.

Note: Previous years’ Proposed Dividend to be given effect, as prescribed in AS-4, Events occurring after the Balance Sheet date. Current years’ Proposed Dividend will be accounted for in the next year after it is declared by the shareholders.

OR

Part B: Computerised Accounting

Unit 4: Computerised Accounting

Overview of Computerised Accounting System

Introduction: Application in Accounting.

Features of Computerised Accounting System.

Structure of CAS.

Software Packages: Generic; Specific; Tailored. Accounting Application of Electronic Spreadsheet.

Concept of the electronic spreadsheet.

Features offered by electronic spreadsheet.

Application in generating accounting information – bank reconciliation statement; asset accounting; loan repayment of loan schedule, ratio analysis

Data representation- graphs, charts, and diagrams. Using Computerized Accounting System.

Steps in the installation of CAS, codification, Hierarchy of account heads, and creation of accounts.

Data: Entry, validation, and verification.

Adjusting entries, preparation of balance sheet, profit, and loss account with closing entries and opening entries.

Need and security features of the system. Database Management System (DBMS)

Concept and Features of DBMS.

DBMS in Business Application.

Generating Accounting Information – Payroll.

Part C: Practical Work

Please refer to the guidelines published by CBSE.

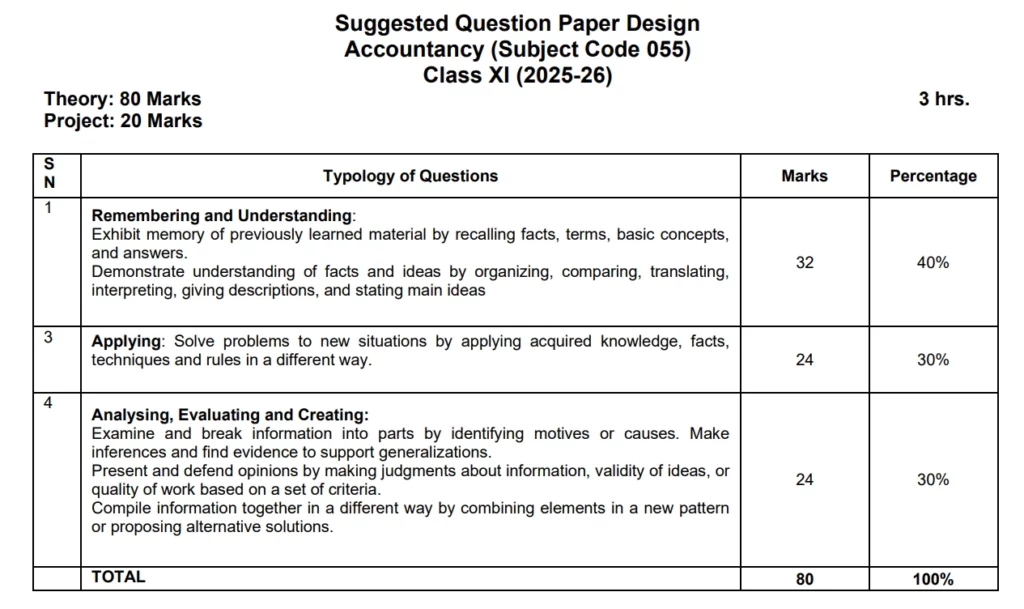

Paper Pattern for 2025-26 Session:-