[CBSE] Q. 102,103,104,105 Solution of Accounting Ratios TS Grewal Class 12 (2026-27)

Solution of Question 102, 103, 104, 105 Accounting Ratios of TS Grewal Book 2026-27 session CBSE Board

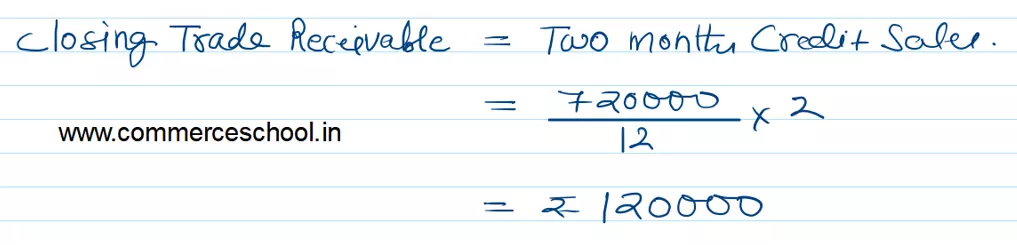

Q. 102. A firm normally has trade Receivables equal to two months’ Credit Sales.

During the coming year it expects Credit Sales of ₹ 7,20,000 spread evenly over the year (12 months). What is the estimated amount of Trade Receivbles at the end of the year?

[Ans.: Estimated Trade Receivables = ₹ 1,20,000.]

Solution:-

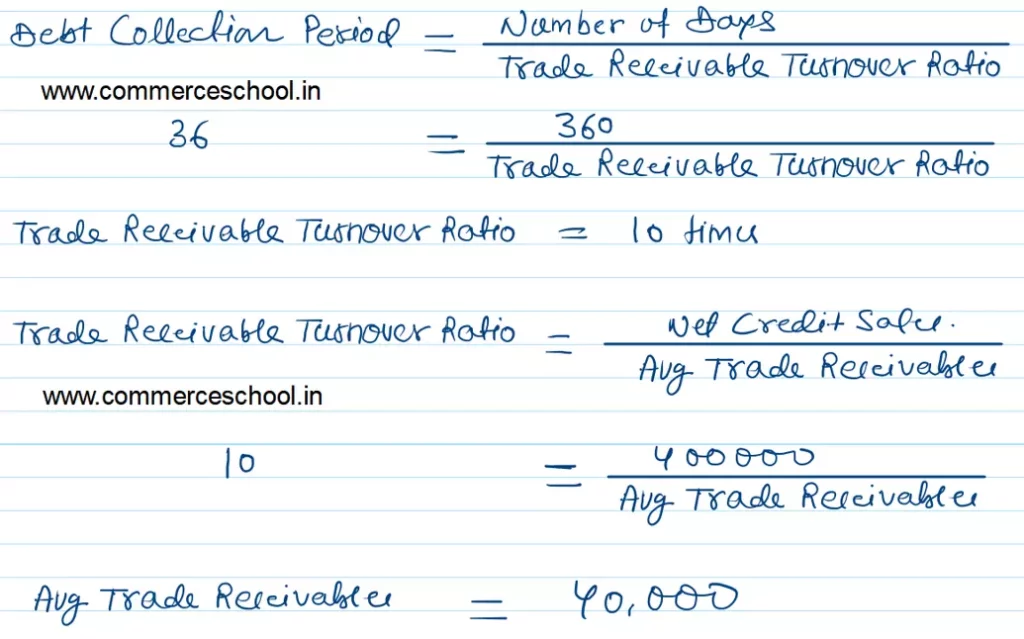

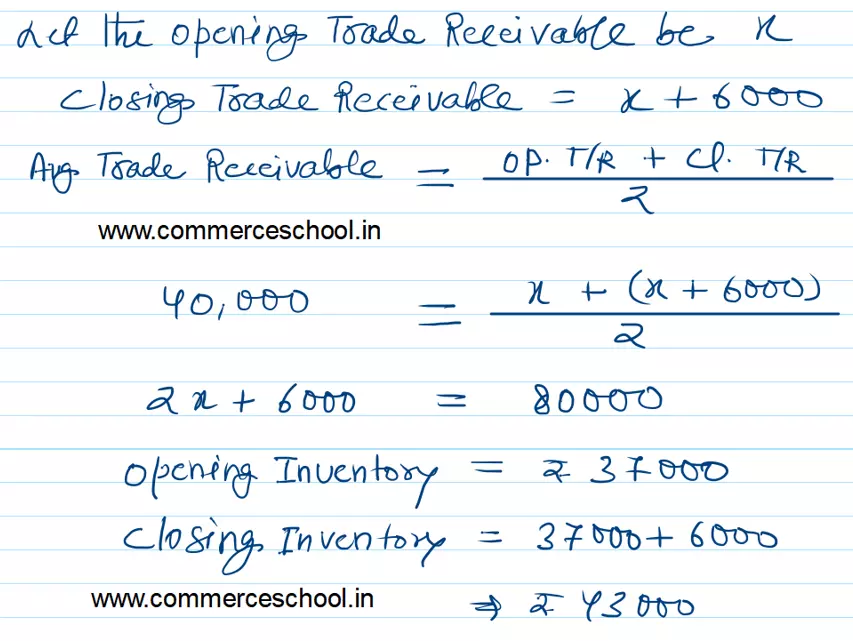

Q. 103. Mercury Ltd. made Credit Sales of ₹ 4,00,000 during the financial period.

If the collection period is 36 days and year is assumed to be 360 days, calculate:

(i) Trade Receivables Turnover Ratio;

(ii) Average Trade Receivables;

(iii) Trade Receivables at the end when Trade Receivables at the end are more than that in the beginning by ₹ 6,000.

[Ans.: (i) Trade Receivables Turnover Ratio = 10 Times: (ii) Average Trade Receivables = ₹ 40,000; (iii) Trade Receivables in the beginning = ₹ 37,000; Trade Receivbles at the end = ₹ 43,000.]

Solution:-

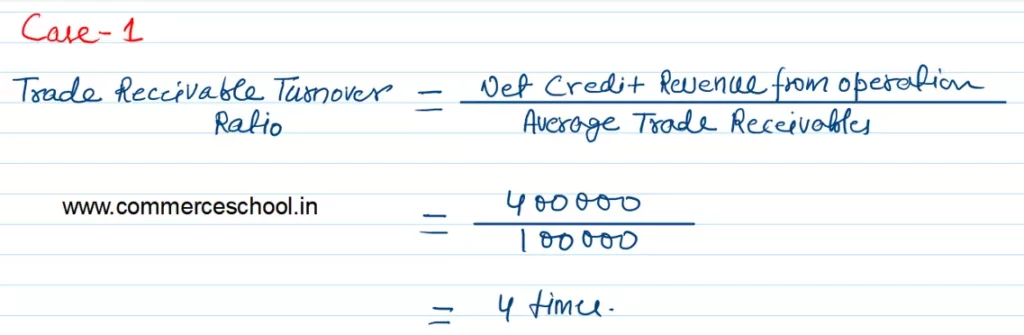

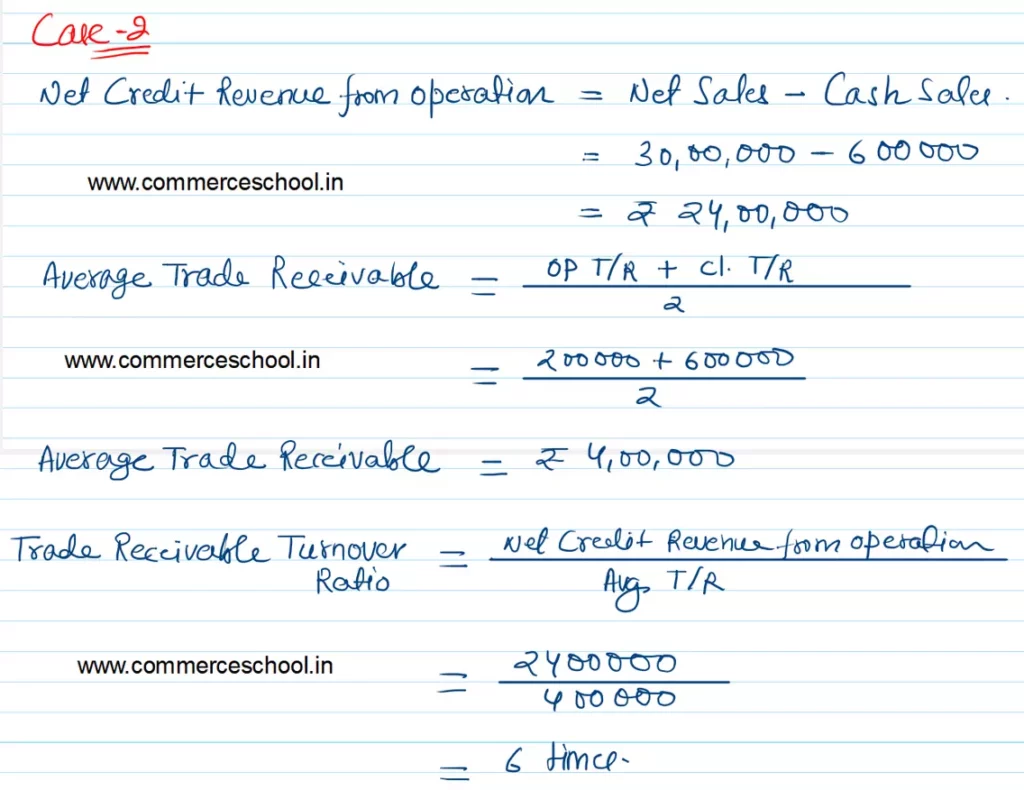

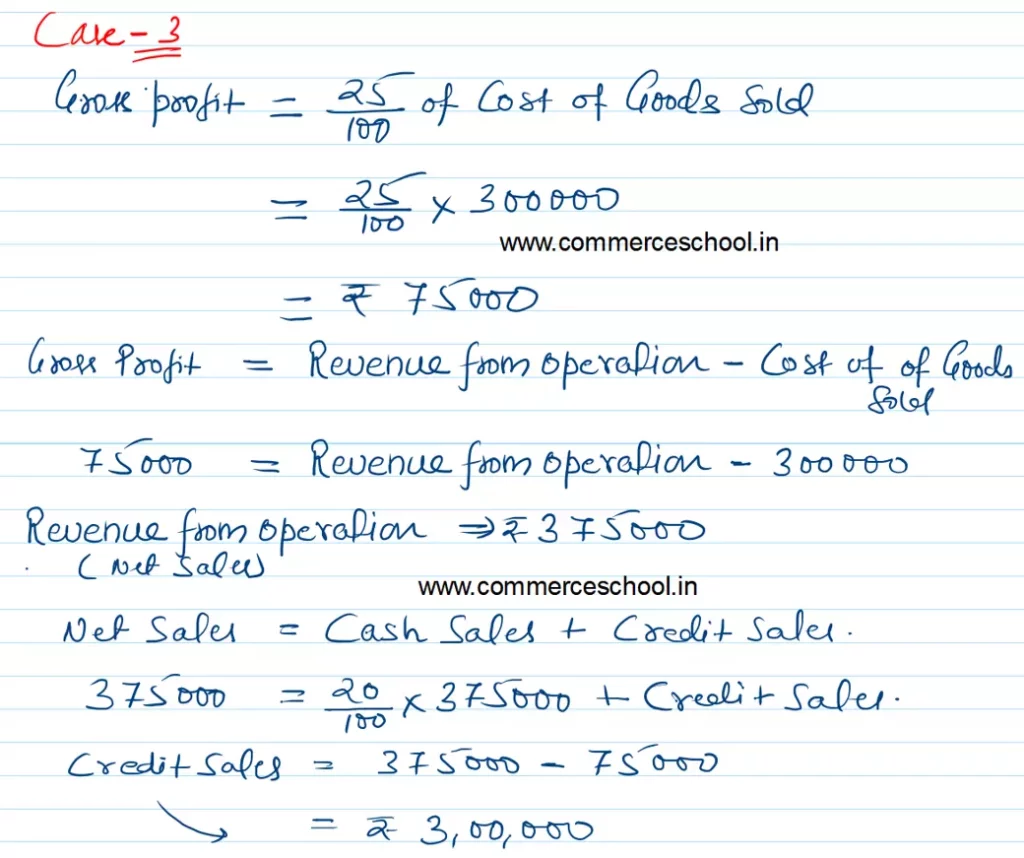

Q. 104. Trade Receivables Turnover Ratio in each of the following alternative cases:

Case 1: Net Credit Sales ₹ 4,00,000; Average Trade Receivables ₹ 1,00,000.

Case 2 : Revenue from Operations (Net Sales) ₹ 30,00,000; Cash Revenue from Operations, i.e., Cash Sales ₹ 6,00,000; Opening Trade Receivables ₹ 2,00,000; Closing Trade Receivables ₹ 6,00,000.

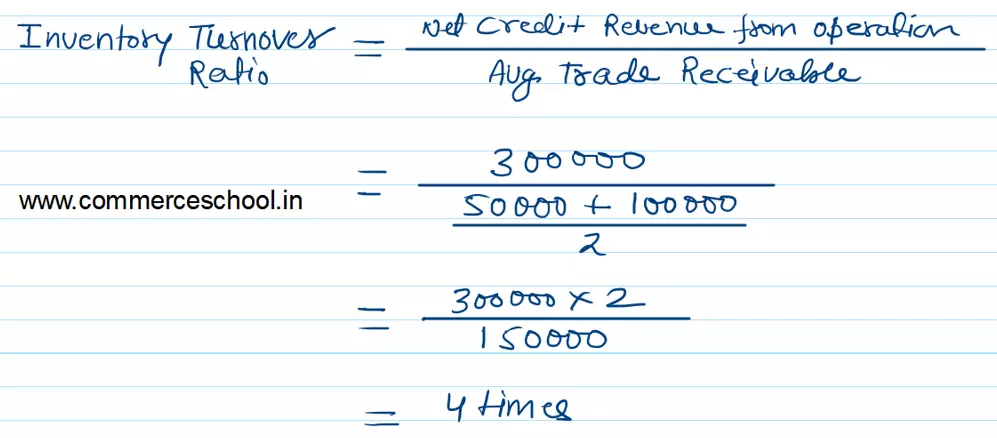

Case 3: Cost of Revenue from Operations or Cost of Goods Sold ₹ 3,00,000; Gross Profit on Cost 25%; Cash Sales 20% of Total Sales; Opening Trade Receivables ₹ 50,000; Closing Trade Receivables ₹ 1,00,000.

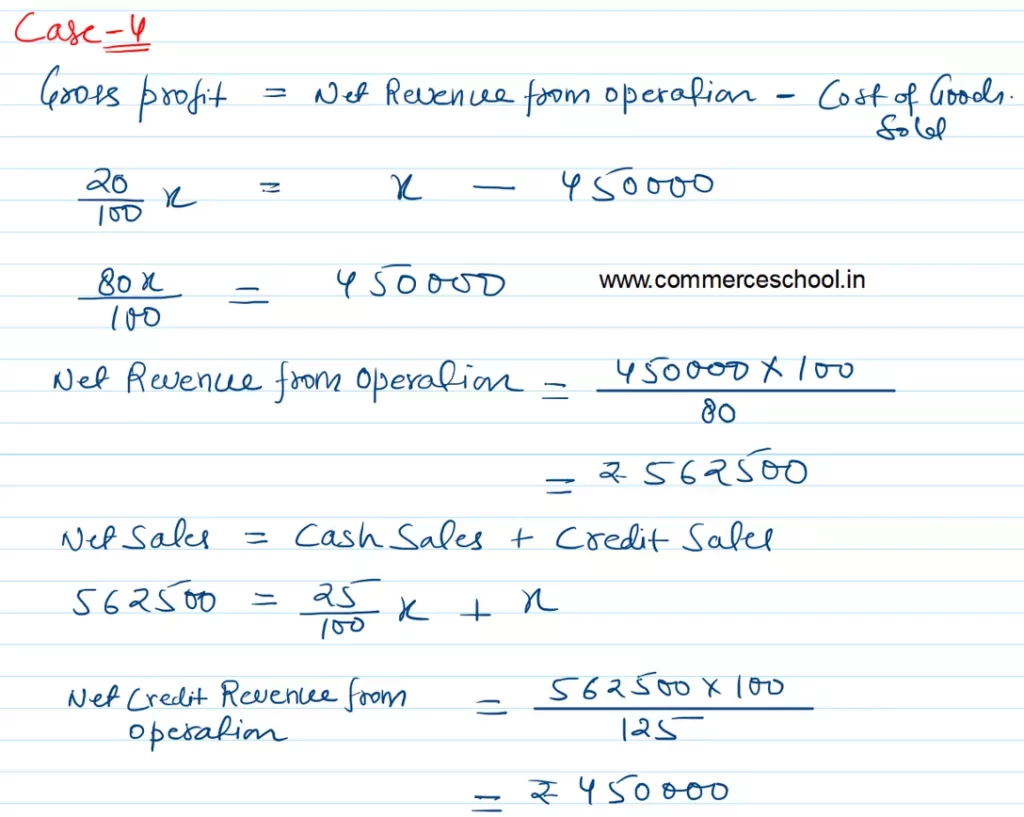

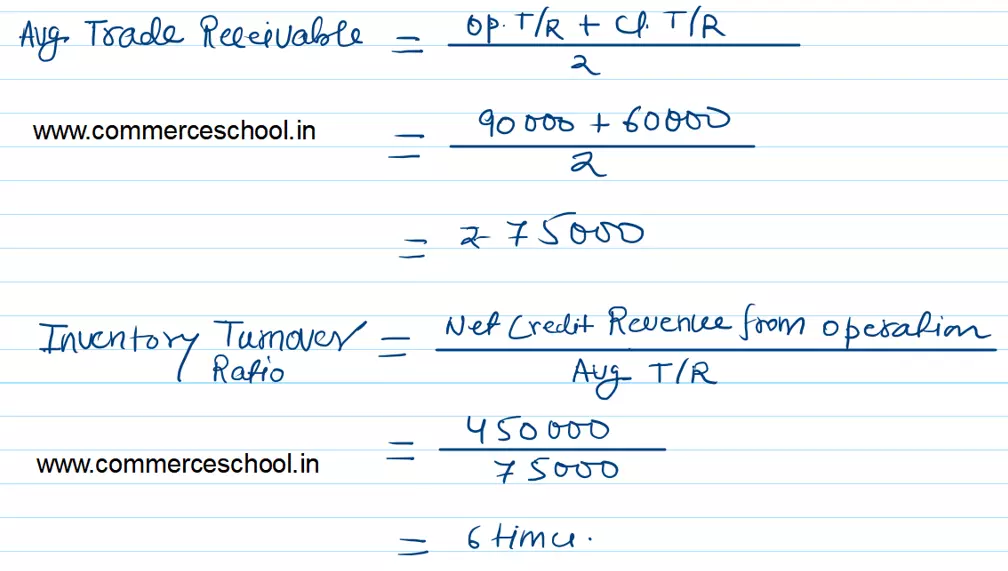

Case 4: Cost of Revenue from Operations or Cost of Goods Sold ₹ 4,50,000; Gross Profit on Sales 20%; Cash Sales 25% of Net Credit Sales, Opening Trade Receivables ₹ 90,000; Closing Trade Receivables ₹ 60,000.

[Ans.: Case 1: Trade Receivables Turnover Ratio = 4 Times; Case 2: Trade Receivables Turnover Ratio = 6 Times; Case 3: Trade Receivables Turnover Ratio = 4 Times; Case 4: Trade Receivables Turnover Ratio = 6 Times.]

Solution:-

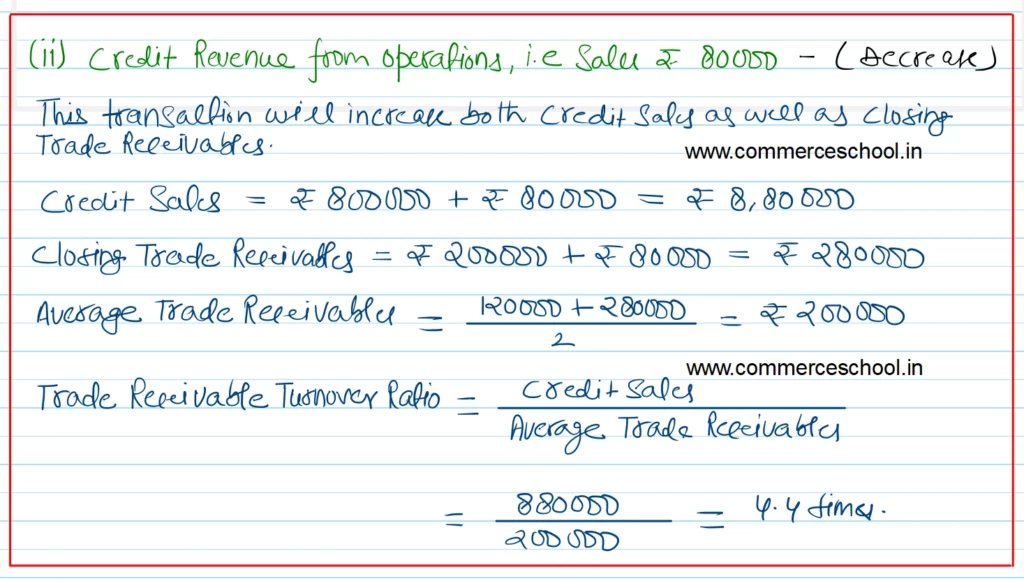

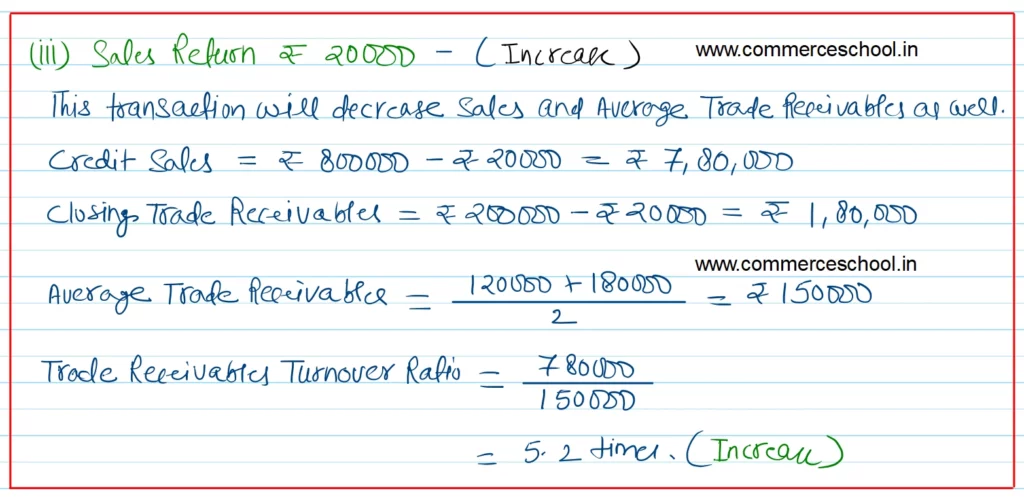

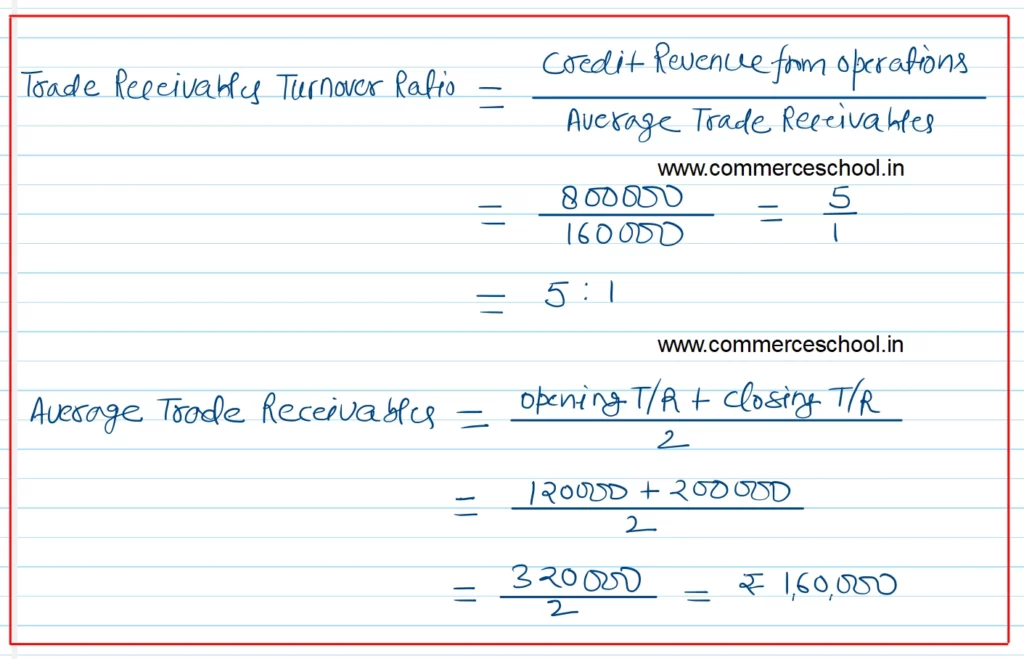

Q. 105. From the information given below, calculate Trade Receivables Turnover Ratio.

Credit Revenue from Operations, i.e., Credit sales ₹ 8,00,000; Opening Trade Receivables ₹ 1,20,000 AND Closing Trade Receivables ₹ 2,00,000.

State, giving reason, which of the following would increase, decrease or not change Trade Receivables Turnover Ratio:

(i) Collection from Trade Receivables ₹ 40,000.

(ii) Credit Revenue from Operation, i.e., Credit Sales ₹ 80,000.

(iii) Sales Return ₹ 20,000.

(iv) Credit Purchase ₹ 1,60,000.

[Ans. Trade Receivables Turnover Ratio = 5 Times: (i) Increase; (ii) Decrease; (iii) Increase; (iv) No Change.]

Solution:-

(i) Collection from Trade Receivables ₹ 40,000

Let’s break down the impact of collecting ₹ 40,000 from trade receivables on the Trade Receivables Turnover Ratio step by step:

Trade Receivables Turnover Ratio Formula:

Trade Receivables Turnover Ratio

= Credit Revenue from OperationsAverage Trade Receivables

Where:

Credit Revenue from Operations: ₹ 8,00,000 (unchanged in this case)

Average Trade Receivables: Calculated as:

Average Trade Receivables = Opening Trade Receivables + Closing Trade Receivables

Step 1: Current Average Trade Receivables

Average Trade Receivables (before collection)} = 1,20,000 + 2,00,000= ₹ 1,60,000

Step 2: Current Trade Receivables Turnover Ratio

Trade Receivables Turnover Ratio (before collection)

= 8,00,000/1,60,000 = 5 times

Step 3: Impact of Collection

The Collection of ₹ 40,000 will reduce the closing trade receivables, changing the closing balance to:

2,00,000 – 40,000 = ₹ 1,60,000

Step 4: Revised Average Trade Receivables

Average Trade Receivables (after collection)

= 1,20,000 + 1,60,000}{2} = ₹ 1,40,000

Step 5: Revised Trade Receivables Turnover Ratio

Trade Receivables Turnover Ratio (after collection)

= 8,00,000/1,40,000 = approx 5.71 times

Impact:

The Trade Receivables Turnover Ratio increases from 5 times to approximately 5.71 times, indicating improved efficiency in the collection of receivables.