[CBSE] Q. 158,159,160,161 Solution of Accounting Ratios TS Grewal Class 12 (2026-27)

Solution of Question 158, 159, 160, 161 Accounting Ratios of TS Grewal Book 2026-27 session CBSE Board

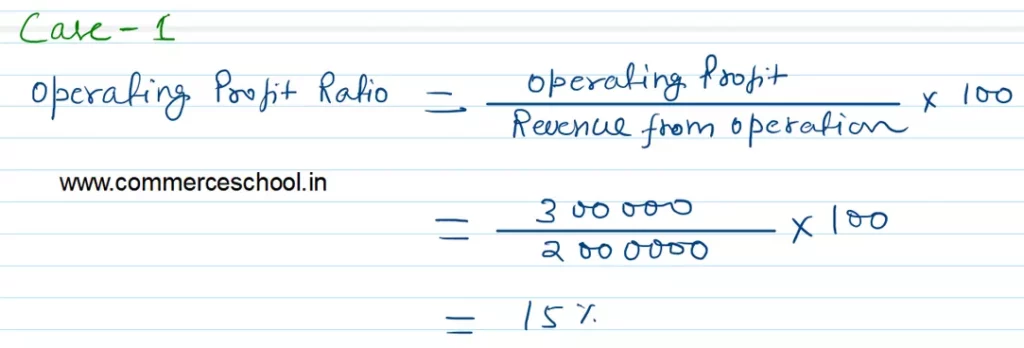

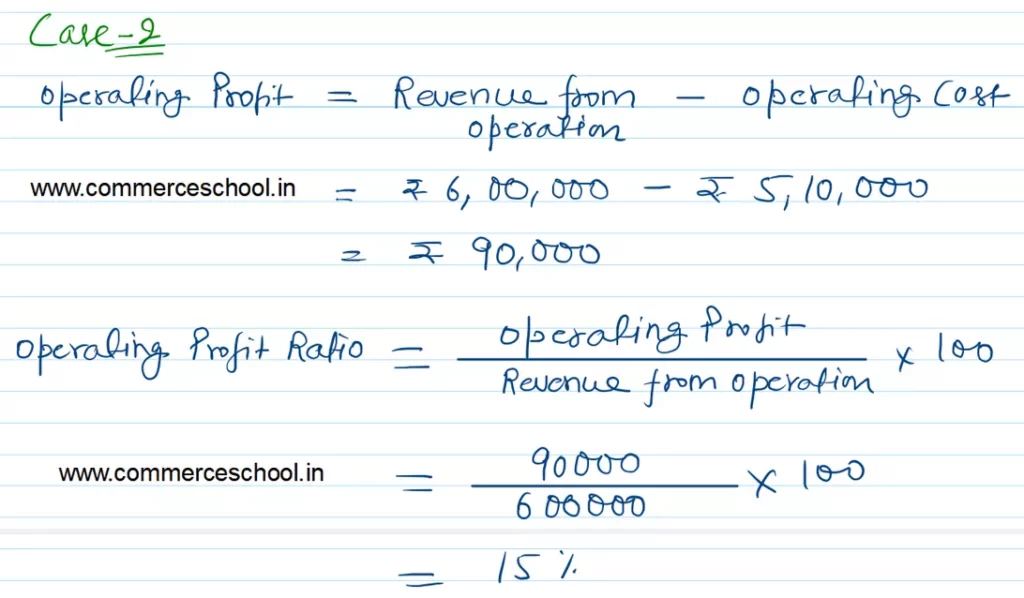

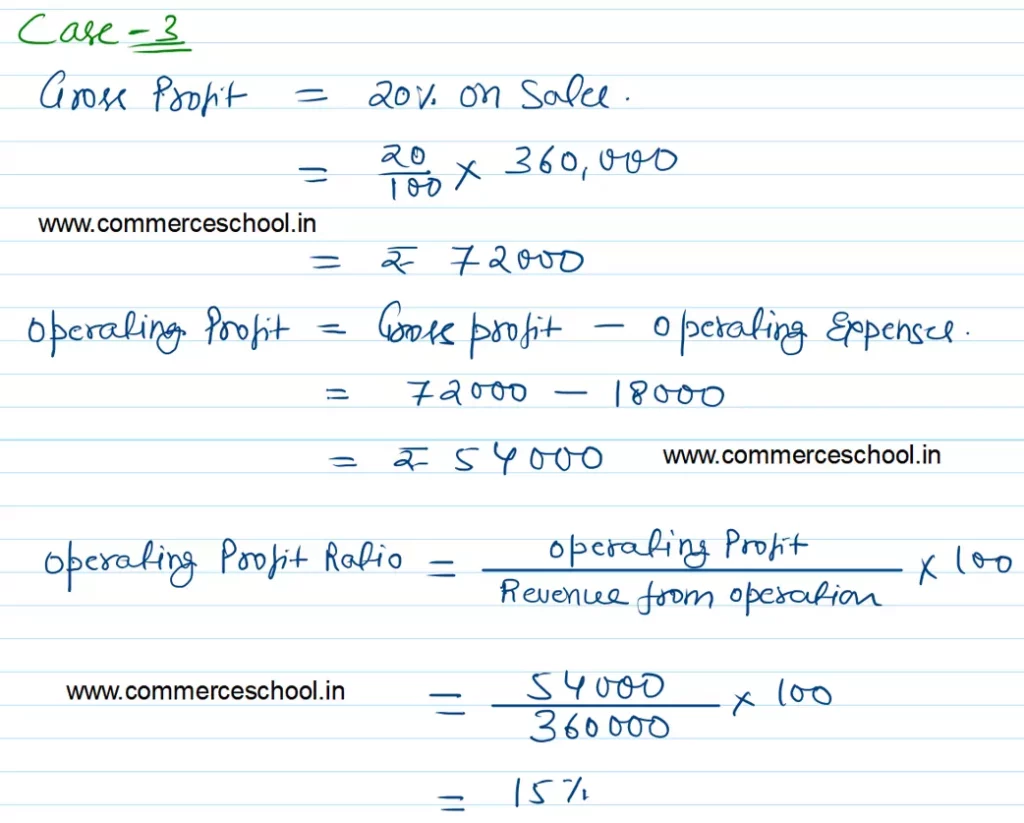

Q. 158. Calculate Operating Profit Ratio in each of the following alternative cases:

Case 1: Revenue from Operations (Net Sales) ₹ 20,00,000; Operating Profit ₹ 3,00,000.

Case 2: Revenue from Operations (Net Sales) ₹ 6,00,000; Operating Cost ₹ 5,10,000.

Case 3: Revenue from Operations (Net Sales) ₹ 3,60,000; Gross Profit 20% on Sales; Operating Expenses ₹ 18,000.

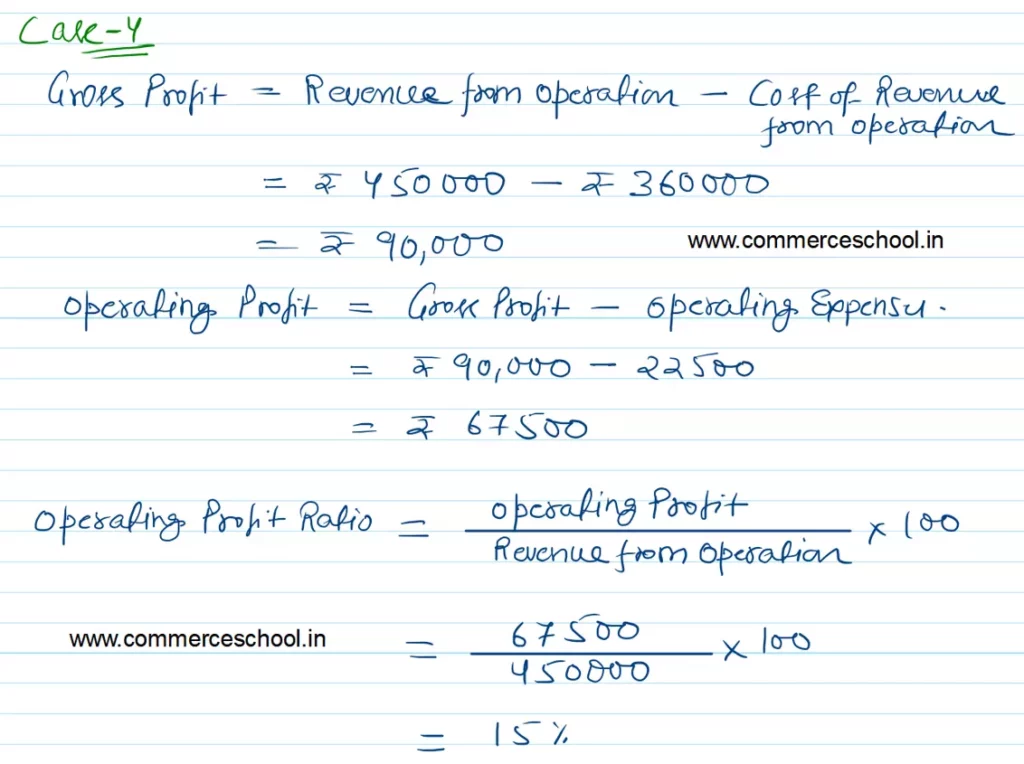

Case 4: Revenue from Operations (Net Sales) ₹ 4,50,000; Cost of Revenue from Operations ₹ 3,60,000; Operating Expenses ₹ 22,500.

Case 5: Cost of Goods Sold, i.e., Cost of Revenue from Operations ₹ 4,00,000; Gross Profit 20% on Sales; Operating Expenses ₹ 25,000.

[Ans.: Case 1 = 15%; Case 2 = 15%; Case 3 = 15%; Case 4 = 15%; Case 5 = 15%.]

Solution:-

Q. 159. Operating Profit Ratio of Star Ltd. is 20%. State, giving reason, which of the following transactions will (i) increase, (ii) decrease, or (iii) not alter the Operating Profit Ratio:

(a) Purchase of Stock-in-Trade ₹ 1,00,000.

(b) Purchase returns ₹ 20,000.

(c) Revenue from Operations on sale of Stock-in-Trade ₹ 1,25,000.

(d) Stock-in-Trade costing ₹ 25,000 withdrawn for personal use.

Assuming that operating cost is variable, i.e., varies with Revenue from Operations.

[Ans.: (a) No Change; (b) No Change; (c) No Change; (d) No Change.]

Solution:-

(a) Purchase of Stock-in-Trade ₹ 1,00,000 – No Change

Reason:- Purchase of stock in Trade increases purchases and closing inventory. This transactions does not impact cost of revenue from operations and net revenue from operations. Thus no change in operating profit.

(b) Purchase Returns ₹ 20,000 – No Change

Reason:- Purchases Returns reduces Purchases and Closing inventory as well. Thus there is no change in Cost of Revenue from Operations and Net Revenue from Operations. Thus no change in Operating Profit.

(c) Revenue from Operations on sale of Stock-in-Trade ₹ 1,25,000. – No Change

Let’s Assume Revenue from Operations be ₹ 10,00,000

Operating Profit = 10,00,000 x 20% = ₹ 2,00,000

New Revenue from Operations After sale

= ₹ 10,00,000 + ₹ 1,25,000

= ₹ 11,25,000

New Operating Profit

= 2,00,000 + 1,25,000 x 20%

= ₹ 2,00,000 + ₹ 25,000 = ₹ 2,25,000

New Operating Profit Ratio

= 2,25,000/11,25,000 x 100 = 20%

(d) Stock-in-Trade Costing ₹ 25,000 withdrawn for personal use. – No Change

It will decrease Purchase of stock in trade and closing inventory with the same amount. Thus Cost of revenue from operations will remain same. As Revenue from operations is not affected, operating profit is also intact.

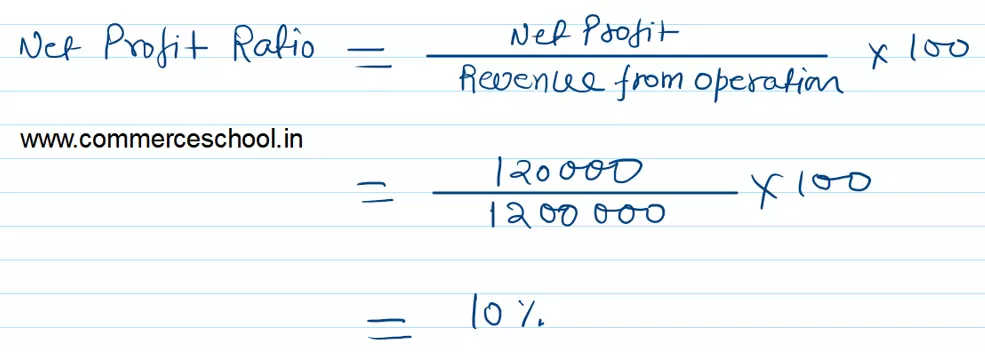

Q. 160. Revenue from Operations, i.e., Net Sales ₹ 12,00,000; Net Profit ₹ 1,20,000; Calculate Net Profit Ratio.

[Ans.: Net Profit Ratio = 10%.]

Solution:-

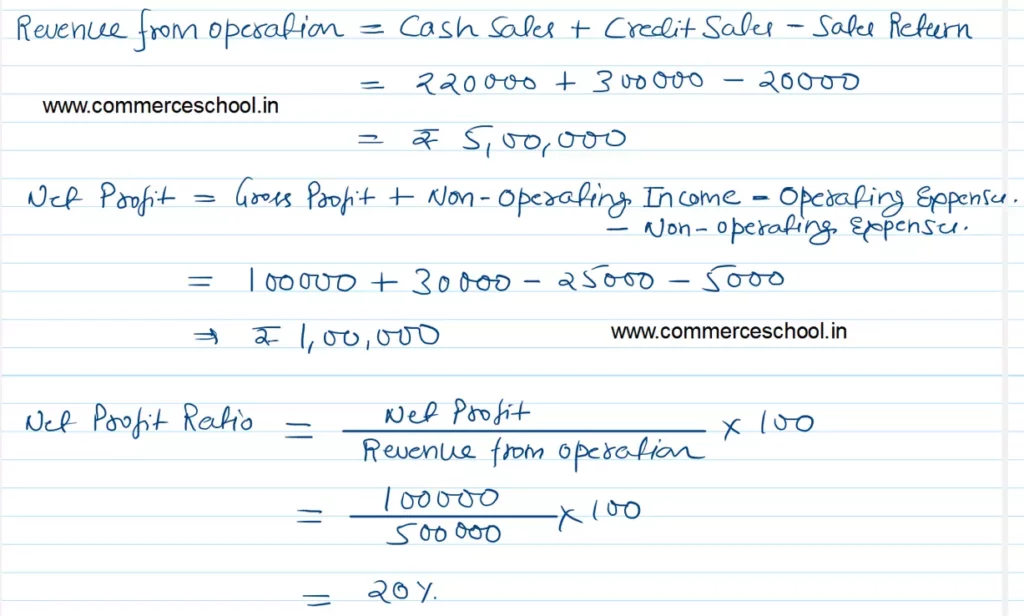

Q. 161. Cash Sales ₹ 2,20,000; Credit Sales ₹ 3,00,000; Sales Return 20,000;

Gross Profit ₹ 1,00,000; Operating Expenses ₹ 25,000; Non-Operating Incomes ₹ 30,000; Non-operating Expenses ₹ 5,000. Calculate Net Profit Ratio.

[Ans.: Net Profit Ratio = 20%.]

Solution:-