[CBSE] Q. 45,46,47,48 Solution of Accounting Ratios TS Grewal Class 12 (2026-27)

Solution of Question 45, 46, 47, 48 Accounting Ratios of TS Grewal Book 2026-27 session CBSE Board

Q. 45. When Debt to Equity Ratio is 2, State, giving reason, whether this ratio will increase, decrease or will have no change in each of the following cases:

(i) Sale of Land (Book value ₹ 4,00,000) for ₹ 5,00,000;

(ii) Issue of Equity Shares for the purchase of Plant and Machinery worth ₹ 10,00,000;

(ii) Issue of Preference Shares for redemption of 13% Debentures, worth ₹ 10,00,000.

[Ans.: (i) Decrease; (ii) Decrease; (iii) Decrease.]

Solution:-

(i) Sale of Land (Book value ₹ 4,00,000) for ₹ 5,00,000

The sale of land at a profit (₹ 4,00,000 book value sold for ₹ 5,00,000) can impact the debt-to-equity ratio, depending on how the proceeds are used. Let’s break this down:

Debt-to-Equity Ratio Formula:

= Debt/Equity

- Impact of the Sale:

- The book value of the land (₹ 4,00,000) is removed from assets, and the sale proceeds (₹ 5,00,000) are added to cash or bank balances.

- A profit of ₹ 1,00,000 (sale price ₹ 5,00,000 minus book value ₹ 4,00,000) is recognized and added to reserves/retained earnings, increasing shareholders’ equity.

- Debt Unchanged:

- If the company does not use the proceeds to pay off debt, the total debt remains unchanged.

- Final Effect:

- Since shareholders’ equity increases due to the profit, the denominator of the ratio increases, leading to a lower debt-to-equity ratio (better financial position).

(ii) Issue of Equity Shares for the purchase of Plant and Machinery worth ₹ 10,00,000;

The issuance of equity shares for purchasing plant and machinery worth ₹ 10,00,000 affects the debt-to-equity ratio as follows:

Debt-to-Equity Ratio Formula:

= Debt/Equity

- Impact of the Transaction:

- The purchase of plant and machinery does not involve cash or debt; instead, equity shares are issued to finance the purchase.

- This transaction increases shareholders’ equity, as the equity capital rises by ₹ 10,00,000 due to the issuance of shares.

- Debt Unchanged:

- Since no debt is taken on to finance the purchase, the total debt remains unchanged.

- Final Effect:

- The denominator of the ratio (shareholders’ equity) increases while the numerator (total debt) stays the same. This results in a lower debt-to-equity ratio, indicating an improved financial position with reduced leverage.

(iii) Issue of Preference Shares for redemption of 13% Debentures, worth ₹ 10,00,000.

The issuance of preference shares for the redemption of 13% debentures worth ₹ 10,00,000 impacts the debt-to-equity ratio as follows:

Debt-to-Equity Ratio Formula:

= Debt/Equity

- Impact of the Transaction:

- Debenture Redemption: By redeeming ₹ 10,00,000 worth of 13% debentures, the company’s total debt decreases since debentures are part of long-term liabilities.

- Issuance of Preference Shares: Preference shares are part of shareholders’ equity, so issuing them increases equity.

- Final Effect:

- The numerator (total debt) decreases, and the denominator (shareholders’ equity) increases. This results in a lower debt-to-equity ratio, reflecting reduced leverage and an improved financial position.

Q. 46. Debt to Equity Ratio of a company is 0.5 : 1. Which of the following would increase, decrease or not change it:

(i) Issue of Equity Shares;

(ii) Cash received from debtors;

(iii) Redemption of debentures;

(iv) Purchased goods on credit?

[Ans.: (i) Decrease; (ii) No change; (iii) No change; (iv) No change.]

Solution:-

(i) Issue of Equity Shares;

The issue of equity shares directly impacts the debt-to-equity ratio in the following way:

- Debt-to-Equity Ratio Formula:

= Debt/Equity

- Impact of Equity Shares:

- When equity shares are issued, the shareholders’ equity increases because the funds raised from the issue are added to the equity capital of the company.

- This increases the denominator of the debt-to-equity ratio.

- Debt Unchanged:

- The issuance of equity shares does not involve borrowing, so total debt remains unchanged.

- Final Effect:

- Since shareholders’ equity rises, the debt-to-equity ratio decreases, indicating reduced financial leverage and a stronger equity base.

(ii) Cash received from debtors;

The receipt of cash from debtors does not directly affect the debt-to-equity ratio. Here’s why:

- Debt-to-Equity Ratio Formula:

= Debt/Equity

- Impact of Cash Receipt:

- When cash is received from debtors, there is simply a reallocation within the current assets—accounts receivable decreases, and cash increases by the same amount.

- This transaction does not affect total debt (numerator) or shareholders’ equity (denominator).

- Final Effect:

- Since neither debt nor equity changes, the debt-to-equity ratio remains unchanged.

(iii) Redemption of debentures;

The redemption of debentures affects the debt-to-equity ratio as follows:

- Debt-to-Equity Ratio Formula:

= Debt/Equity

- Impact of Redemption:

- When debentures are redeemed, the company’s long-term debt decreases, as debentures are part of long-term liabilities.

- The payment for redemption usually comes from cash or bank balances, which does not directly impact shareholders’ equity.

- Final Effect:

- As the numerator (total debt) decreases while the denominator (shareholders’ equity) remains constant, the debt-to-equity ratio decreases. This indicates reduced leverage and an improved financial position.

(iv) Purchased goods on credit?

If we consider debt only as long-term liabilities, the purchase of goods on credit typically does not directly affect the debt-to-equity ratio. Here’s why:

- Debt-to-Equity Ratio Formula:

= Debt/Equity

- Impact of the Transaction:

- When goods are purchased on credit, it creates current liabilities, such as accounts payable.

- Current liabilities are not included in the debt figure for the debt-to-equity ratio if we’re only focusing on long-term liabilities.

- Therefore, neither the numerator (long-term liabilities) nor the denominator (shareholders’ equity) changes.

- Final Effect:

- Since there is no change in long-term debt or equity, the debt-to-equity ratio remains unchanged.

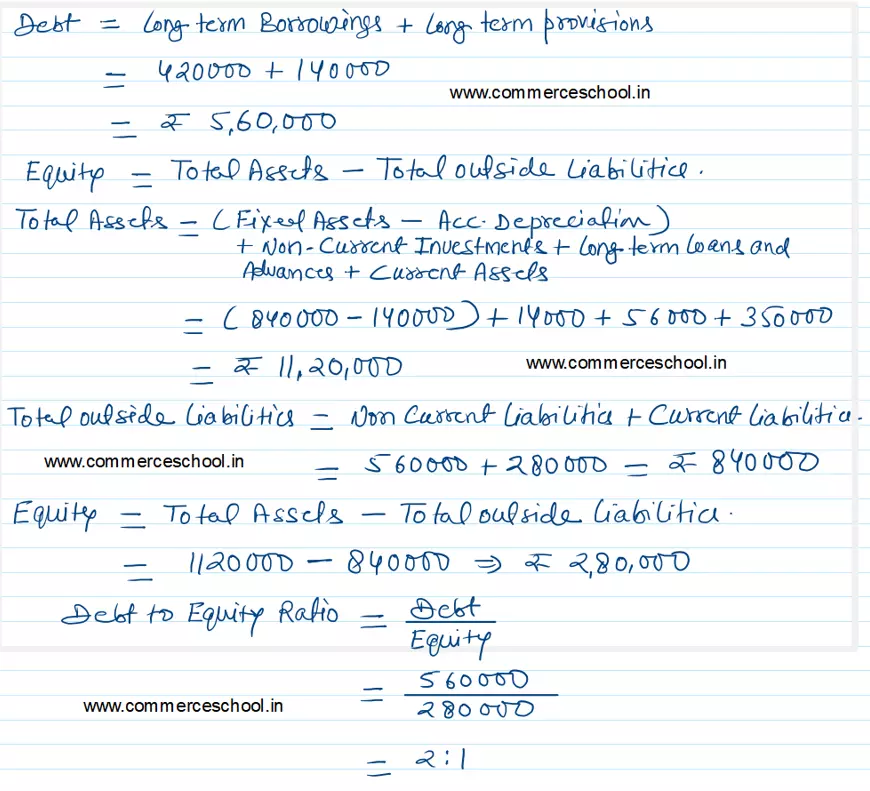

Q. 47. Calculate Debt to Equity Ratio from the following information:

| Property, Plant and Equipment (Gross) | 8,40,000 |

| Accumulated Depreciation | 1,40,000 |

| Non-Current Investments | 14,000 |

| Long-term Loans and Advances | 56,000 |

| Current Assets | 3,50,000 |

| Current Liabilities | 2,80,000 |

| 10% Long term Borrowings | 4,20,000 |

| Long-term Provisions | 1,40,000 |

[Ans.: Debt to Equity Ratio = 2 : 1.]

Solution:-

Q. 48. Assuming that the Debt to Equity Ratio is 2 : 1, State, giving reasons, which of the following transactions would (i) Increase, (ii) Decrease, (iii) Not alter Debt to Equity RAtio:

(i) Issue of new shares for cash.

(ii) Conversion of debentures into equity shares.

(iii) Sale of a fixed asset at profit.

(iv) Purchase of a fixed asset on long-term deferred payment basis.

(v) Payment to creditors.

[Ans.: (i) Decrease; (ii) Decrease; (iii) Decrease; (iv) Increase; (v) No change.]

Solution:-

(i) Issue of new shares for cash.

The debt-to-equity ratio measures the proportion of debt to equity in a company’s capital structure. Issuing new shares for cash increases equity, while debt remains unchanged, leading to a reduction in the debt-to-equity ratio.

Before the issuance of new shares:

- Debt: ₹ 2,00,000

- Equity: ₹ 1,00,000

- Debt-to-Equity Ratio: 2,00,000/1,00,000 = 2 : 1

After the issuance of new shares:

Let’s assume the company issues shares worth ₹ 50,000.

- Debt: ₹ 2,00,000 (unchanged)

- Equity: ₹ 1,00,000 + ₹ 50,000 = ₹ 1,50,000

- Debt-to-Equity Ratio: 2,00,0001,50,000 = 1.33 : 1

Impact: The debt-to-equity ratio decreases from 2 : 1 to 1.33 : 1, reflecting a less leveraged capital structure and a stronger equity base. The exact impact depends on the value of shares issued. Let me know if you’d like to refine this with another scenario!