[CBSE] Q. 52 Cash Flow Statement TS Grewal Class 12 2023-24

Solution of Question number 52 of the Cash Flow Statement of TS Grewal Book 2023-24 session?

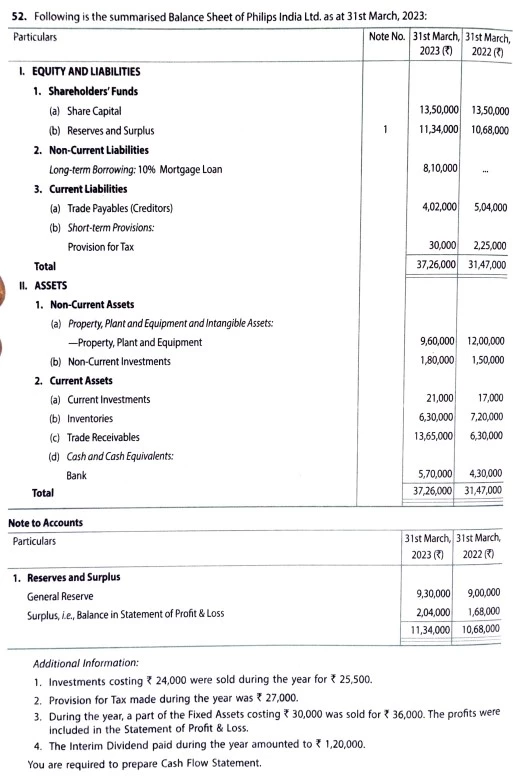

Following is the summarised Balance Sheet of Philips India Ltd. as at 31st March, 2023:

| Particulars | 31st March, 2023 (₹) | 31st March, 2022 (₹) |

| I. EQUITY AND LIABILITIES | ||

| Shareholder’s Funds (a) Share Capital (b) Reserves and Surplus | 13,50,000 11,34,000 | 13,50,000 10,68,000 |

| Non-Current Liabilities Long-term Borrowings: 10% Mortgage Loan | 8,10,00 | – |

| Current Liabilities (a) Trade Payables (Creditors) (b) Short-term Provisions: Provision for Tax | 4,02,000 30,000 | 5,04,000 2,25,000 |

| Total | 37,26,000 | 31,47,000 |

| II. Assets | ||

| Non-Current Assets (a) Property, Plant and Equipment and Intangible Assets: Property, Plant and Equipment (b) Non-Current Investments | 9,60,000 1,80,000 | 12,00,000 1,50,000 |

| Current Assets (a) Current Investments (b) Inventories (c) Trade Receivables (d) Cash and Cash Equivalents Bank | 21,000 6,30,000 13,65,000 5,70,000 | 17,000 7,20,000 6,30,000 4,30,000 |

| Total | 37,26,000 | 31,47,000 |

| Particulars | 31st March, 2023 (₹) | 31st March, 2022 (₹) |

| Reserves and Surplus General Reserve Surplus, i.e., Balance in Statement of Profit & Loss | 9,30,000 2,04,000 | 9,00,000 1,68,000 |

| 11,34,000 | 10,68,000 |

Additional Information:

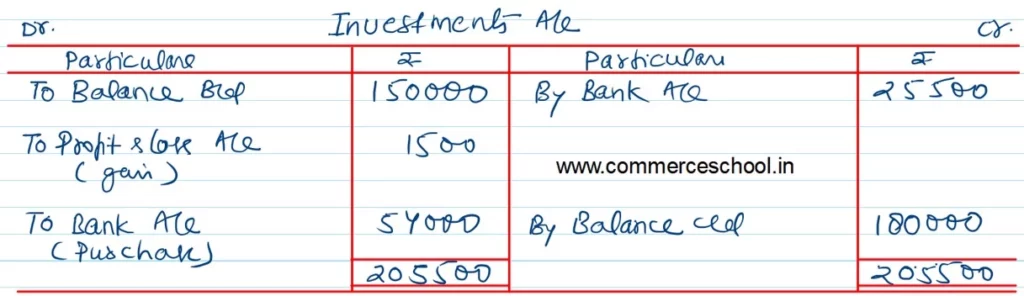

- Investments costing ₹ 24,000 were sold during the year for ₹ 25,500.

- Provision for Tax made during the year was ₹ 27,000.

- During the year, a part of the Fixed Assets Costing ₹ 30,000 was sold for ₹ 36,000. The profits were included in the statement of Profit & Loss.

- The Interim Dividend paid during the year amounted to ₹ 1,20,000.

You are required to Prepare Cash Flow Statement.

[Ans.: Cash Used in Operating Activities = ₹ 5,53,000; Cash Flow from Investing Activities = ₹ 7,500; Cash Flow from Financing Activities = ₹ 6,90,000; Net Increase in Cash and Cash Equivalents = ₹ 1,44,000.]

Solution:-

Here is the list of all Solutions.

| S.N | Solutions |

| 1 | Question – 1 |

| 2 | Question – 2 |

| 3 | Question – 3 |

| 4 | Question – 4 |

| 5 | Question – 5 |

| 6 | Question – 6 |

| 7 | Question – 7 |

| 8 | Question – 8 |

| 9 | Question – 9 |

| 10 | Question – 10 |

| S.N | Solutions |

| 11 | Question – 11 |

| 12 | Question – 12 |

| 13 | Question – 13 |

| 14 | Question – 14 |

| 15 | Question – 15 |

| 16 | Question – 16 |

| 17 | Question – 17 |

| 18 | Question – 18 |

| 19 | Question – 19 |

| 20 | Question – 20 |

| S.N | Solutions |

| 21 | Question – 21 |

| 22 | Question – 22 |

| 23 | Question – 23 |

| 24 | Question – 24 |

| 25 | Question – 25 |

| 26 | Question – 26 |

| 27 | Question – 27 |

| 28 | Question – 28 |

| 29 | Question – 29 |

| 30 | Question – 30 |

| S.N | Solutions |

| 31 | Question – 31 |

| 32 | Question – 32 |

| 33 | Question – 33 |

| 34 | Question – 34 |

| 35 | Question – 35 |

| 36 | Question – 36 |

| 37 | Question – 37 |

| 38 | Question – 38 |

| 39 | Question – 39 |

| 40 | Question – 40 |

| S.N | Solutions |

| 41 | Question – 41 |

| 42 | Question – 42 |

| 43 | Question – 43 |

| 44 | Question – 44 |

| 45 | Question – 45 |

| 46 | Question – 46 |

| 47 | Question – 47 |

| 48 | Question – 48 |

| 49 | Question – 49 |

| 50 | Question – 50 |

| S.N | Solutions |

| 51 | Question – 51 |

| 52 | Question – 52 |

| 53 | Question – 53 |

| 54 | Question – 54 |

| 55 | Question – 55 |

| 56 | Question – 56 |

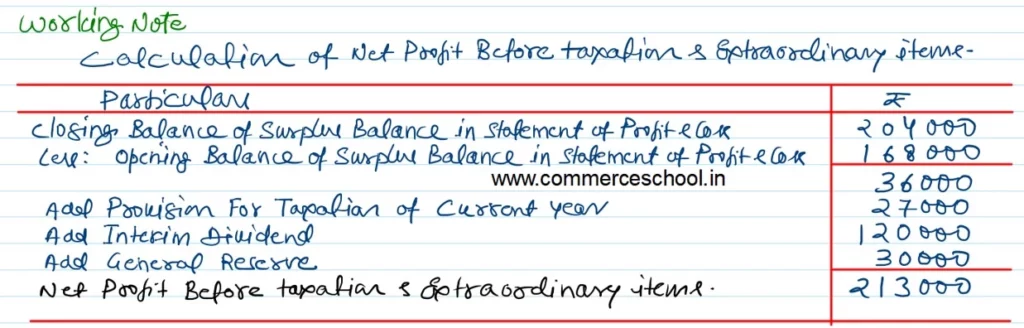

Sir you didn’t show the working of net profit before tax and extraordinary items

Updated, thanks for informing