[DK Goel] Q. 161,162,163,164 Accounting Ratios Solutions Class 12 CBSE (2026-27)

the solutions of Question number 161, 162, 163, 164 of Accounting Ratios chapter 5 of DK Goel Class 12 CBSE (2026-27)

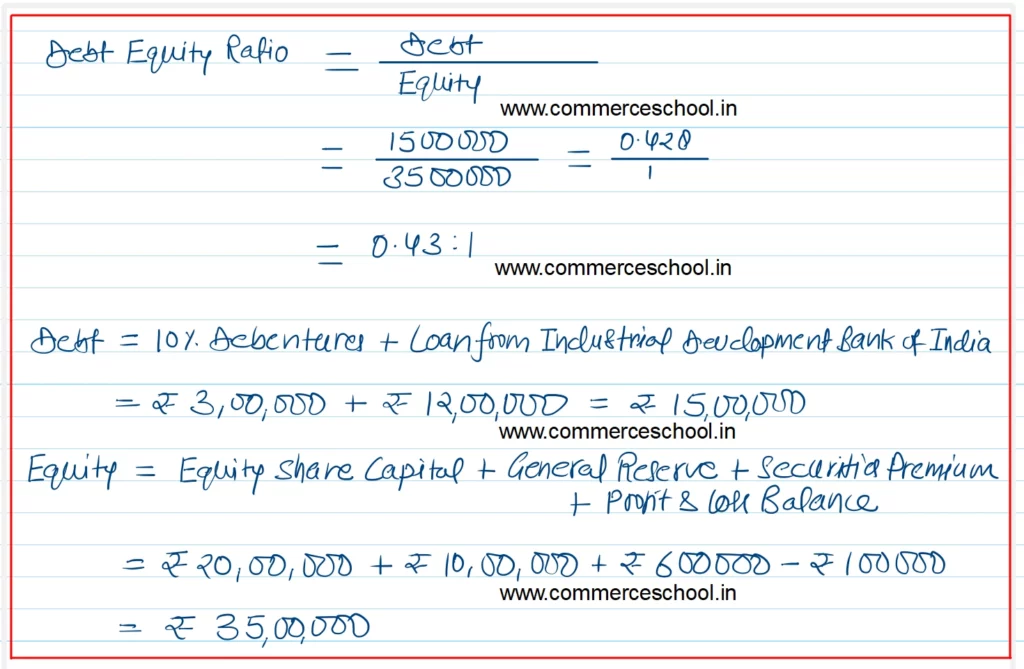

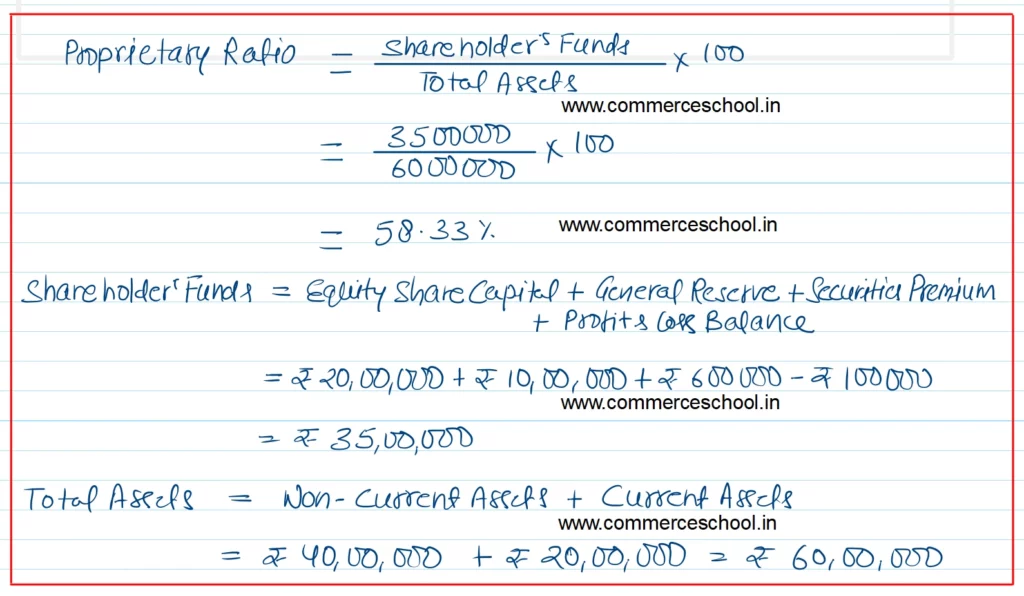

Q. 161. From the following, ascertain Debt-Equity Ratio and Proprietary Ratio:-

| ₹ | |

| Equity Share Capital | 20,00,000 |

| General Reserve | 10,00,000 |

| Securities Premium | 6,00,000 |

| Profit & Loss Balance | (1,00,000) |

| 10% Debentures | 3,00,000 |

| Loan from Industrial Development Bank of India (I.D.B.I) | 12,00,000 |

| Current Liabilities | 10,00,000 |

| Non-Current Assets | 40,00,000 |

| Current Assets | 20,00,000 |

[Ans.]

(i) Debt-Equity Ratio = .43 : 1

(ii) Proprietary Ratio = 58.33%

Solution:-

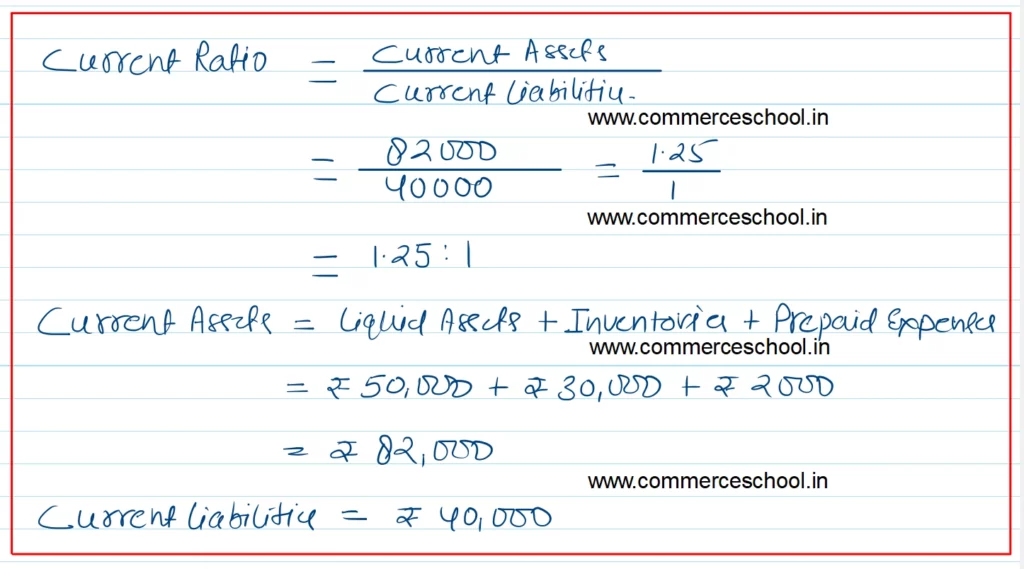

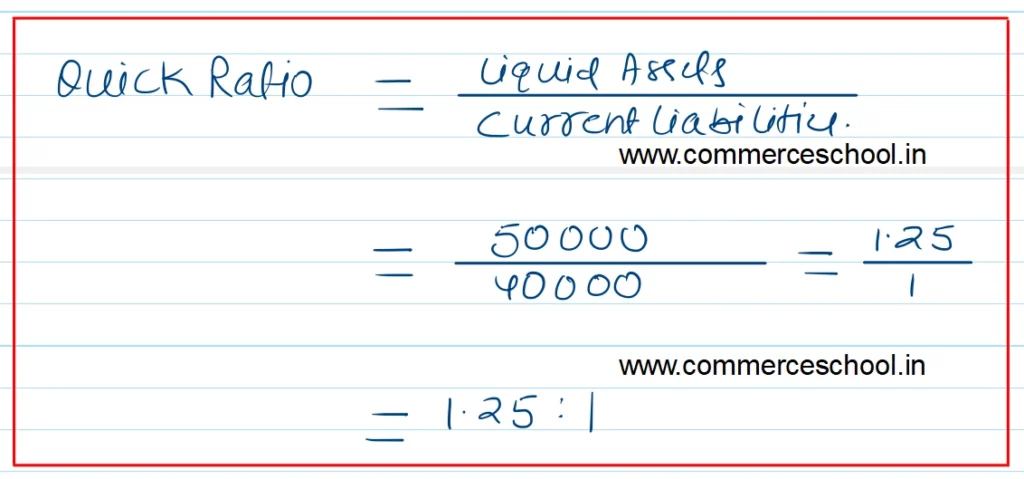

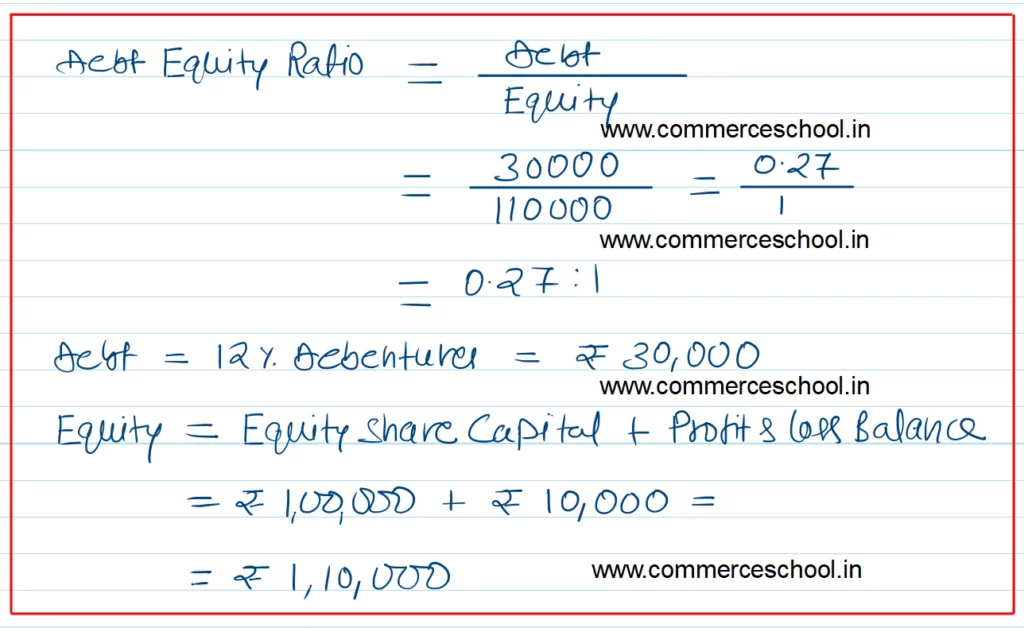

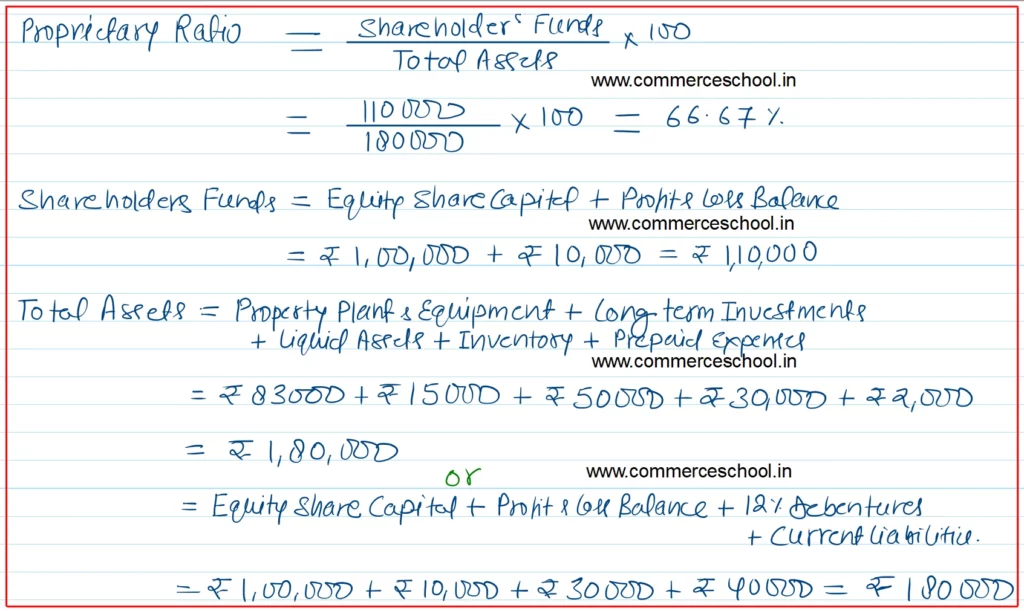

Q. 162. Calculate Current Ratio, Quick Ratio, Debt-Equity Ratio and the Proprietary Ratio from the figures given below:-

| Inventory | 30,000 |

| Prepaid Expenses | 2,000 |

| Liquid Assets | 50,000 |

| Current Liabilities | 40,000 |

| 12% Debentures | 30,000 |

| Profit & Loss Balance | 10,000 |

| Equity Share Capital | 1,00,000 |

| Long term Investments | 15,000 |

| Property, Plant and Equipment | 83,000 |

[Ans.]

(i) Current Ratio 2.05 : 1, (ii) Quick Ratio 1.25 : 1; (iii) Debt-Equity Ratio .27 : 1; (iv) Proprietary Ratio i.e., 61.11%.]

Solution:-

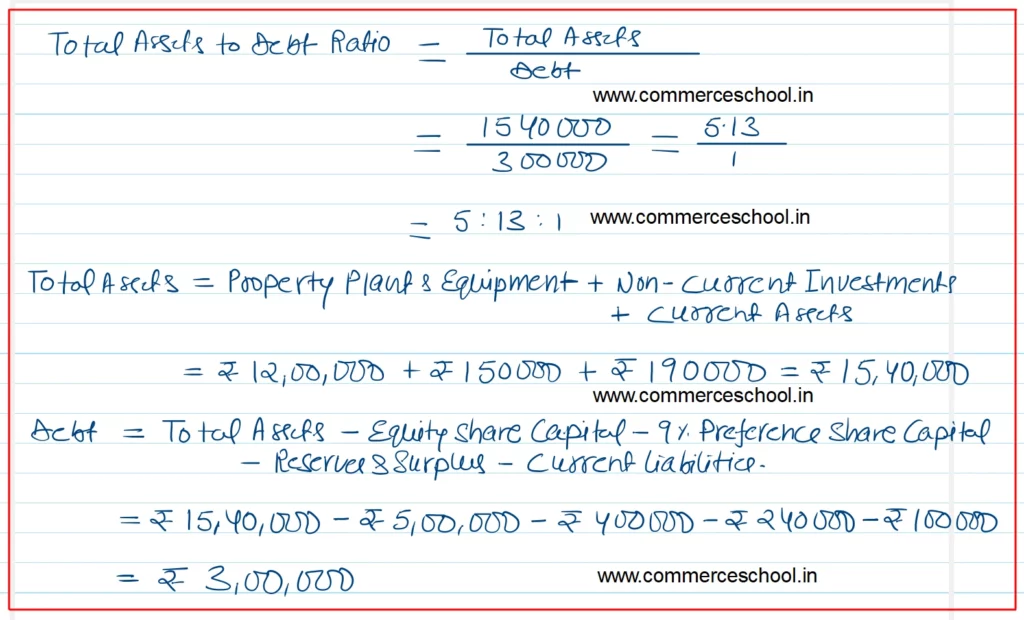

Q. 163. From the following information of Shiva Ltd., Calculate total assets to debt ratio:-

| Equity Share Capital | 5,00,000 |

| 9% Preference Share Capital | 4,00,000 |

| Property, Plant and Equipment | 12,00,000 |

| Non-Current Investments | 1,50,000 |

| Reserves and Surplus | 2,40,000 |

| Current Assets | 1,90,000 |

| Current Liabilities | 1,00,000 |

[Ans. Total Assets to debt ratio 5.13.]

Solution:-

Hint:-

Total Assets = Property, Plant and Equipment + Non-Current Investment + Current Assets = ₹ 15,40,000

Long-term Debt = ₹ 15,40,000 – Equity Capital – Pref. Capital – Reserves – Current Liabilities = ₹ 3,00,000

Q. 164. Assuming that Debt to Equity Ratio is 0.5 : 1, state, giving reasons whether this ratio will increase or decrease or will have no change in each one of the following cases:

(i) Issue of Preference Shares for Cash.

(ii) Issue of Debentures for Cash.

(iii) Issue of Bonus Shares.

(iv) Repayment of Long term Borrowings.

(v) Conversion of Debentures into Equity Shares.

(vi) Purchase of a Non-Current Asset for Cash.

(vii) Purchase of a Non-Current Asset by taking long-term loan.

(viii) Sale of Non-Current Asset (Book Value ₹ 5,00,000) for ₹ 4,00,000.

(ix) Sale of Non-Current Asset (Book Value ₹ 2,00,000) at a profit of ₹ 50,000.

[Ans. (i) Decrease; (ii) Increase; (iii) No Change; (iv) Decrease; (v) Decrease; (vi) No Change; (vii) Increase; (viii) Increase; (ix) Decrease.]

Solution:-