[DK Goel] Q. 185,186,187,188 Accounting Ratios Solutions Class 12 CBSE (2026-27)

the solutions of Question number 185, 186, 187, 188 of Accounting Ratios chapter 5 of DK Goel Class 12 CBSE (2026-27)

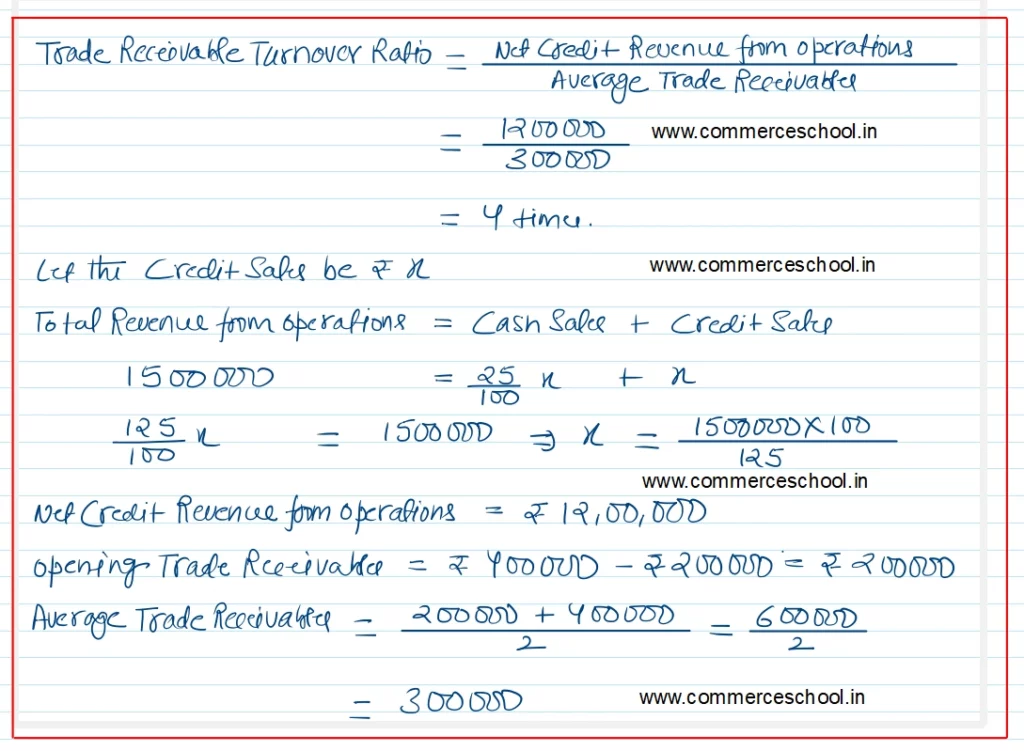

Q. 185. Closing Trade Receivables ₹ 4,00,000; Cash Revenue from Operations being 25% of Credit Revenue from Operations. Excess of Closing Trade Receivables over Opening Trade Receivables ₹ 2,00,000. Total Revenue from Operations ₹ 15,00,000. Calculate Trade Receivables Turnover Ratio.

[Ans. 4 Times.]

Solution:-

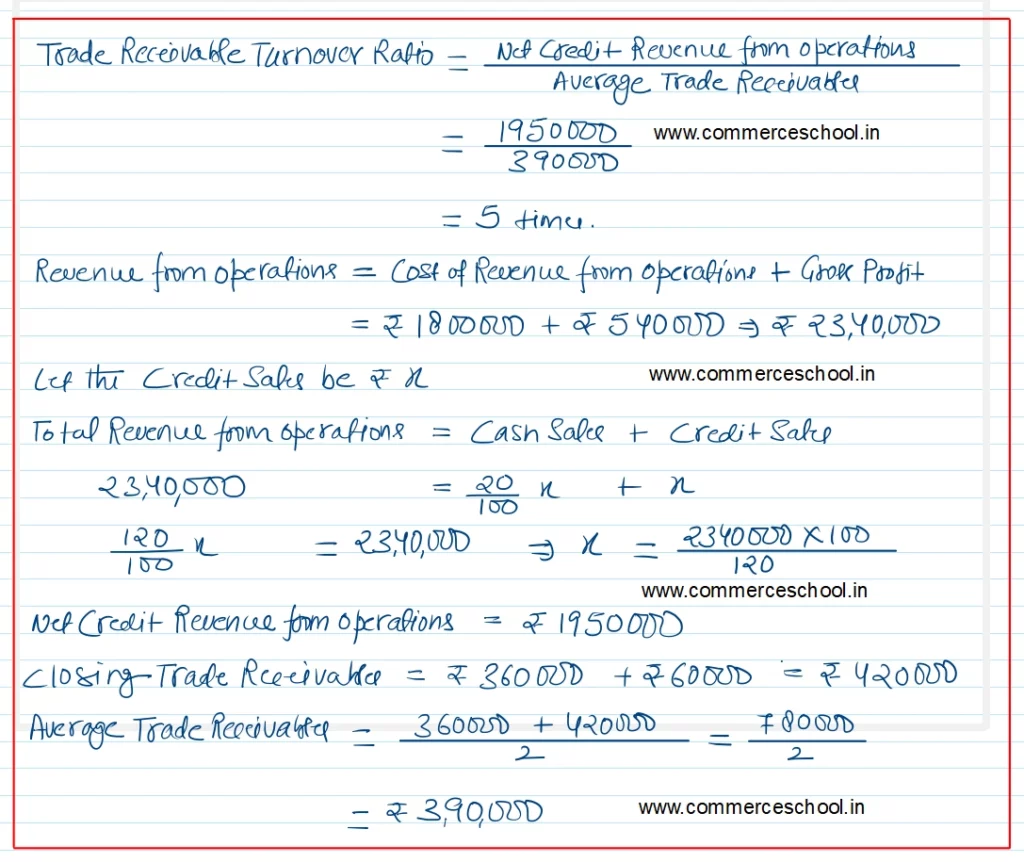

Q. 186. Opening Trade Receivables ₹ 3,60,000; Cash Revenue from Operations being 20% of Credit Revenue from Operations. Excess of Closing Trade Receivables over Opening Trade Receivables ₹ 60,000. Cost of Revenue from Operations ₹ 18,00,000; Gross Profit ₹ 5,40,000. Calculate Trade Receivables Turnover Ratio.

[Ans. 5 Times.]

Solution:-

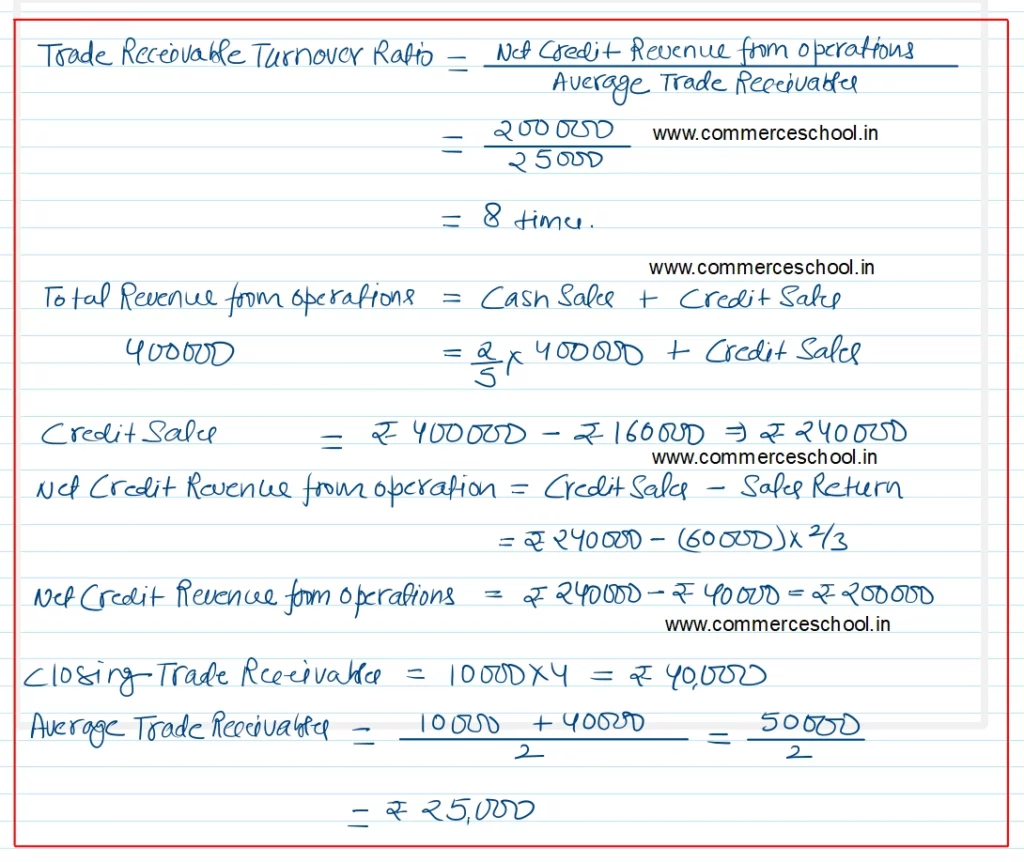

Q. 187. Opening Trade Receivables ₹ 10,000; Total Revenue from Operations (Total Sales) ₹ 4,00,000; Cash Revenue from Operations being 2/5th of Total Revenue from Operations; Revenue from Operations Return (Sales Returns) ₹ 60,000 (1/3rd out of Cash Revenue from Operations); Closing Trade Receivables were four times than that in the beginning. Calculate Trade Receivables Turnover Ratio.

[Ans. Trade Receivables Turnover Ratio 8 Times.]

Solution:-

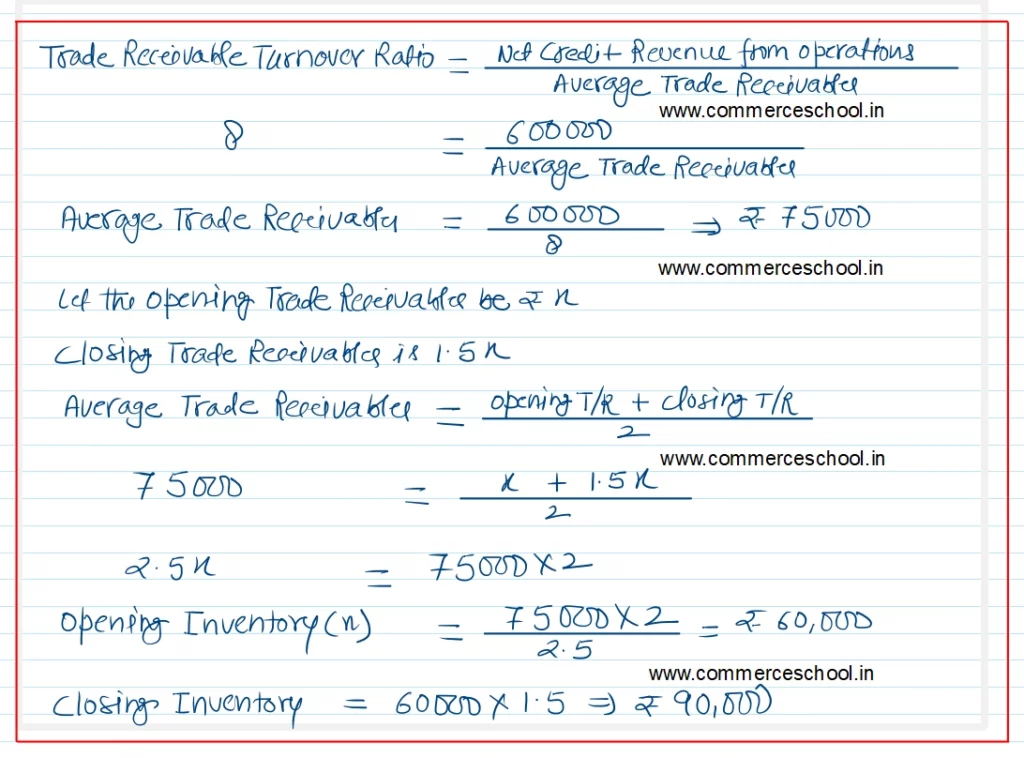

Q. 188. Credit Revenue from Operations ₹ 6,00,000; Trade Receivables Turnover Ratio 8 times; Closing Trade Receivables were 1.5 times than that in the beginning. Calculate Opening and Closing Trade Receivables.

[Ans. Opening Trade Receivables ₹ 60,000; Closing Trade Receivables ₹ 90,000.]

Solution:-