[DK Goel] Q. 57,58,59,60 Accounting Ratios Solutions Class 12 CBSE (2026-27)

the solutions of Question number 57, 58, 59, 60 of Accounting Ratios chapter 5 of DK Goel Class 12 CBSE (2026-27)

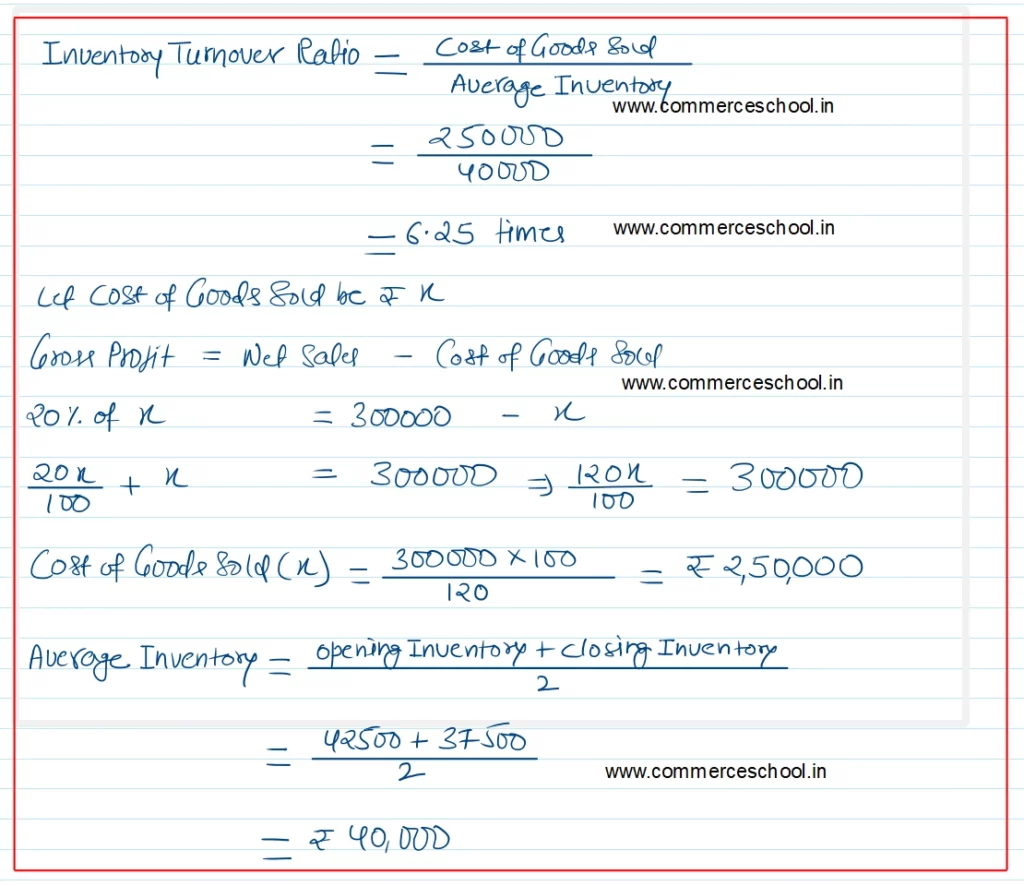

Q. 57. Calculate Inventory Turnover Ratio from the following:

Opening Inventory ₹ 42,500; Closing Inventory ₹ 37,500; Revenue from Operations (Sales) ₹ 3,00,000; Gross Profit 20% on cost.

[Ans. Inventory Turnover Ratio 6.25 times.]

Solution:-

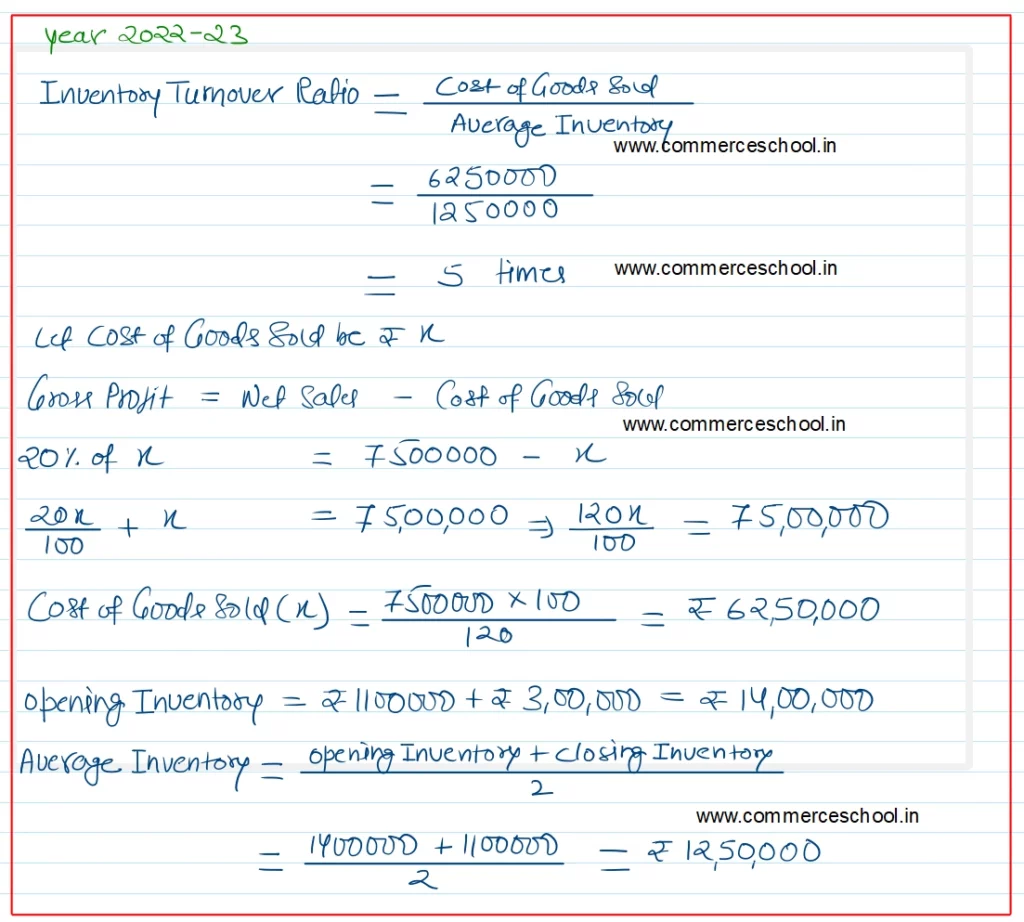

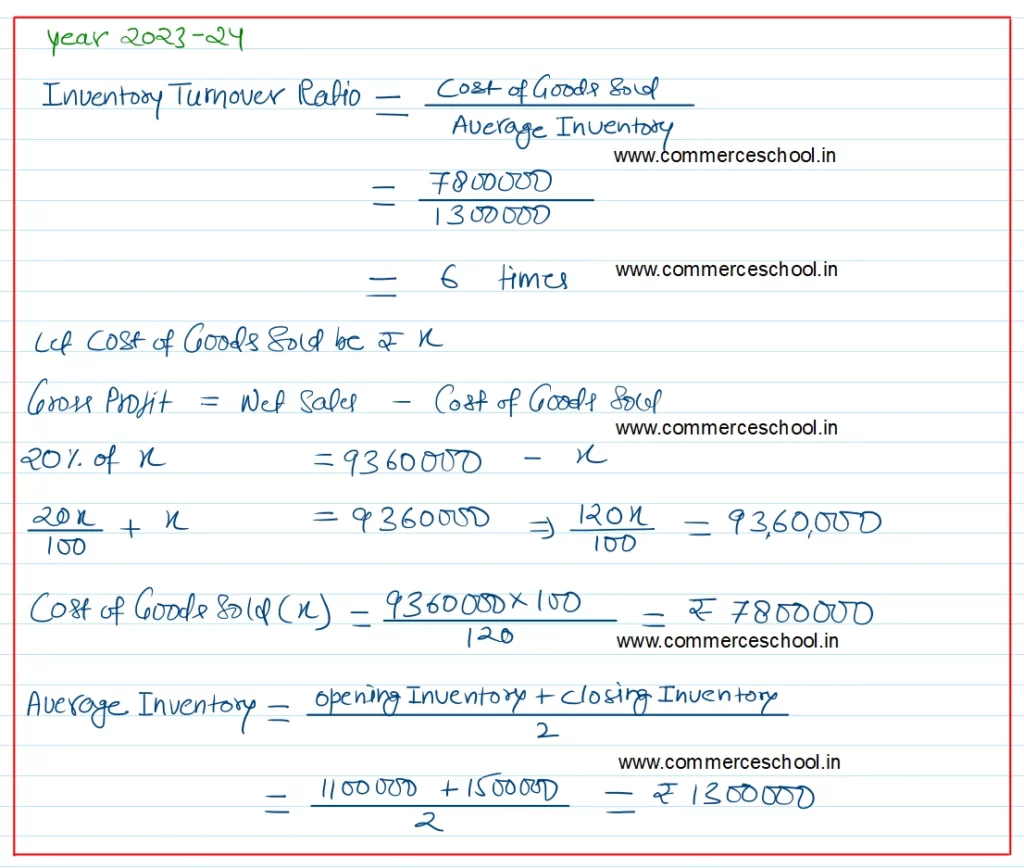

Q. 58. Calculate Inventory Turnover Ratio for the year 2022-23 and 2023-24 from the following information:

| 2022-23 | 2023-24 | |

| Inventory on 31st March | 11,00,000 | 15,00,000 |

| Revenue from Operations (Gross Profit is 20% on cost of revenue from Operations) | 75,00,000 | 93,60,000 |

In the year 2022-23 inventory decreased by ₹ 3,00,000.

[Ans. Inventory Turnover Ratio for 2022-23 : 5 times, for 2023-24 : 6 times]

Solution:-

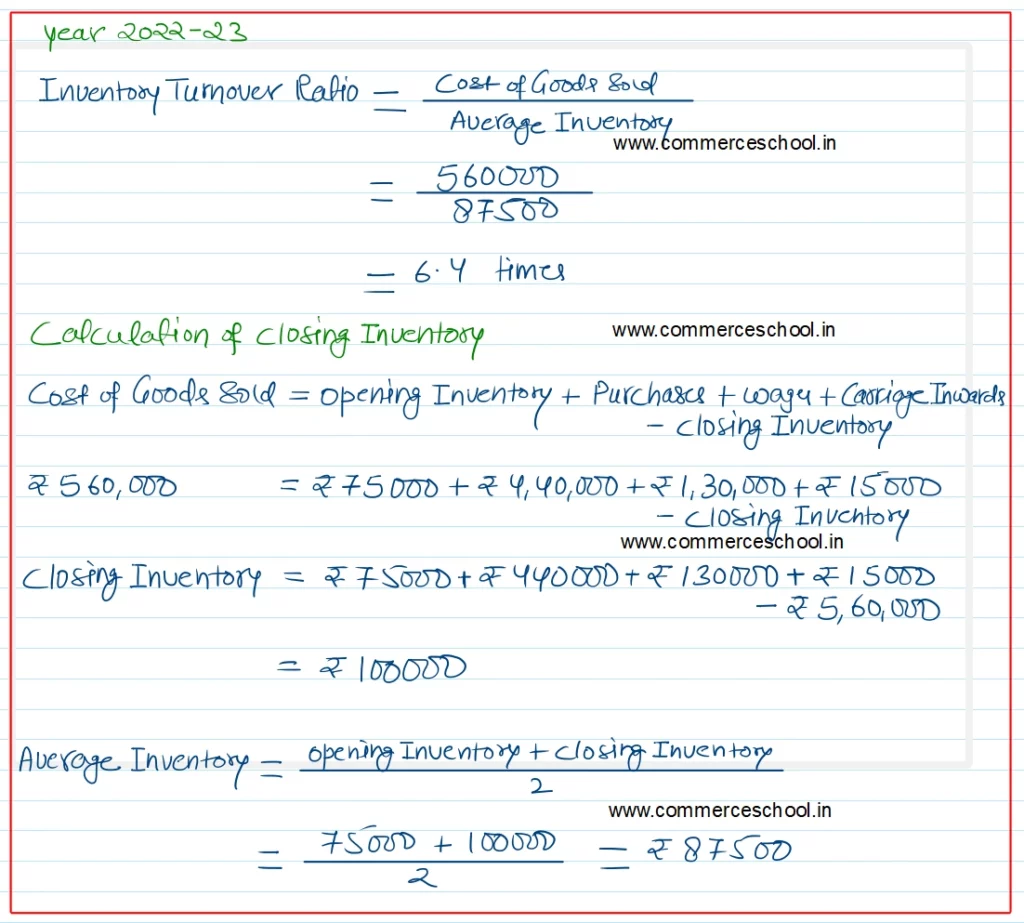

Q. 59. Compute Inventory Turnover Ratio from the following:

| ₹ | |

| Cost of Revenue from Operations (Cost of Goods Sold) | 5,60,000 |

| Purchases | 4,40,000 |

| Wages | 1,30,000 |

| Carriage Inwards | 15,000 |

| Opening Inventory | 75,000 |

[Ans. Closing Inventory ₹ 1,00,000; Inventory Turnover Ratio 6.4 times.]

Hint: Wages and Carriage Inwards are direct expenses. Hence, these will be included in cost of revenue from operations.

Solution:-

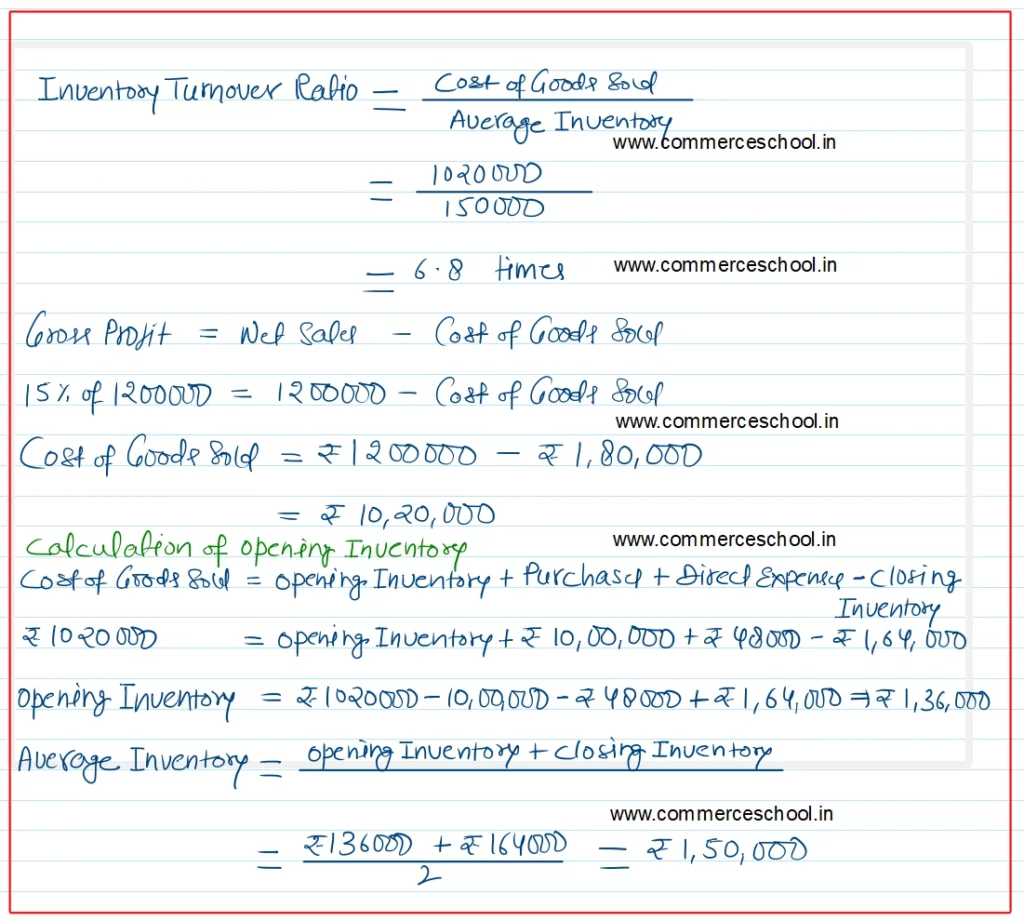

Q. 60. From the following information, calculate Inventory Turnover Ratio:

Purchases ₹ 10,00,000; Revenue from Operations (Sales) ₹ 12,00,000; Direct Expenses ₹ 48,000; Gross Profit Ratio 15% on Revenue from Operations; closing Inventory ₹ 1,64,000.

[Ans. Opening Inventory ₹ 1,36,000; Inventory Turnover Ratio 6.8 times]

Solution:-