[DK Goel] Q. 33, 34 Retirement of Partner Solutions Class 12 CBSE (2026-27)

Here are the solutions of Question number 33 and 34 of Retirement of Partner chapter 5 of DK Goel Class 12 CBSE (2026-27)

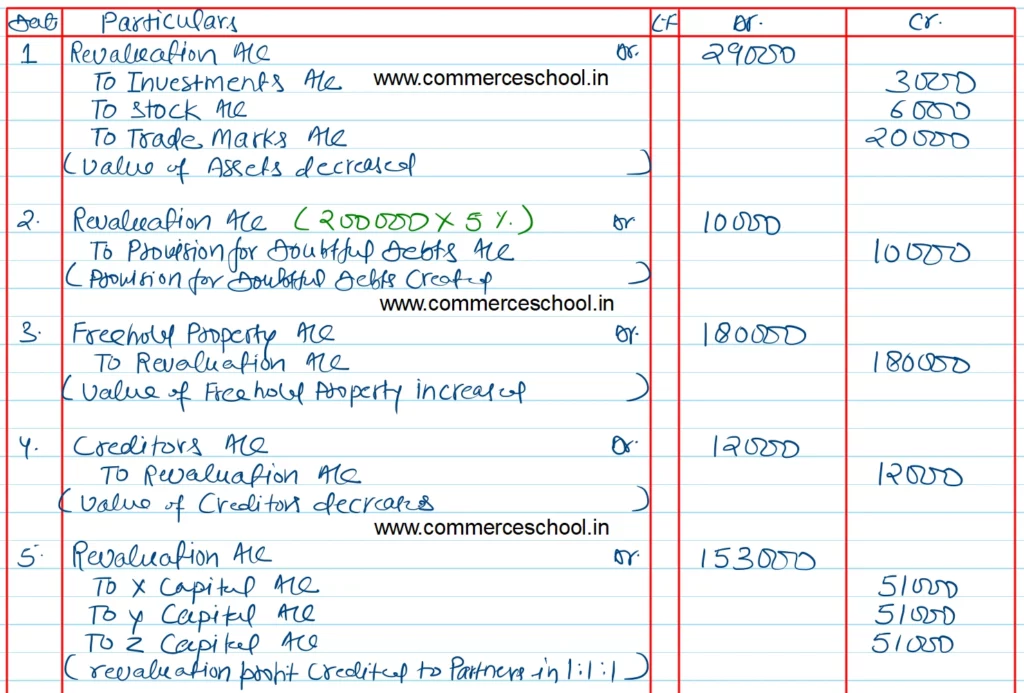

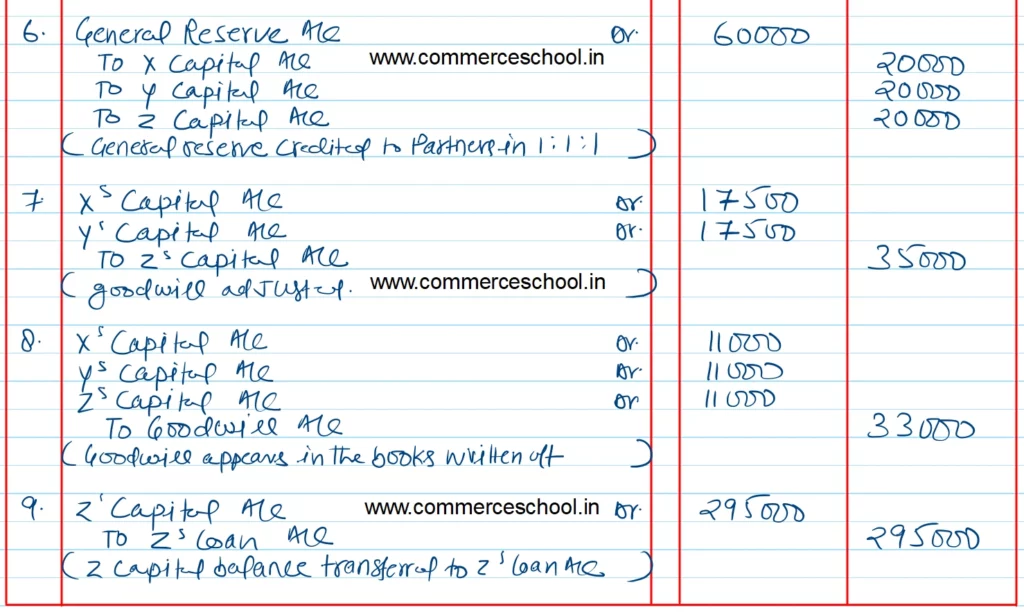

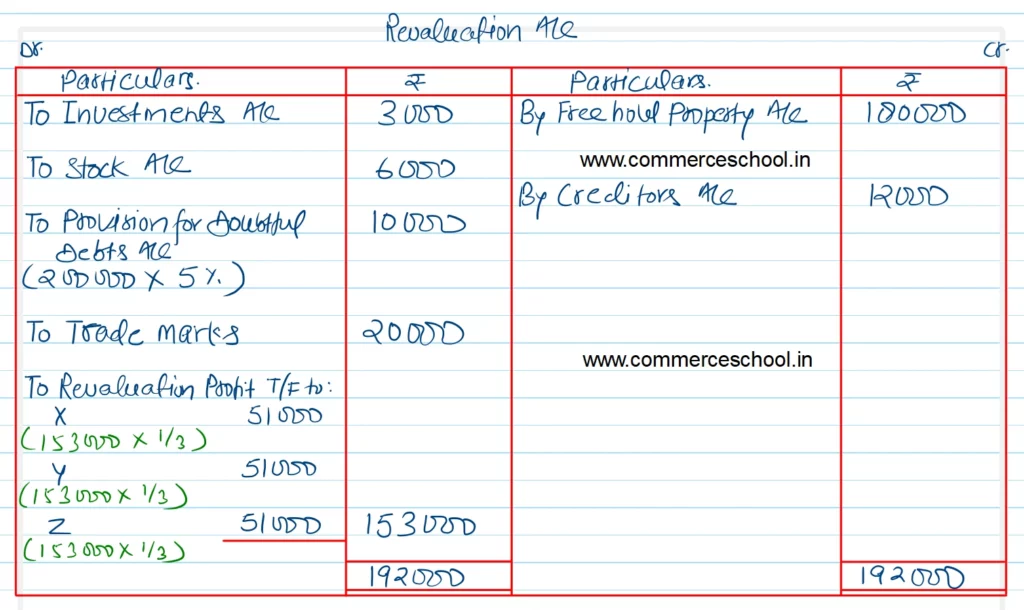

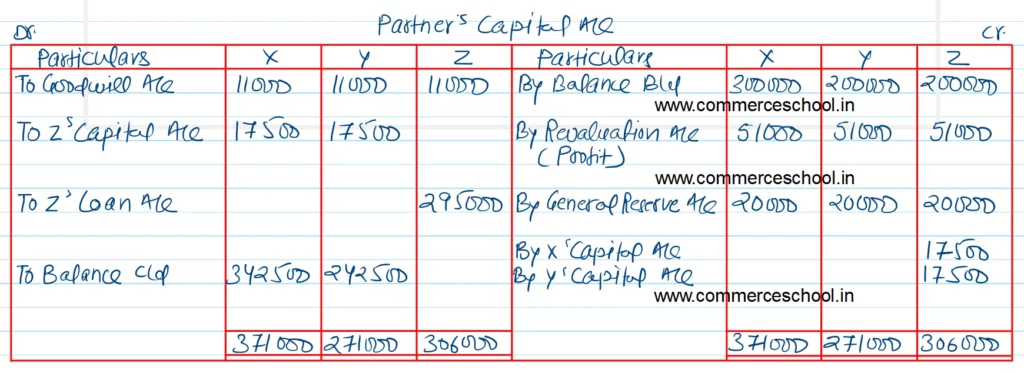

Q. 33. X, Y and Z are partners in a firm sharing profits and losses equally. The balance Sheet of the firm as at 31st March, 2023 stood as follows:

| Liabilities | ₹ | Assets | ₹ |

| Creditors | 1,09,000 | Cash in Hand and Cash at Bank | 86,000 |

| General Reserve | 60,000 | Debtors | 2,00,000 |

| Provident Fund | 20,000 | Stock | 1,00,000 |

| Capitals: X Y Z | 3,00,000 2,00,000 2,00,000 | Investments (at cost) | 50,000 |

| Freehold Property | 4,00,000 | ||

| Trade Marks | 20,000 | ||

| Goodwill | 33,000 | ||

| 8,89,000 | 8,89,000 |

Z retires on 1st April, 2023 subject to the following adjustments:

(i) Freehold Property be valued at ₹ 5,80,000.

(ii) Investments be valued at ₹ 47,000; and stocks be valued at ₹ 94,000;

(iii) A provision of 5% be made for doubtful debts.

(iv) Trade Marks are valueless.

(v) An item of ₹ 12,000 included in creditors is not likely to be claimed.

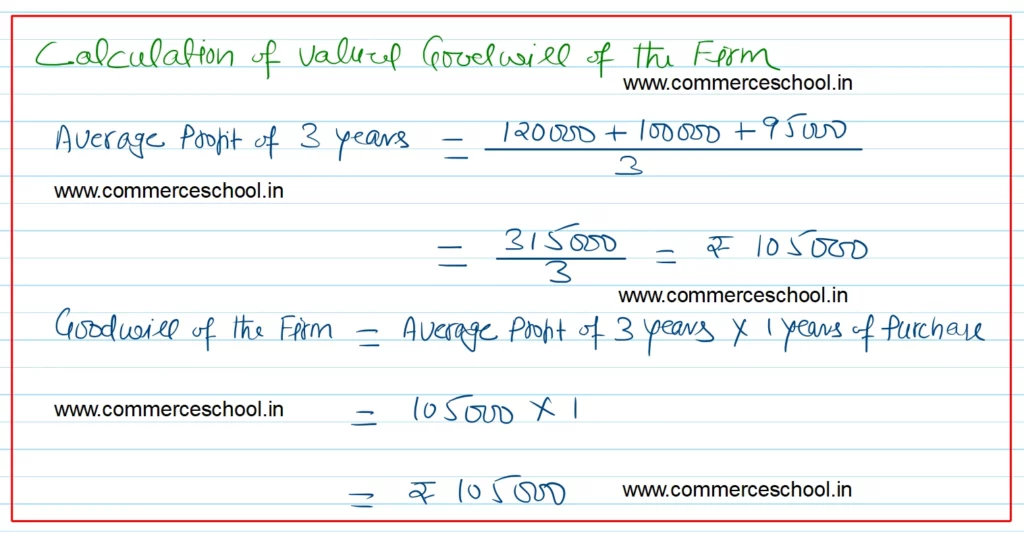

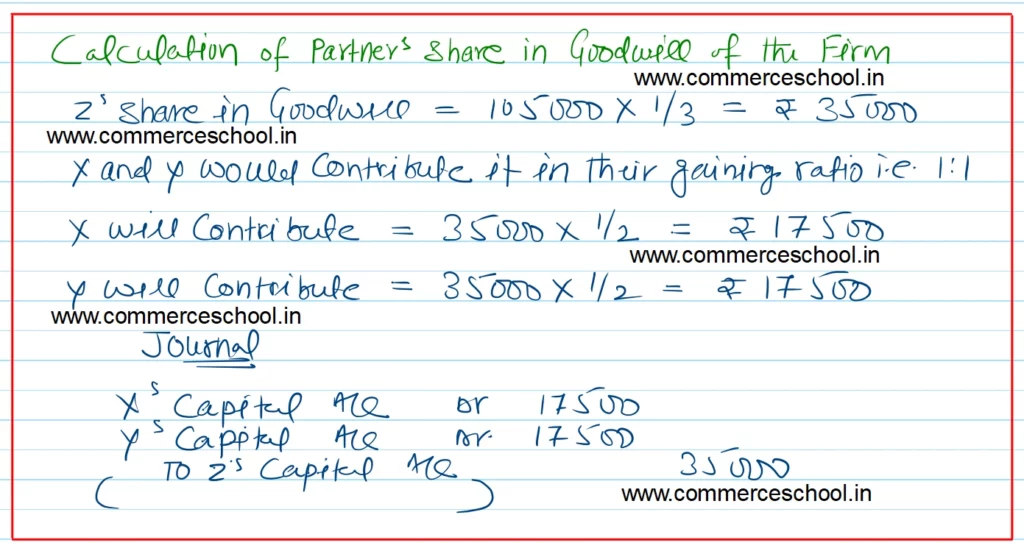

(vi) Goodwill be valued at one year’s purchase of the average profit of the last three years. Profits ending 31st March were : 2021 ₹ 1,20,000; 2022 ₹ 1,00,000 and 2023 ₹ 95,000.

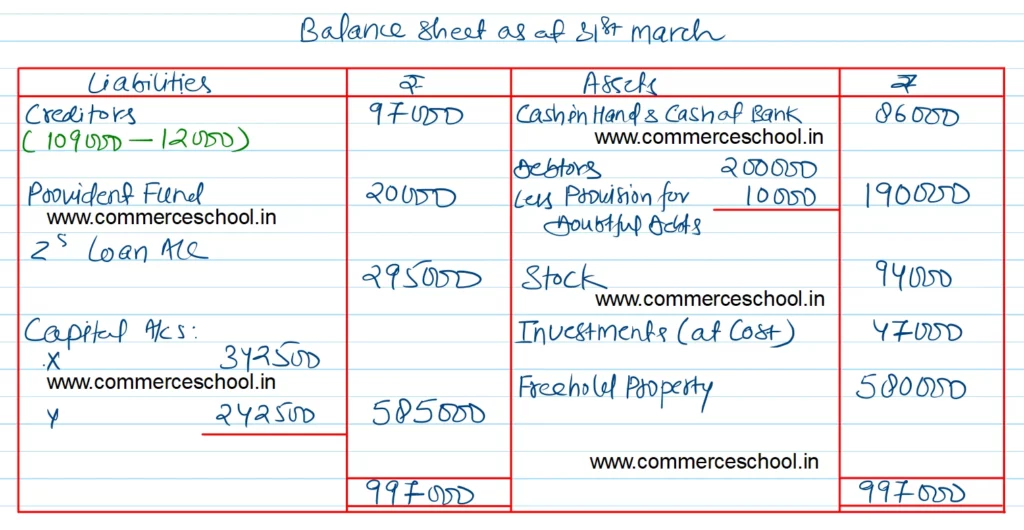

Pass journal entries, give capital accounts and the balance Sheet of the remaining partners.

[Ans. Gain on Revaluation ₹ 1,53,000; Z’s Loan A/c ₹ 2,95,000; Capitals X ₹ 3,42,500; Y ₹ 2,42,500; B/S Total ₹ 9,97,000.]

Solution:-

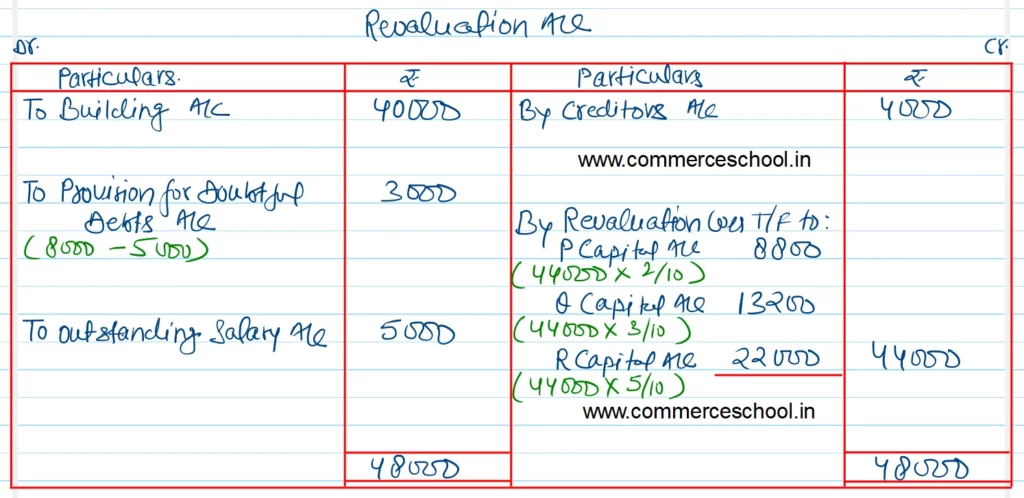

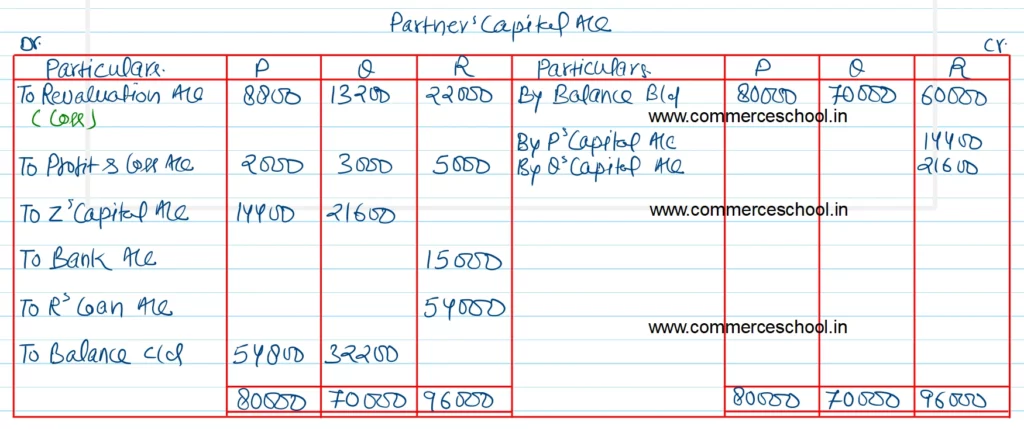

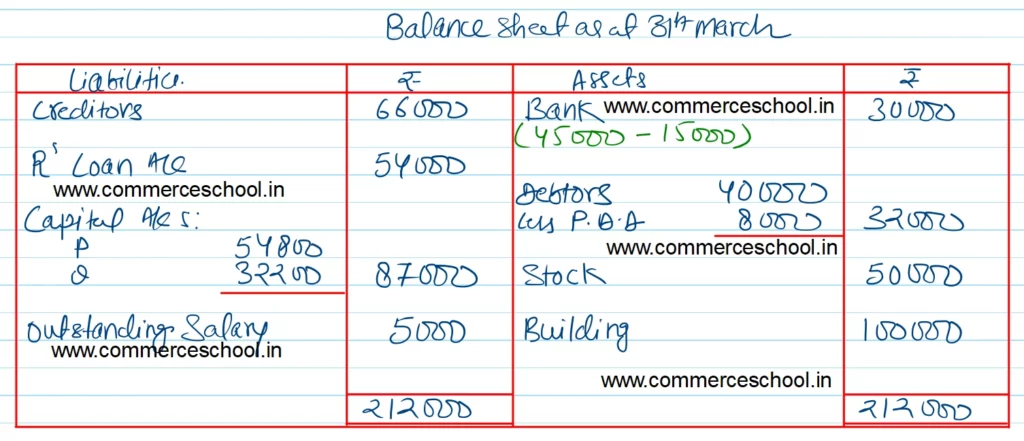

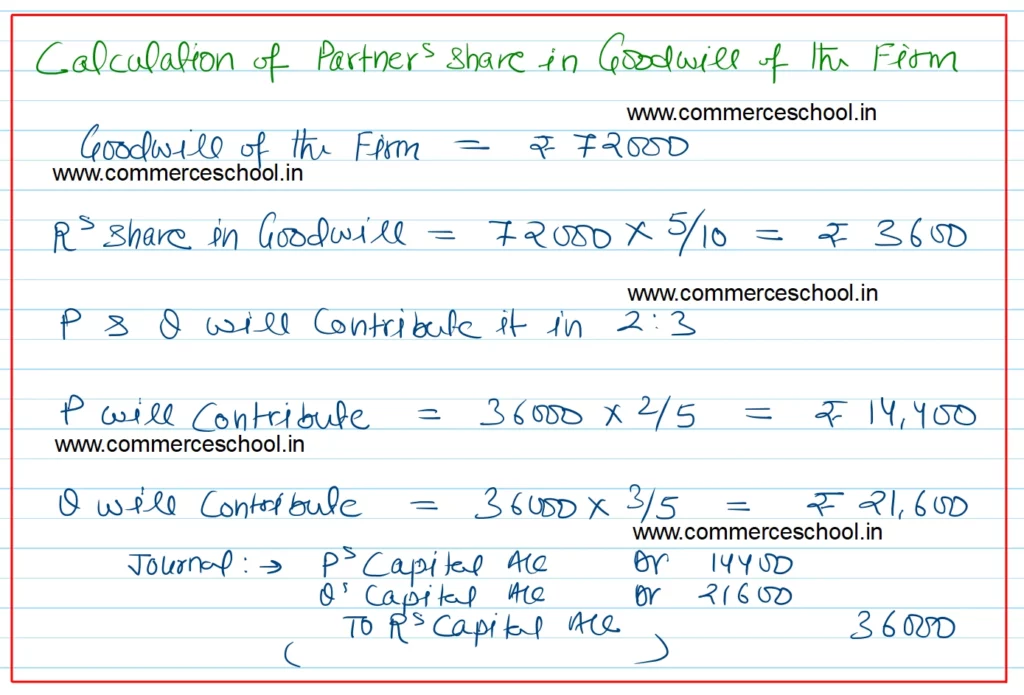

Q. 34. P, Q and R were partners in a firm sharing profits in the ratio of 2 : 3 : 5. On 31-3-2024 their Balance Sheet was as follows:

| Liabilities | ₹ | Assets | ₹ |

| Creditors | 70,000 | Bank | 45,000 |

| Capital Accounts: P Q R | 80,000 70,000 60,000 | Debtors 40,000 Less: Provision for Doubtful Debts 5,000 | 35,000 |

| Stock | 50,000 | ||

| Building | 1,40,000 | ||

| Profit and Loss A/c | 10,000 | ||

| 2,80,000 | 2,80,000 |

On the above date R retired from the firm due to his illness on the following terms:

(i) Building was to be depreciated by ₹ 40,000.

(ii) Provision for doubtful debts was to be maintained at 20% on debtors.

(iii) Salary outstanding ₹ 5,000 was to be recorded and creditors ₹ 4,000 will not be claimed.

(iv) Goodwill of the firm was valued at ₹ 72,000.

(v) R was to be paid ₹ 15,000 in cash, through bank and the balance was to be transferred to his loan account.

Prepare Revaluation Account, Partner’s Capital Accounts and the Balance Sheet of P and Q after R’s retirement.

[Ans. Loss on Revaluation ₹ 44,000; R’s Loan A/c ₹ 54,000; Capital Accounts: P ₹ 54,800 and Q ₹ 32,200; B/S Total ₹ 2,12,000.]

Solution:-