[DK Goel] Q. 35, 36 Retirement of Partner Solutions Class 12 CBSE (2026-27)

Here are the solutions of Question number 35 and 36 of Retirement of Partner chapter 5 of DK Goel Class 12 CBSE (2026-27)

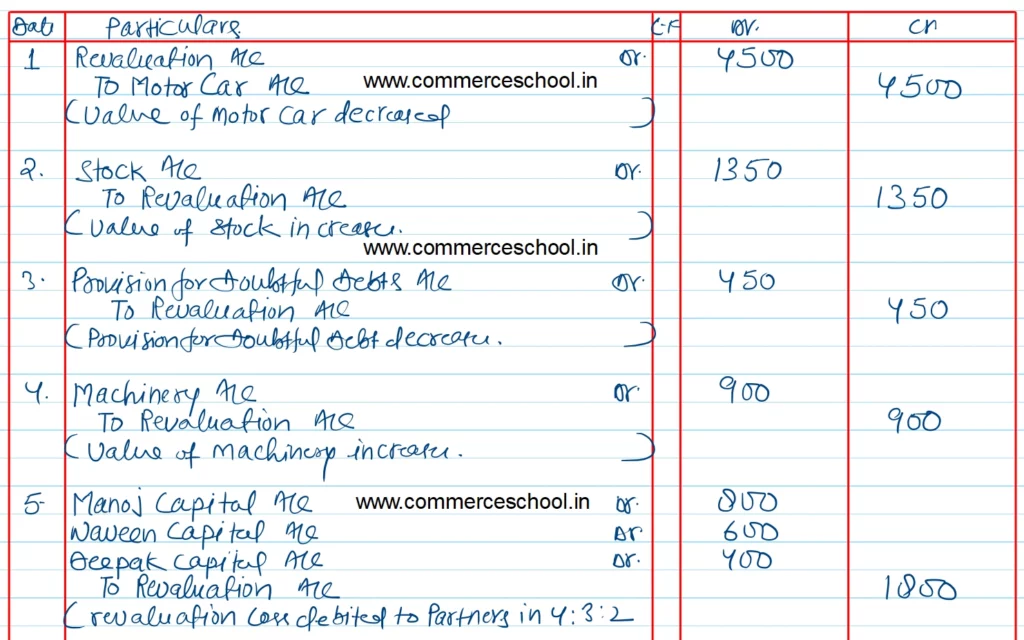

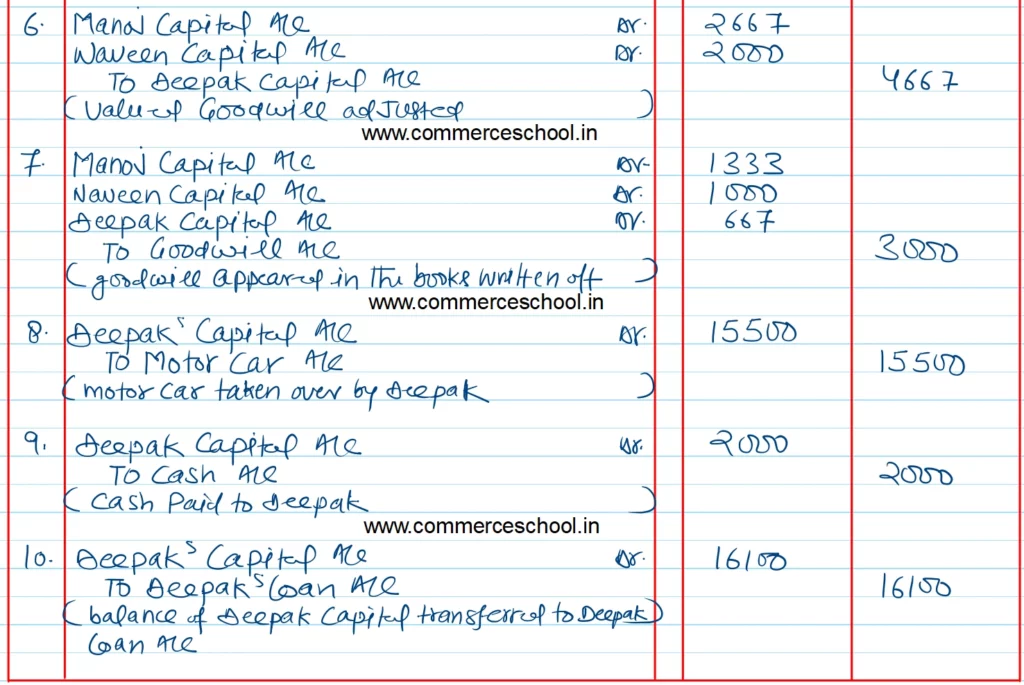

Q. 35. Manoj, Naveen and Deepak were partners sharing profits and losses in the ratio of 4 : 3 : 2. As at 1st April 2022, their Balance Sheet was as follows:

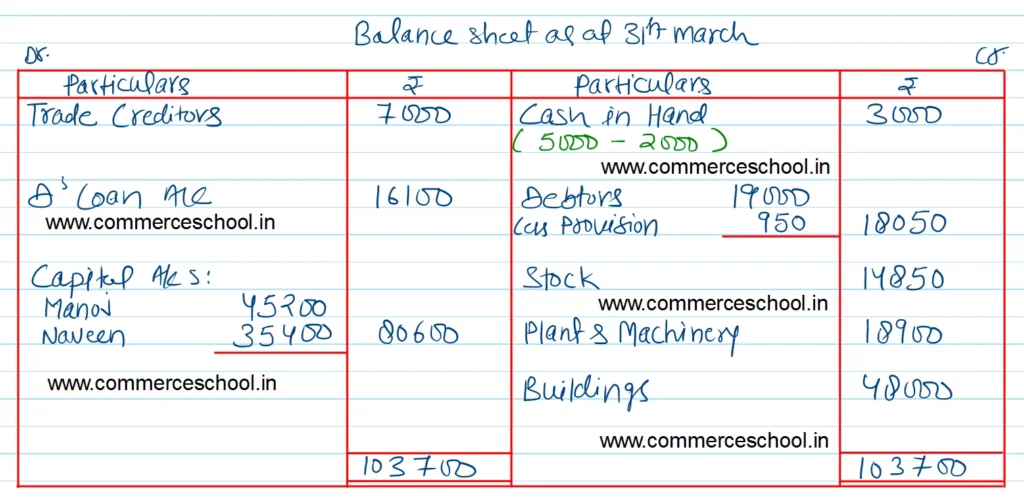

| Liabilities | ₹ | Assets | ₹ |

| Trade Creditors | 7,000 | Cash in Hand | 5,900 |

| Capitals: Manoj Naveen Deepak | 50,000 39,000 30,000 | Debtors 19,000 Less: Provision 1,400 | 17,600 |

| Stock | 13,500 | ||

| Plant and Machinery | 18,000 | ||

| Motor Car | 20,000 | ||

| Buildings | 48,000 | ||

| Goodwill | 3,000 | ||

| 1,26,000 | 1,26,000 |

Deepak retired on the above date as per the following terms:

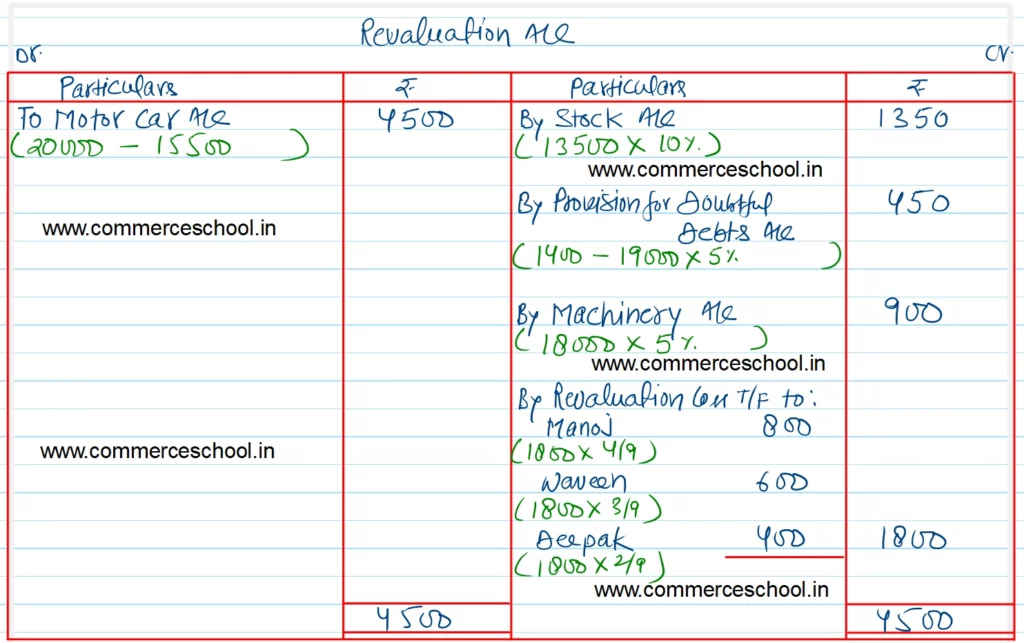

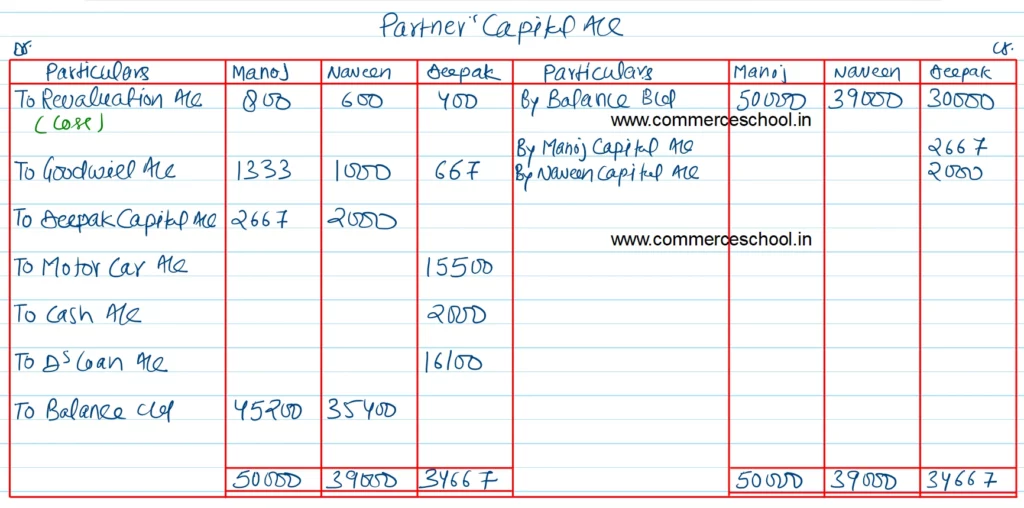

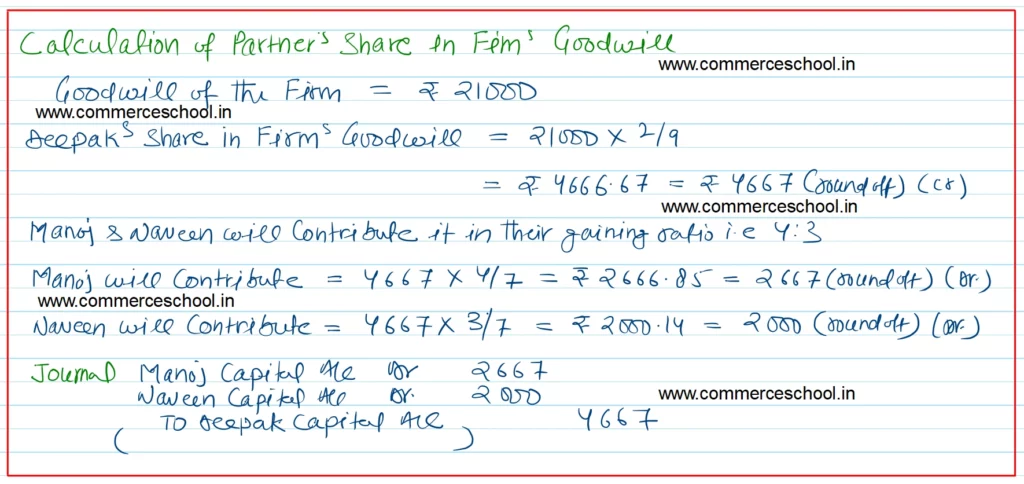

- Goodwill of the firm was valued at ₹ 21,000.

- Stock to be appreciated by 10%.

- Provision for doubful debts should be 5% on debtors

- Machinery is to be valued at 5% more than its book value.

- Motor car is revalued at ₹ 15,500. Retiring partner took over Motor Car at this value.

- Deepak be paid ₹ 2,000 in cash and balance be transferred to his loan account.

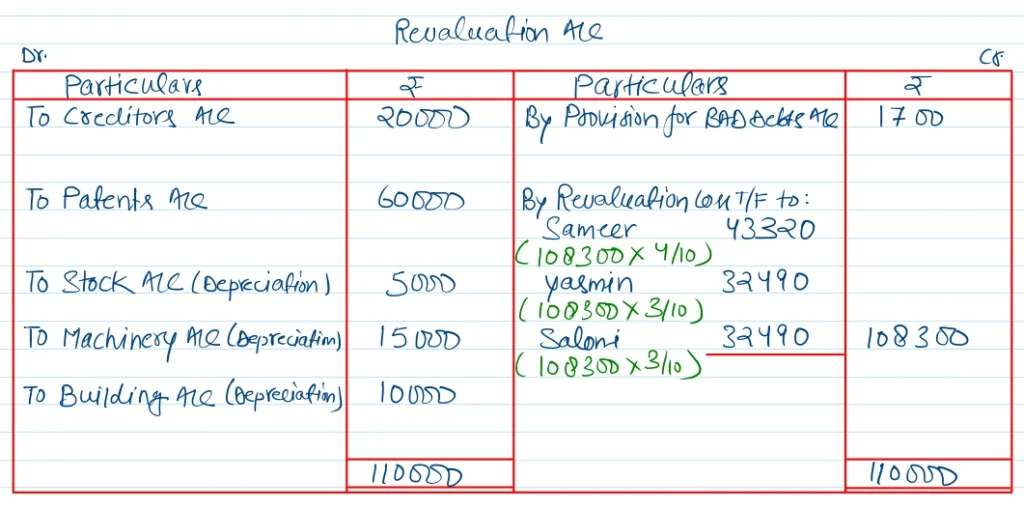

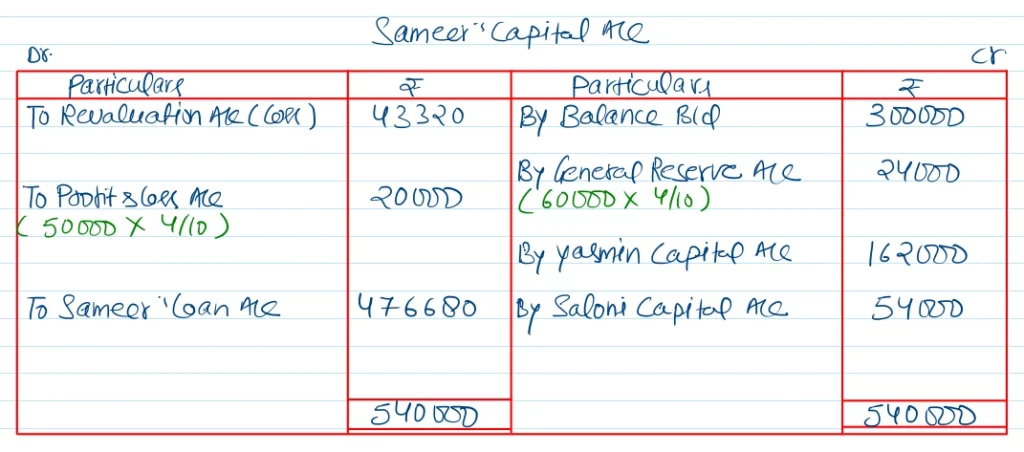

Show necessary journal entries. Prepare Revaluation Account, Capital Accounts and Opening Balance Sheets of continuing partners.

[Ans. Loss on Revaluation ₹ 1,800; Deepak’s Loan A/c ₹ 16,100; Capitals : Manoj ₹ 45,200; Naveen ₹ 35,400; B/S total ₹ 1,03,700.]

Hint: Goodwill amounting to ₹ 3,000 will be written off among old partners in old ratio and Deepak’s Share in ₹ 21,000 will be debited to the accounts of Manoj and Naveen in gaining ratio i.e., 4 : 3.

Solution:-

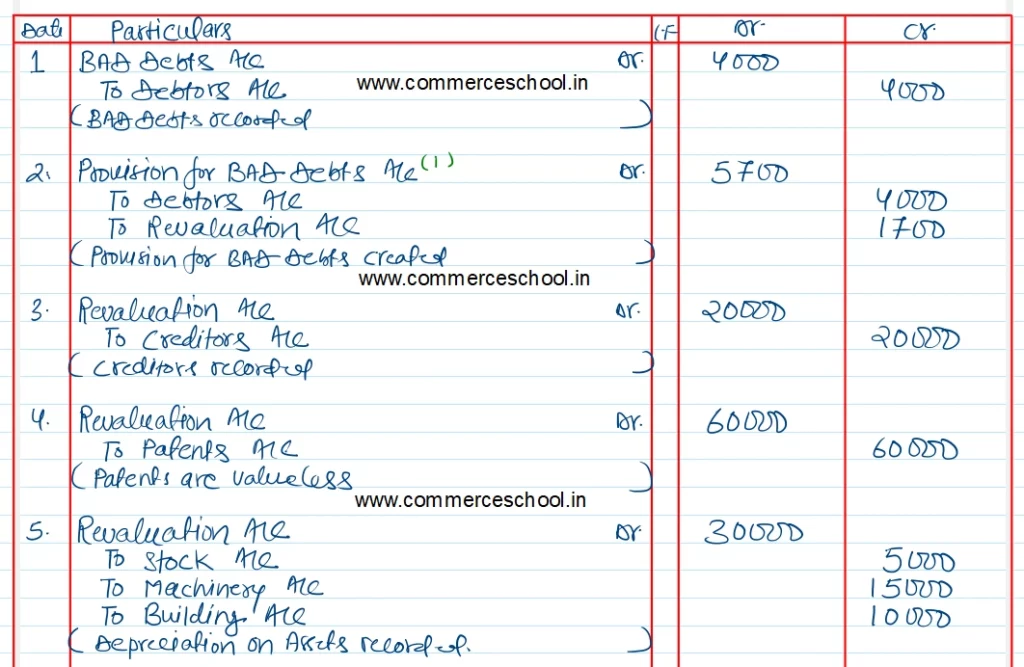

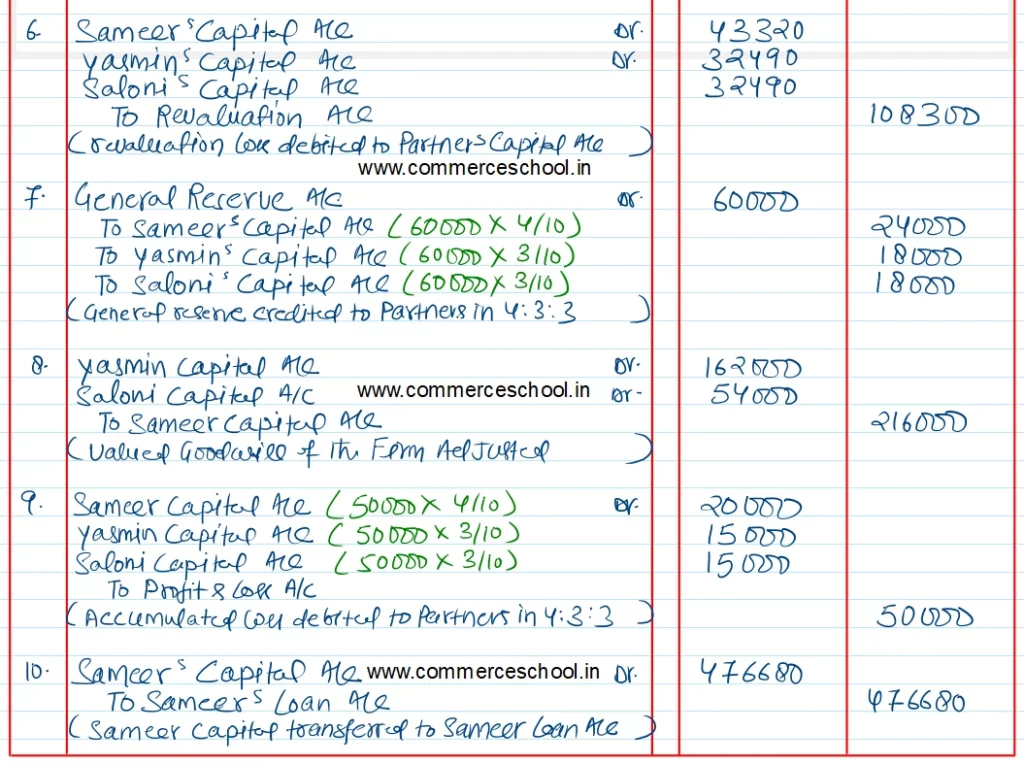

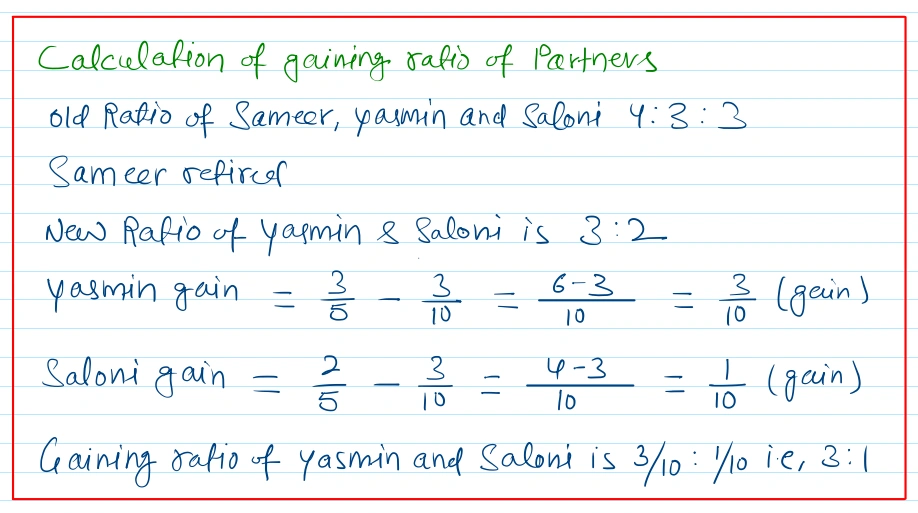

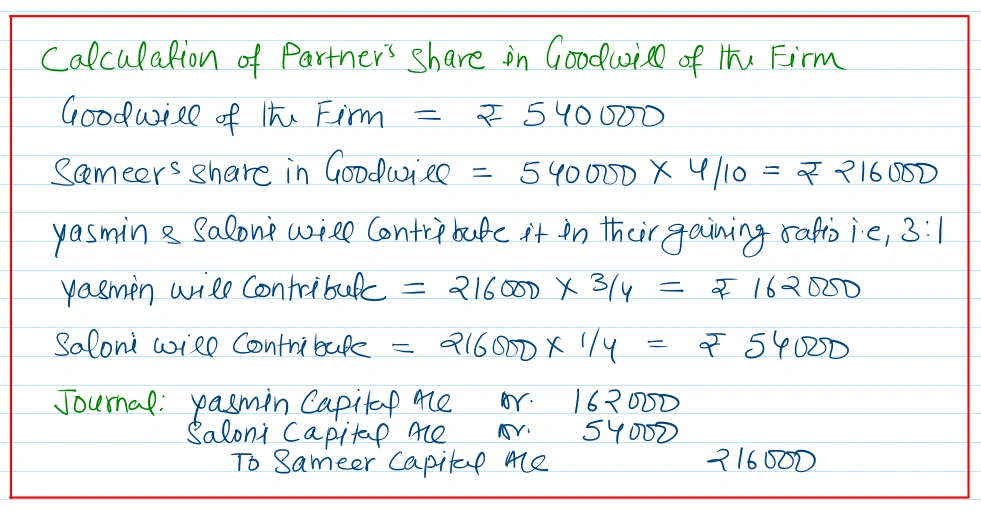

Q. 36. Sameer, Yasmin and Saloni were partners in a firm sharing profits and losses in the ratio of 4 : 3 : 3. On 31.3.2016, their Balance Sheet was as follows:

Balance Sheet of Sameer, Yasmin and Saloni as at 31st Marc

| Liabilities | ₹ | Assets | ₹ |

| Creditors | 1,10,000 | Cash | 80,000 |

| General Reserve | 60,000 | Debtors 90,000 Less: 10,000 | 80,000 |

| Capitals: Sameer Yasmin Saloni | 3,00,000 2,50,000 1,50,000 | Stock | 1,00,000 |

| Machinery | 3,00,000 | ||

| Building | 2,00,000 | ||

| Patents | 60,000 | ||

| Profit and Loss Account | 50,000 | ||

| 8,70,000 | 8,70,000 |

On the above date, Sameer retired and it was agreed that:

(i) Debtors of ₹ 4,000 will be written off as bad debts and a provision of 5% on debtors for bad and doubtful debts will be maintained.

(ii) An unrecorded creditor of ₹ 20,000 will be recorded.

(iii) Patents will be completely written off and 5% depreciation will be charged on stock, machinery and building.

(iv) Yasmin and Saloni will share profits in the ratio of 3 : 2.

(v) Goodwill of the firm on Sameer’s retirement was valued at ₹ 5,40,000.

Pass necessary journal entries for the above transactions in the books of the firm on Sameer’s retirement.

[Ans. Loss on Revaluation ₹ 1,08,300; Amount transferred to Sameer’s Loan A/c ₹ 4,76,680.]

Solution:-